Dynamites come in small packages. And mostly everything in India.

British economist E.F. Schumacher in his award-winning book titled “Small Is Beautiful: Economics As If People Mattered” advanced the argument that small and appropriate technology will empower people.

Bite-sizing of consumer products and commodities, or sachetisation, has been pioneered by India, as early as some 70 years ago when we started putting tea leaves in small paper pouches just enough to make tea for two.

And sachets have worked for consumer products. But is it working for banking?

Think about microfinance - it came from Bangladesh in the 1980s and fit into India like a piece of a puzzle. It unlocked formal credit for underserved populations by going door-to-door in villages, eschewing the need for onerous collateral, and collecting payments in small, weekly instalments.

Microfinance should have done to India what sachets did to shampoo companies. But microfinance’s potential to be the MSME messiah is still unrealised; Mudra, the government’s refinancing support scheme for banks/MFIs/NBFCs that wanted to disburse microcredit to MSMEs, was one of the more promising Grameen micro-credit schemes. Until it wasn’t - our two-part series on the Mudra scheme (Part I and Part II) involved a simple data analysis showing how it largely hasn’t succeeded in achieving the full objectives of financial empowerment, inclusion, or job creation.

Indian households’ savings rate fell sharply to 10.8% in FY22 from 15.9% in FY21; inflation is expected to stay above the monetary policy panel’s target of 2-6% for three quarters in a row and people’s purchasing power is eroding.

Microcredit is crucial in sustaining the livelihoods of low-income households and MSMEs, especially during seemingly one of the most financially stressed times in recent years.

It's well-established that sachet loans, the bite-sized version of microcredit, work. It works because it’s targeted, short-term, collateral-free, and contextual. We’ve written about why it works here and here, but I want to try to answer a couple of questions today to think of how we can make sachet loans work.

What is the enabling architecture needed to make sachet loans work?

For sachetised loans to work, products must be built in a way that’s -

Scalable

API-driven

Modular

Cloud-based

This can only happen when every player in the ecosystem is working in tandem

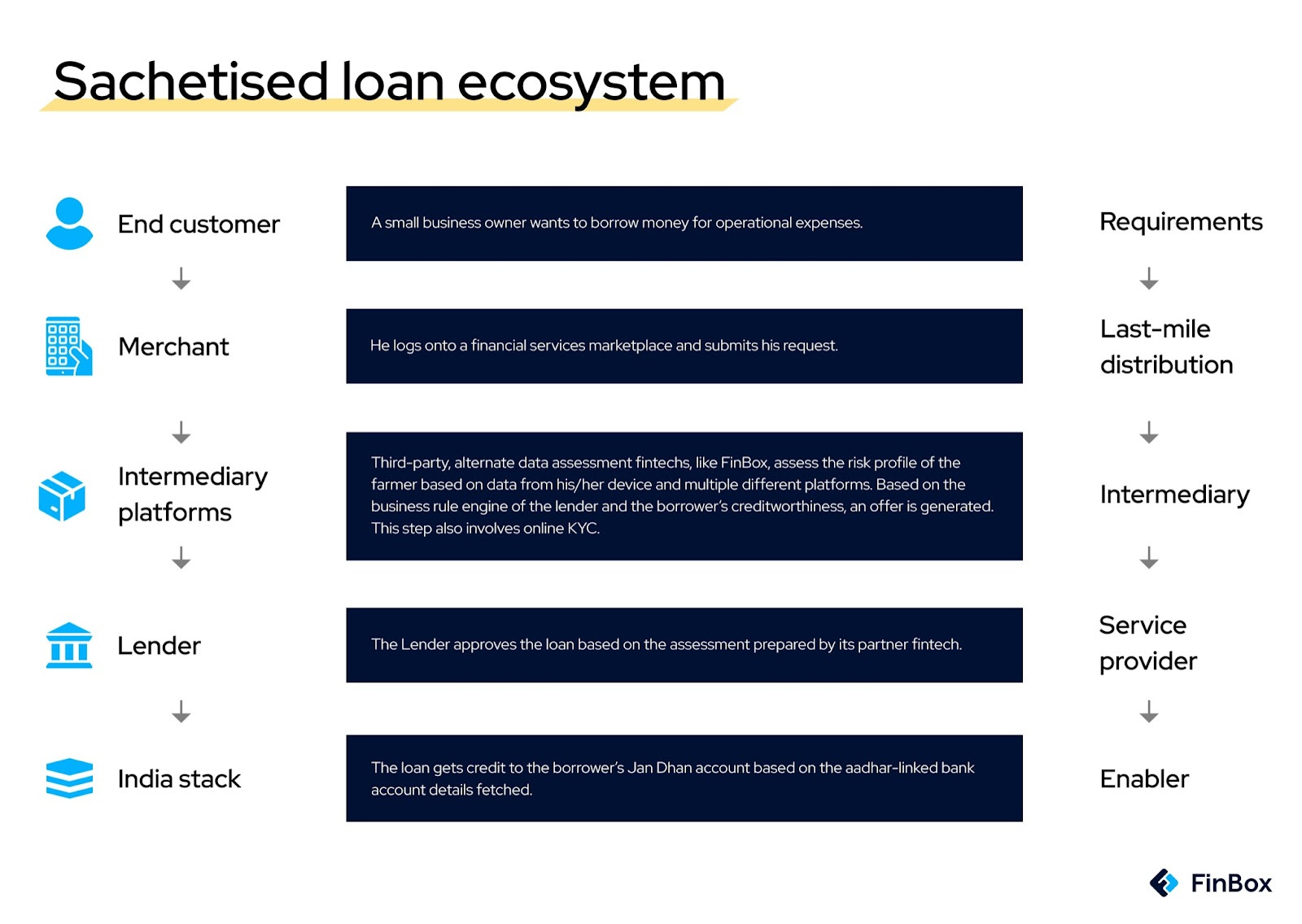

For a small business owner, like a farmer in the example above, there could be different needs at different points in the year. He’d probably need financing to transport his goods from his farm to the Mandi, which would then count as business vehicle trip financing. Unlike a direct transfer of money in the example above, this one could be designed with end-use control. That means control could be in the form of paying the transportation company/ truck driver directly.

It's easy to understand why a lender would be more comfortable with an arrangement like this. And here’s also where the architecture comes into play - the same fintech partners that give a green signal to the lender to lend, are also continuously monitoring the farmer’s activity to ensure dues are paid on time.

The same lender and the same partner fintech can also lend to the truck driver in this example with end-use control, where the control comes in the form of fuel cards and paying for FastTag.

There needs to be synergy between all the players in the ecosystem to ensure that loans are disbursed at source and immediately.

But none of this is possible with our existing fintech infrastructure. This brings us to the second question-

How can we put existing innovation and infrastructure to GOOD use?

Enter Account Aggregator-driven OCEN framework.

OCEN is a new paradigm for credit that seeks to ‘provide a common language for lenders and marketplaces to build innovative, financial credit products at scale’.It provides a standardized set of APIs so that applications that already interface with individuals and MSMEs can effectively ‘plug in’ lending capabilities into their current product and service offerings.

Think about what UPI did to payments, that’s what OCEN hopes to do to credit.

A vital piece of OCEN is the Account Aggregator (AA) framework. For any open protocol to work, data flows need to be easy, that’s what AA ensures. I have a few thoughts about making good use of AA -

We’re putting AA to good use already: At its core, AA brings data out of silos into a level playing field. And it's done wonders already - look at what cash flow-based underwriting, and alternate data underwriting have done. It’s brought under-served communities into the formal lending system and big banks have been in on it too. In fact, a couple of weeks back I wrote about how private banks are getting MSME lending right.

We might have a data visibility problem: In essence, OCEN will ensure tailor-made microcredit/nano credit products that solve immediate business problems. But businesses and consumers have complex financial lives. Looking at GST data + cashflow isn’t going to be enough anymore, how do we get a holistic view of a borrower? What about looking at investments, insurance, savings, pension plans, fintech apps, etc? There’s a whole world of data we’re missing, even with APIs for every data set, the ability to AGGREGATE and present it neatly is lacking. How can we solve market fragmentation?

Data needs to be contextualized for everybody’s benefit: The big assumption is the higher your income, the better you are with money. Obviously, that isn’t necessarily true. Some low-income earners live paycheck to paycheck and some immediately cash the cheque to have more control over their money. These are two very different life contexts. How can we infer data in a way that contextualizes for everyone? A shared framework that can come out of AA.

Look at Financial Health Network, a US-based pro bono organisation with several members, ranging from businesses to policymakers etc, something like Ispirit. They’ve got a meter that measures a consumer’s financial health that looks like this -

What could be the possible metrics we measure?

Are you spending less than your income?

Do you have enough liquidity for an emergency?

What kind of saving instruments have you invested in?

Do you have insurance?

Have you paid bills, utilities and other debt on time?

Does your business have manageable debt?

There could be several overarching questions that measure financial health. Imagine having a meter like this that immediately tells you where the borrower is and you could lend accordingly.

The bottom line of Sachetised products is this - interoperability, ease of use and contextualisation. And the wonder of OCEN is anybody, from a Kirana store to a cab aggregator to the shipping company you use could be a Loan Service Provider (LSP) on the network and that means credit where credit is required. For banks and Fintechs, that means keeping a sharp eye out for new sources of data and how lending models and business rule engines can be consistently updated to lend better.

For MSMEs and new-to-credit borrowers, early money is like yeast. It makes them rise, but this early money is the hardest to get. Even the first 10,000 Rs can feel like the hardest to get. A tailor from a small town in India might struggle just as much as a city-bred entrepreneur eager to start an ethical fashion brand. This is where contextual lending can help, micro loans like what Shopify does for entrepreneurs on its platform or via OCEN.

Sachietised loans have the potential to be the zeitgeist of micro financing, we just have to build products as if people mattered.