Will digital banking units further stir the bank-fintech contest?

Will digital banking units further stir the bank-fintech contest?

The success of financial technology in India is owed to a certain agility (though often, it may seem counterproductive) – for every two steps forward, we’re willing to take a step back.

At FinBox, for instance, we’re idealistic about digitalisation. We’re creating a sophisticated credit architecture intended for an overhaul of traditional lending. But we also recognize that our overarching vision doesn’t always align with the problems at the grassroots.

So, even as we navigate by the light of a north star, we’re compelled to routinely check for very real roadblocks in our path. To build not only for the future, but also for the present – in a way that pays off exponentially in the future.

This willingness to face facts and solve ground-level problems doesn’t just make business sense – it also guides the hand of policy makers in a government tasked with building a Digital India. An India that’s currently grappling with a glaring digital and financial divide.

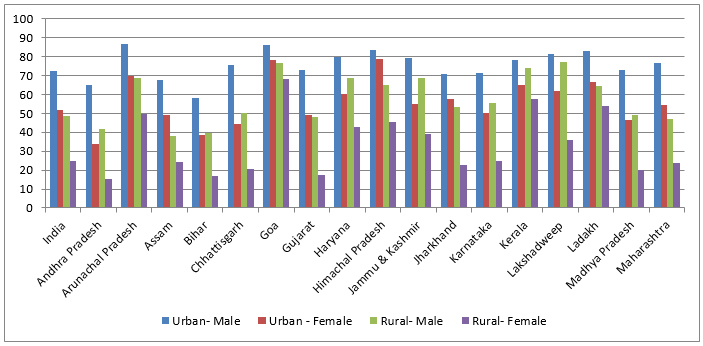

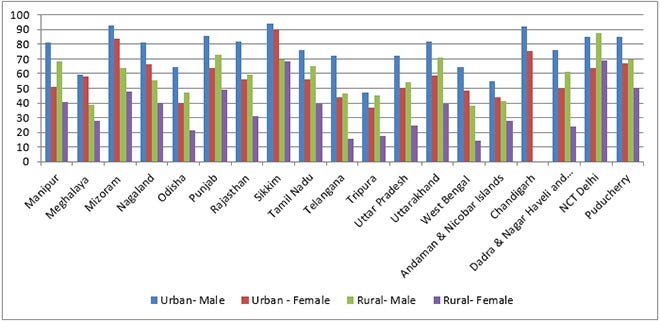

72.5% of India’s urban males and 57.5% of urban females have ever used the internet. In rural India, those numbers stand at 48.7% for males and 24.6% for females. Refer to the following chart for a more detailed state-wise breakdown of these numbers.

Public sector banks have 28,828 branches in rural areas and 16,801 in metropolitan areas. The numbers are heartening, but not nearly enough when 70% of the country’s population lives in rural areas.

The skewed distribution also holds true of ATMs - PSBs have 33,783 ATMs in metropolitan areas but only 29,372 in rural areas.

It isn’t fair to expect the same speed and penetration of digital and financial adoption from rural and semi-urban parts as metropolitan India. Financial education, digital literacy, internet and device access along with the physical process of hand holding will provide the bridge needed for such a transition.

Digital isn’t possible without ‘phygital’

Earlier this week, a joint initiative by the union government, the RBI and the Indian Banks’ Association was launched to achieve precisely this. Digital banking units (DBUs) opened for business in small towns and villages of 75 districts.

These outlets run by several public and private sector banks are mandated to offer a set of banking services digitally, in self-service and assisted modes. Customers will be able to open bank accounts, avail of retail and MSME loans, and access the benefits of several government schemes.

(1)")

I won’t get into more micro details of how this initiative works. You can find a detailed lowdown on the role of digital banking units here. Instead, I’d like to focus on the new competitive front the DBU model has thrown open.

A godsend for banks

Buried within the financial inclusion narrative of DBUs is a story of pressing business significance. The digital banking units model will give a decisive leg-up to banks in the race against fintechs and NBFCs to capture market share.

Firstly, the DBU model has already invited countless comparisons to the revolution brought about by ATMs in the 1990s. Just like ATMs cut down on the repetitive task of cash withdrawal for bank tellers, freeing them up to pursue more value-additive functions, self-service DBUs will take out manual intervention from a whole suite of banking services. This will give banks a much-needed pivot towards digitisation in smaller markets.

Second, banks with even a minimal presence in rural and semi-urban areas can onboard customers for their assets segment. The RBI has allowed banks to share the core banking system and other back office information systems for digital banking with their incumbent systems. This will be banks’ answer to fintechs’ low onboarding costs.

Most significantly, however, digital banking units are widely being regarded as a precursor to the RBI’s impending rollout of a special digital banking license. DBUs will create inroads for traditional banks to operate on this highly anticipated license.

This is where it gets interesting. The regulator has allowed banks to outsource their digital banking operations under this model. Since many of these banks already have partnerships with neobanks, this fintech segment will both gain and lose from such scrutiny.

Currently, neobanks are viewed as “the function of a regulatory vacuum”. The new model leaves room for neobanks to formalize their relationships with their licensed lending partners. Neobanks already have a digitally superior front end and core along with a host of tech savvy business correspondents, placing them at an advantage when it comes to distribution that will promote their adoption.

But there’s a catch – regulatory ambiguity so far meant a lower barrier to entry for fintechs, raising suspicions of sub-par players entering the market that may pose a consumer protection risk from the RBI’s standpoint. This first step towards a digital banking license would restrict the entry of neobank fintechs in the market.

Regardless, banks have their work cut out for them.

Coming back to the point I made at the beginning – for all the noise around digitisation, banks are required to take a ‘phygital’ approach under this model. Their mission is to digitize – which comes with the promise of greater business dividends in the future – will, in the short-run, be frustratingly slow. Unlike their fintech counterparts, they will have to undergo a patient exercise of customer education before they can reap the rewards of digitisation.

In fact, setting up these units won’t be easy. Banks will be required to rebuild their tech infrastructure in the hinterlands to meet even the most basic requirements laid out by the RBI. It’s exhaustive list for front-end and distribution includes:

Interactive teller machines

Interactive bankers

Service terminals

Teller and cash recyclers

Interactive digital walls

Self-service card issuance devices

Video KYC apparatus

A secure and connected environment to use own devices

Video conferencing facilities

Cyber security safeguards

Moreover, the room for competition among banking contenders is lukewarm, at best. Just like ATMs, the underlying digital architecture and infrastructure of digital banking units remains uniform. The mandatory bouquet of services is the same for all participating banks. Crafting a personalized experience based on the location and demographics served by a DBU is the only way to gain an edge.

The regulator has also enforced fresh reporting requirements for digital banking units. DBUs must be reported as a sub-segment within retail banking and their performance updates must be presented to the RBI’s Department of Supervision on a monthly basis and in the annual report.

Compete or collaborate?

Apart from these operational challenges, banks also face the challenge posed by the fintech-NBFC combine. NBFCs have traditionally served high risk customers in niche segments like SME and agriculture, largely sidelined by banks.

They have also been more technologically inclined and likewise reinvented their business models. As a result, even though they only form 25% of the total assets of the banking industry, NBFCs accounted for 15 million credit inquiries as of June 2022 – at par with private and public sector banks.

Competition from NBFCs as well as fintechs over the market share of underserved customers is simply too high. However, traditional banks could go two ways:

Leverage their existing neobank partnerships or forge new ones to fuel the capacity of their DBUs. Thus, giving regulatory legitimacy to fintechs and sharing the rewards – a win-win.

Build neobank-like capabilities in-house. This would shake the foothold of digitalised NBFCs and their tech providers over tier 2 to tier 6 markets.

The backing of vast amounts of capital and a supportive regulatory environment has given banks ample incentive to face their biggest challenge head-on – to rebuild their digital infrastructure for the masses. But will it stoke the flames of competition with their challengers?

Only time will tell.