Will banks finally rise up to the FinTech occasion?

The platform is set, let the lending begin

FinTech will become irrelevant. It’ll become so much bigger and vastly more pervasive, to the point that we won’t use the word anymore. There will be no ‘fintech’ companies anymore, except that every company will be a fintech company. We’ve all heard that one before, right?

But here’s a thought, as we try to democratise credit and financial services for the next billion, we need to account for changing demands. The world is evolving faster than ever and it’s incredibly hard to just keep pace with the times and build in isolation.

What I’m trying to say is - FinTech began with making financial products easily accessible. What happens when financial functionality becomes a native component of the stack (both technology stack and as a business model)? There’s more opportunity for embedded fintech. In other words, rather than constituting a segment on its own, fintech joins the internet, cloud and mobile as the fourth major platform technology.

Five years, two rounds of funding and a little over a 100 employees later, I might sound like I’m axing my own foot with what I’ve said so far - but not really.

FinTech’s evolution will now come from its infrastructure agility. One needs tracks to run rails. And FinTech infrastructure platforms have the potential to power previously inconceived innovation and build not just one but a thousand different $1bn businesses.

One of the most exciting areas for me is the micro, small and medium business segment - especially in India. They provide unlimited opportunity for both product and business innovation.

SMEs are fragmented, diverse and complex. Their owners are quite like individual consumers in that they want what they want, when they want it. And now, they are becoming just as tech savvy as the first billion and tech-demanding, expecting sophisticated, smooth, personalised, and speedy digital experiences with self-serve options.

This should serve as proof enough that banks and financial institutions should stop looking at SME lending through a glass darkly. Embedded finance is a compelling opportunity to better serve SMEs, grow loyalty, and drive revenue. Lenders must start looking at themselves as more than just a bank, they need to be more comprehensive and agile - a one-stop-shop for end-to-end SME finance management.

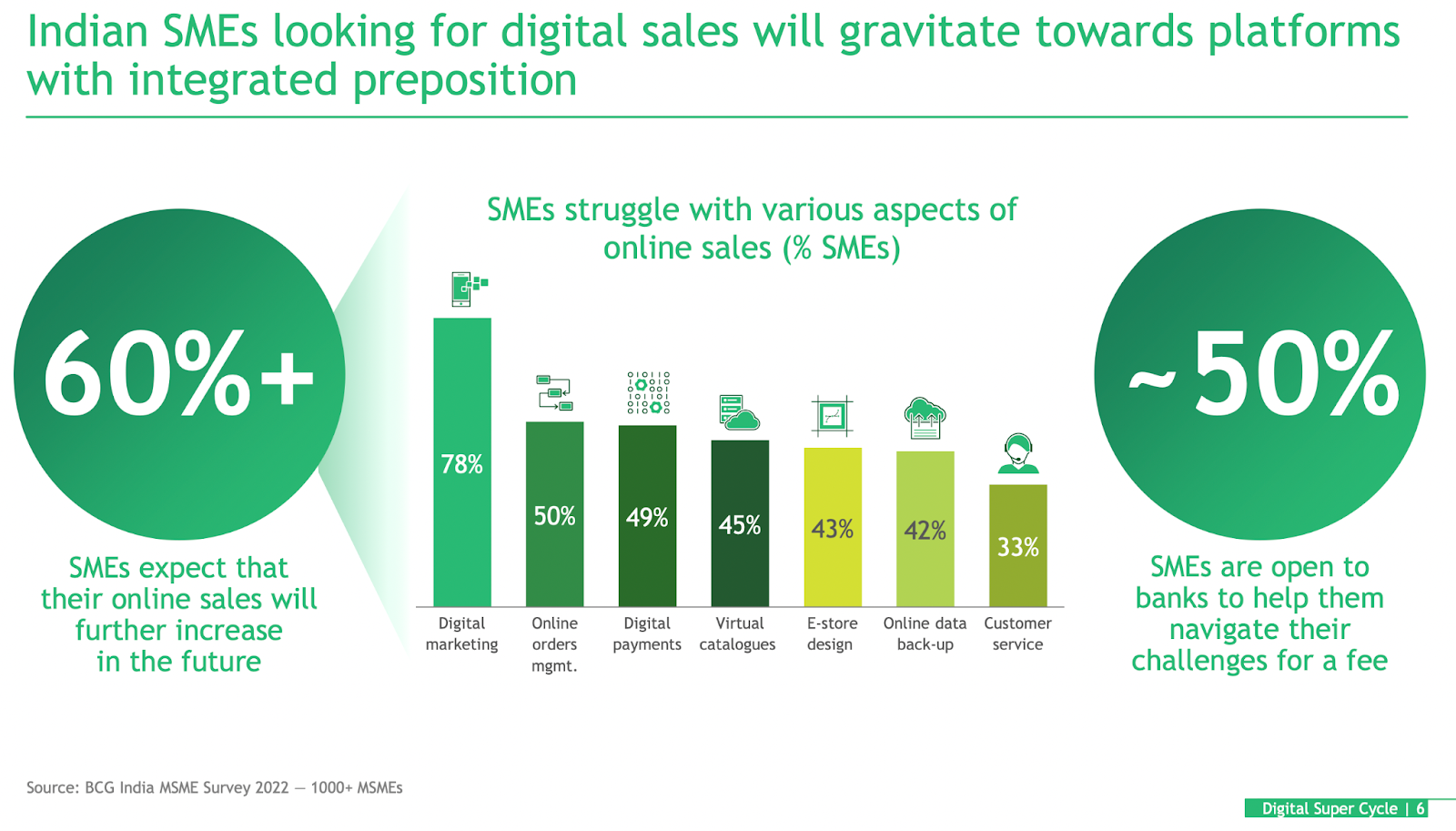

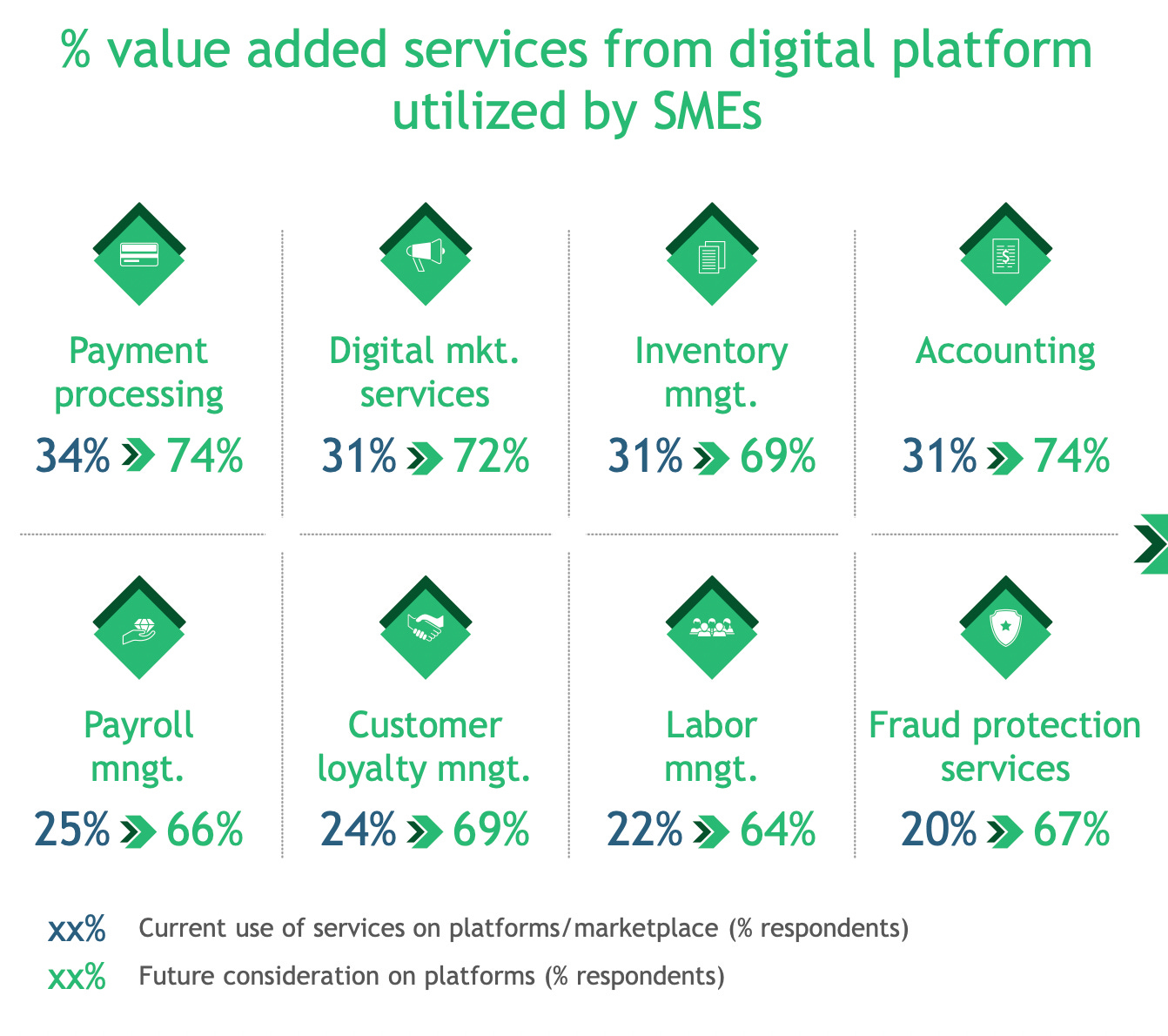

Look at this other piece of research from one of the latest BCG surveys -

Again, this should serve as an indication of which direction the financial services industry should move towards. Why the financial industry only specifically? Because funding is the largest bottleneck that most SMEs face which in turn puts supply chains at risk as it affects the downstream activities, which in turn impacts labourers and customers.

I get by with a little help from embedded finance

How can lenders ensure superior service for SMEs? In three ways -

Integration

Embedded finance is a natural part of the modern SME workflow. It allows for pre-approval, one-click provisioning, dynamic repayments at the point of need. The central premise? A single interface without getting redirected to other pages and simple user journey. The biggest challenge for SMEs is to maintain business momentum through liquidity. Approved cash advances can benefit SMEs and if you’re a lender, being placed in the SME payments flow will give the edge to offer tailored solutions and dynamic repayment functionalities. One survey revealed that 65% SMEs would be happy to switch their existing payments provider for improved integration.

Speaking of dynamic repayments, my colleague had written this piece a while ago on Equated Daily Instalments (EDI) and how it’ll bring formal credit to scores of small businesses. We’ll be delving deeper into this subject during our second webinar ‘EDIs: Making MSME credit work with innovative products’ tomorrow, 10th November at 3 PM, so don’t forget to register here

<insert webinar image>

The other piece of the integration puzzle is public platforms like TReDs - a great invoice discounting system, GST, e-way bill. These are vessels of data waiting to be utilised, if these platforms could be consolidated, SME lending could potentially catapult five years ahead.

Data granularity

The missing piece of the bank-led model puzzle is the high level of granular data that platforms have access to. From real-time payment flows and cash positions to inventory levels and point of sales activity, platforms have access to a broad range of relevant user data. To be relevant in the platform economy then, banks should consider developing digital interfaces that connect all the players in the supply chain. This will enable seamless end-to-end journeys that cover procurement, invoicing and financing. For banks, not only is this an opportunity to underwrite more effectively and lend more, it's also a gateway into the world of supply chain financing.

The data-driven platform model for financial institutions can also ensure new product growth. For instance, dynamic discounting - a data-driven method for buyers to make early payments to suppliers in return for a discount on the invoices. Products like this can not only help SMEs ensure viability of their suppliers and in the process the health of their own supply-chains, it also ensures greater trust in the lending institution.

Deep relationships make for niche products

Behind every SME is an individual that’s looking for trust, ease and speed. In the fast moving world of SME businesses, it can be challenging to understand the unique dynamics when it comes to payment terms, supplier relationships and creditworthiness. For instance, automobile firms develop strategic relationships to an extent where they invest heavily in the suppliers’ businesses. In the cement industry, raw materials are commodities. A typical approach to platform thinking is an exercise in automating various processes, to put it simply. One way to do that for banks is by adopting the account aggregator (AA) framework - all information about customers can be leveraged to apply algorithms and optimize the offering specific to customer needs.

For instance, banks can use the AA framework to determine spending patterns.

A McKinsey survey shows companies with an offensive platform strategy yield a better payoff in both revenue and growth and make them flexible to move across markets.

The bank of tomorrow

Historically, banks have invested heavily in security and not as much into optimizing user experience. The platform environment is going to change that - the bank of tomorrow will be a customer-centric platform where e-commerce, social media and retail payments come together. According to research by McKinsey in 2018, banking returns (between 8-10% at the time of the research), could improve significantly in an ecosystem environment. And banks naturally have a competitive edge thanks to customer trust, regulatory experience, large customer base, and unexploited data.

Banks of tomorrow will benefit from the platform model in terms of revenues, profitability and customer satisfaction. Platform-oriented banks are being called visionary as they’re in a better position to compete with platform players.

In conclusion

Financial services are severely more complicated a space than a cab booking service but if the Shopifys of the world have taught us something - it’s that leveraging data to grow revenue and build trust is an underrated skill. That being said, banks have an inherent advantage by virtue of being legacy organizations. But resistance to change might do more harm than good.

As this McKinsey article succinctly puts it -

“Executing on a platform operating model is arduous. However, when done correctly, it has the potential to deliver four main benefits to all stakeholders: value-oriented business-technology partnerships, stronger performance (speed, efficiency, and productivity), transparency, and a future-ready business model.”

The word FinTechs might become redundant in the future, but the agility, ease, convenience and speed it has introduced to the world will continue to stay - and that’s truly the value proposition of the bank of the future!