Was embracing riskier borrowers FinTechs’ biggest folly?

Almost everything worth doing is risky.

Hi,

Every FinTech you’ve ever met, read about, or heard about has one thing in common - they’re all trying to ‘democratise financial services’ or they’re innovating through ‘alternative data’ and ‘proprietary underwriting’ or working towards ‘financial inclusion’.

These lofty aspirations invite critical scrutiny from some quarters.

An academic paper titled 'FinTech Lending with LowTech Pricing' recently examined FinTech underwriting and pricing to determine if the widely promoted 'big data' and 'advanced analytics' in the industry truly outperform traditional credit scoring models like FICO.

To conduct their analysis, the researchers utilised a dataset encompassing approximately 70% of FinTech loans issued in the US between 2014 and 2020 by prominent lenders such as LendingClub, Upstart, and Avant.

They filtered the dataset to include only loans with the necessary data points for a meaningful analysis and ensured comparability, such as loans with a three-year term.

The study encompassed 2.3 million loans, with an average interest rate of 16.29%, and an average loan amount of $11,898 extended to borrowers with a median income of $62,500 and a median FICO score of 677. For the analysis, FICO scores above 660 were categorised as 'prime,' while those below 660 were deemed 'non-prime.'

The authors' main finding indicates that FinTech lenders' pricing approach is deemed "rather simplistic and inefficient." This conclusion rests on three key arguments:

FinTech lenders continue to heavily rely on conventional credit scores (FICO), suggesting a lack of substantial advancement in their pricing methods.

FinTech loans granted to non-prime borrowers demonstrate a lower level of responsiveness to expected risk compared to loans offered to prime borrowers. This implies a potential inconsistency in risk assessment and pricing strategies.

Across both prime and non-prime fintech loans, loan-level returns generally decrease as the expected risk increases. This pattern suggests that the risk-reward balance in the pricing structure may not be optimised for either borrower category.

Basically, FinTech lenders’ primary ‘innovation’ was serving the borrowers banks didn’t want - by charging higher interest rates

Lending inherently involves risk, as loans are given with the expectation of repayment in the future. Unforeseen events, such as crop failure or obsolescence of skills, can disrupt borrowers' ability to repay, increasing the risk of default. To compensate for this risk, lenders set higher interest rates, like the 78% rate observed in Chambar, Pakistan.

Although the Chambar example is from the 90s, the rationale still applies today.

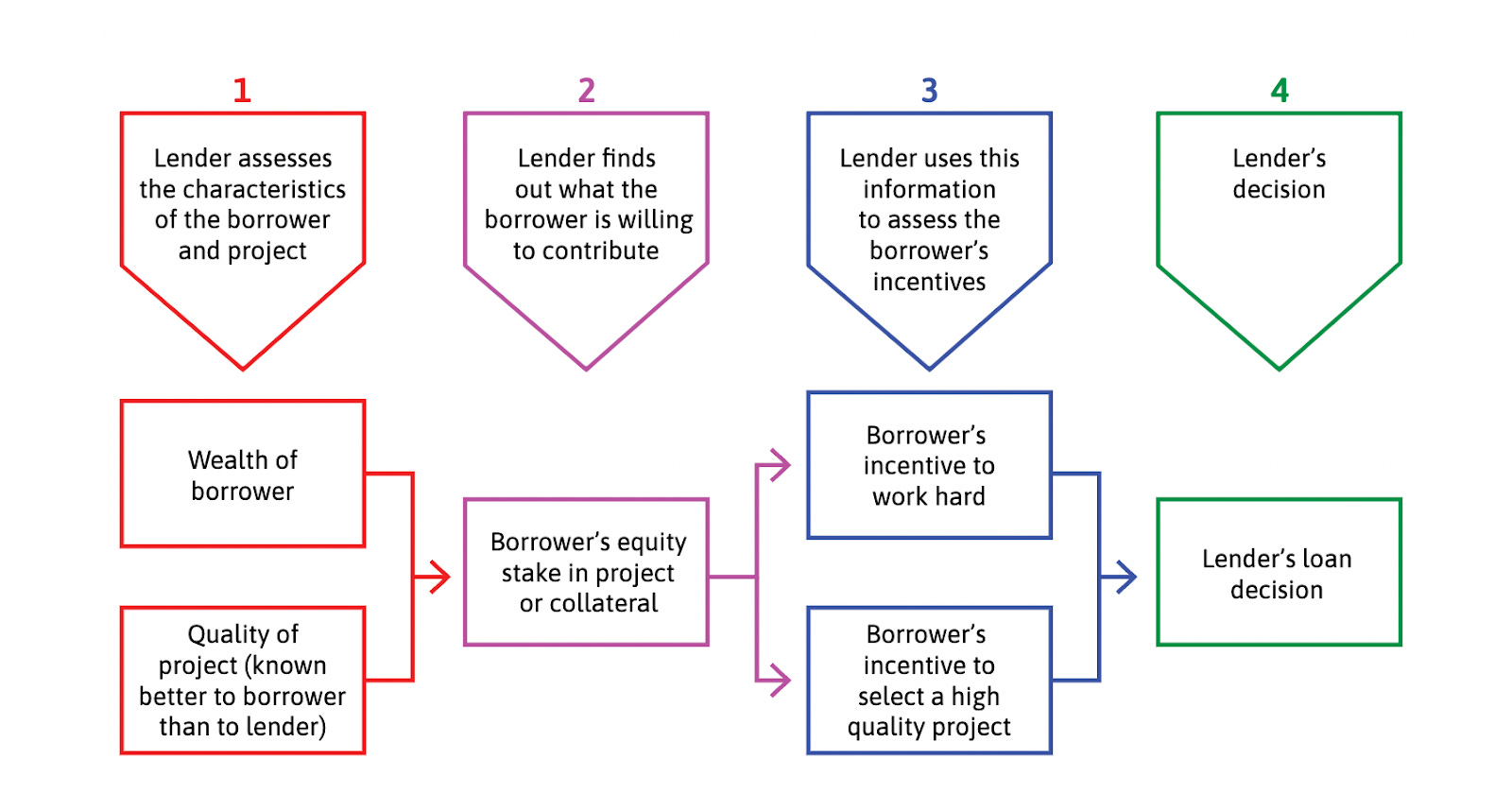

Secondly, the lending process involves conflicts of interest and information asymmetry between borrowers and lenders. Lenders cannot be certain that borrowers will make sufficient efforts to ensure the success of investment projects funded by loans. Additionally, borrowers may possess more information about the projects than the lenders, leading to adverse selection and moral hazard problems. Monitoring and enforcing loans under these circumstances incur additional costs, further justifying higher interest rates.

Collateral and equity requirements are strategies employed by lenders to mitigate the conflict of interest and reduce risk. However, this presents a dilemma for less wealthy borrowers, as they may lack the resources to provide adequate collateral or equity. As a result, they face credit rationing, borrowing on unfavourable terms, or being excluded from credit opportunities altogether.

The relationship between wealth and credit is summarised

What I’m trying to say is, lending is a business, run on the basic principles of economics.

Individuals with limited wealth face credit constraints that curtail their capacity to capitalise on investment opportunities available to those with greater assets.

Moreover, when it comes to determining the interest rate for borrowing, lenders typically hold more leverage, enabling them to establish rates that allow them to capture the majority of the mutual gains arising from the loan.

In essence, mutual gains denote outcomes wherein all parties involved experience a higher level of benefit as a result of their interaction, compared to what they would have achieved without the transaction (or, at the very least, some parties benefit without any experiencing losses).

Like other profit-making firms, banks are owned by wealthy people and they often transact on terms (rates of interest, wages) that may seem to be perpetuating the lack of wealth of borrowers. But the profitability of the lending also depends on the extent of competition among lenders.

And FinTech companies are worthy competitors.

Not just that -

FinTech solutions have been transformative in addressing financial bottlenecks and promoting inclusion.

I’m not saying that, the IMF is.

FinTech has successfully managed issues like high costs of delivering financial services in remote rural areas, information asymmetries among the unbanked population, complex documentation procedures, and the lack of suitable financial products for lower-income groups.

The FinTech revolution in India has significantly impacted the MSME lending landscape, providing smaller enterprises with access to credit through innovative alternative lending platforms.

During the pandemic, there was a remarkable surge in internet penetration and mobile device usage, a trend that is likely to persist and potentially accelerate in the post-COVID period.

This development has opened up significant opportunities for e-commerce and smartphone-based services, granting them access to vast amounts of data pertaining to individuals and small businesses in India. By capitalising on these trends, banks, in collaboration with FinTech players, have been able to provide financial services across various geographical and societal boundaries.

As more data continues to be digitised, the process of evaluating the creditworthiness of individuals and micro, small, and medium-sized enterprises (MSMEs) has become more efficient in terms of cost, time, and effort. This enhanced access to data enables financial institutions to make better-informed decisions and expand their services to a broader customer base, ultimately contributing to the growth and development of the financial sector in India.

I understand the scepticism around FinTechs, though.

Financial inclusion sounds like an audacious dream or even as an overly altruistic ambition.

But here’s the thing - much like any other business, FinTechs want to build and maintain a sustainable enterprise. They need to make a profit and ensure operations are viable.

That doesn’t mean FinTechs don’t have a genuine desire to uplift lives and bring even the most marginalised communities into the fabric of economic prosperity.

Both realities can exist simultaneously.

Sceptics may scoff, dismissing these ambitions as fantastical musings; but the way I look at it, we must embrace the scepticism as a challenge to prove that our aspirations as an industry are grounded in the firmament of reality.

After all, the financial inclusion curve is steep at first, but flattens out eventually. Much like everything else.

That’s all from me this week!

Cheers,

Rajat