These 5 indicators will spell win-or-bust for fintechs 2022

“The public have an insatiable curiosity to know everything, except what is worth knowing.” ― Oscar Wilde

I wonder if Wilde would even make the distinction between things that are/aren’t worth knowing had he been around. To see the year 2022 rollout was to see a new year emerge amidst a shadow of widespread fear, despair, and fragility across the world that’s as much economic as it is intellectual.

We truly lived through times where no news is good news. Except there was too much of it. Information, statistics, trends, and graphs - from those of unwell patients to that of vaccination status to those of macroeconomic stress. Yes, the last year did give us some positives - lots of new unicorns, technological and medical innovation, new economic thinking, and perhaps, also an overall sense of optimism about our own future (if we can make a vaccine in six months, what can’t we do?).

However, as the old saying goes ‘man proposes, god disposes’ - it’s impossible to really know what this year has in store for us - but it doesn’t mean we cannot be cautiously optimistic.

To that end, I decided to create my own set of benchmark indicators for this year that has the potential to define and change the trajectory of the lives of a billion Indians.

Without further ado, let’s look at these and why it’s important to closely track them in order to gauge the impact of all this innovation. Stories are dime a dozen as of now but only hard numbers tracked intelligently can indicate if there’s a resultant orbit shift through all this innovation for the typical (not average by any means) Indian.

Digital payments have attained velocity, depth is next

Despite hiccups such as market share limitation and zero to low MDR regimes that the digital payments space is currently battling, the rate of adoption has been stratospheric.

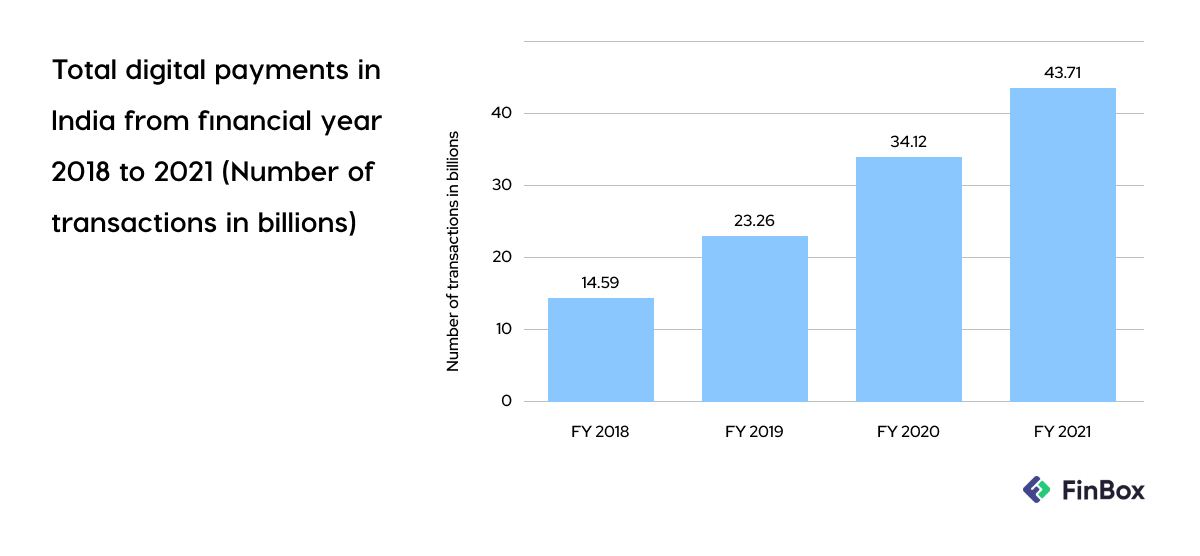

Digital transactions saw a 53% increase in volume over the last 12 months. UPI payments account for a major chunk of these transactions as they increased to USD 16 Bn a month - almost equal to merchant payments done via debit and credit cards combined.

Be it UPI apps, QR codes, or the government’s concerted push towards digitizing the economy - the digital payments wave is one that has not just continued but grown stronger with every passing day.

However, a lot of work is still undone. The depth is certainly still missing with a bulk of digital payments value coming from large-scale interbank transfers such as RTGS or NEFT.

In fact, in FY 2021, digital payments in India amounted to over 1.4 quadrillion Indian rupees in total. This was a decrease compared to the previous two years, when the total value stood above 1.6 quadrillion rupees, respectively.

While UPI etc are taking hold along with BNPL making its mark in Tier 1, 2, and 3 cities, there needs to be a broad-based inclusion of the populace at large in the digital payments regime.

While most Indians shopping on the likes of Amazon pay digitally, one should track how many of those beyond the metropolitan areas are able to pay their electricity, water, and other bills online. That's when you know Bharat is digitizing, not just India.

That’s the key indicator and for me, 2022 will be a defining year if both volumes and value pick up in digital payments mediums especially in UPI, credit and debit cards, etc. At the same time, I’ll be tracking the average transaction size across payment mediums as well as the average wallet share of digital payments for an individual household vs offline payments.

Source: https://www.statista.com/statistics/1251321/india-total-volume-of-digital-payments/

Despite the digital blitz, cash is still king…

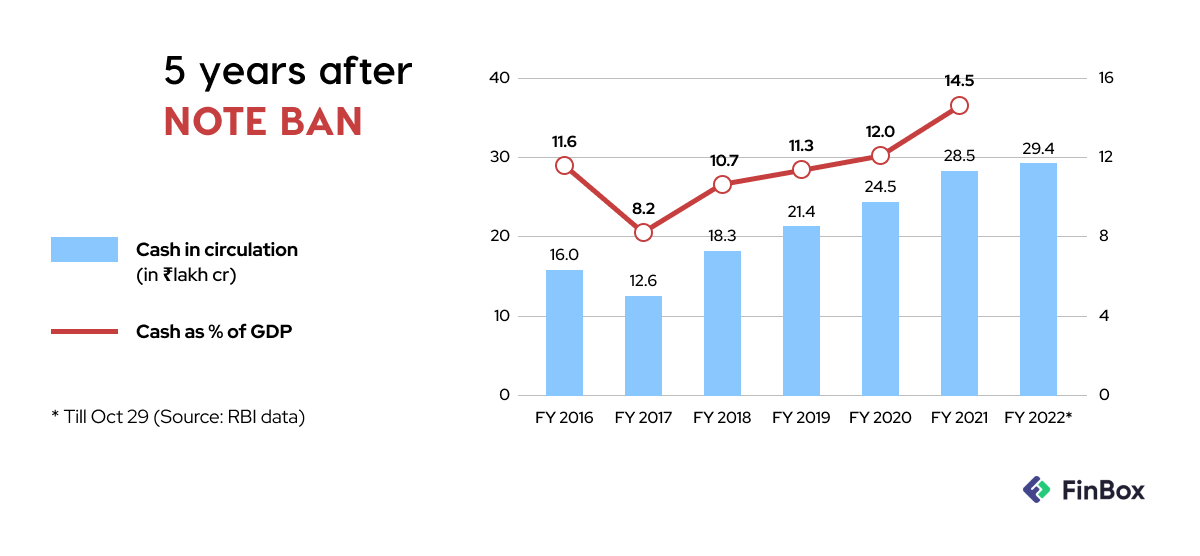

The ratio of currency in circulation as a proportion of the GDP touched a high of 14.5% for fiscal 2020-21 - and this isn’t a one-off. Data from the last few years shows that cash in the system has been rising steadily since 2017, hitting its peak in 2020-21 fiscal as people rushed to hoard cash in the face of COVID-induced lockdowns.

The truth is though, that COVID only exacerbated an existing lack of financial inclusion. Almost 15 crore Indians still don’t have a bank account, and even for some that do, digital payments are inaccessible and/or hard to understand.

To be fair, cash isn’t the devil that we need to fight but it’s the shadow economy that seems to follow it. With more digitization and formalization of businesses across the country, the cash-to-GDP ratio is bound to come down and that’ll be a more meaningful metric to track rather than just looking at the brighter digital payments numbers.

Source: https://timesofindia.indiatimes.com/business/india-business/cash-in-use-now-at-record-14-5-of-gdp/articleshow/87574005.cms

Could 4G be the answer?

Statistics sometimes tell you the story you want to hear - and that’s especially true when it comes to internet access in India.

On the one hand, 4G has reached close to 80% of Indians - but on the other, over 25,000 villages in India lack any sort of internet connectivity whatsoever.

But 2022 could be the year things change. Its financial troubles notwithstanding, the state-owned Bharat Sanchar Nigam Limited (BSNL) is likely to finally roll out pan-India 4G services by September.

While smartphone adoption has taken off across the country - 696 million Indians have access to smartphones, and 560 million of them are online - the proliferation of high-speed internet in the form of 4G could be a game-changer for financial inclusion.

How? Because with faster internet speeds comes the ability to download and use more applications and that opens up use cases hitherto locked (think cryptocurrency, equity markets, online PPFs, mutual funds, etc).

For instance, investment, expense tracking, neobank apps, etc are all relying on an increase in high-speed internet users who are set to increase their consumption of data to 40GB per month by 2026 (it could happen a lot sooner if the 5G rollout happens on time).

Will digital subsidies reach more Indians this year?

The government’s Direct Benefit Transfer (DBT) is aimed to transfer subsidies directly to the people who need them through their bank accounts. This checks both the leakages in the system and also improves the overall efficiency of subsidy delivery by cutting down on logistics, personnel, and large program management costs.

FY 2021-2022 saw over 4 lakh crore transferred to beneficiaries. A number of schemes are covered under DBT (312 schemes from 54 ministries) and this year, the government planned to shift to DBT to deliver fertilizer subsidies but put this on hold given prolonged farmer protests and impending elections in five states.

Had it been implemented, subsidies would have gone directly to farmers' bank accounts (as opposed to the current system where it's transferred to fertilizer companies for farmers to purchase at lower prices). This would have helped bring down frauds, promote accountability, and plugged the misuse of public funds.

While DBT sounds good on paper and has resulted in immense cost savings for the government, its downside is that it creates a strong dependence on the banking system, especially for those who traditionally have not had access to it. While the Jan Dhan Yojana was linked with Aadhaar to solve this problem, the truth is that about 6 crore Jan Dhan accounts are dormant.

The only way to increase access would be to work not just with scheduled banks, but also with rural regional banks and other last-mile banking correspondents networks to not just enable access to banking but also access to social welfare funds that so many citizens depend on.

I will be closely tracking both the depth of banking service usage in rural areas as well as the digitization of subsidies and welfare schemes delivered to the citizens this year as a proxy for the overall status of financial digitalization in the country.

Will the Account Aggregator (AA) framework have its UPI moment this year?

According to Sahamati, close to 80,000 accounts have already been linked to account aggregators, and 65,000 consent requests were fulfilled as of the first week of January.

At FinBox, we were one of the first in the industry to launch Account Aggregation as part of our underwriting offering and the response has been nothing short of phenomenal.

All the signs point in the right direction, and this could be the year AA truly comes into its own - once the few wrinkles are ironed out. Large public sector banks are yet to come on board, which means that a bulk of rural India is yet to experience the benefits of AA.

Most banks that are already leveraging AA are doing so to disburse only smaller loans. Increasing awareness of the framework is the need of the hour and can be done with lenders and AAs collaborating to launch marketing and informational campaigns.

UPI too was initially met with a lukewarm response, and slowly picked up. With the right efforts, that could be the way the AA story turns out as well. If so, it’ll be the ultimate game-changer for the financial services sector as products like credit, insurance, and investments will open up to millions of unserved Indians.

Bonus:

Apart from the above, it'll be interesting to track other catalyst indicators such as credit growth to the manufacturing sector, digital loans originations, insurance penetration as well as other adjacent metrics such as ARPU for telecom companies and smartphone sales numbers.

Is there anything else that you'd be tracking? I'd love to hear your thoughts.

Once again, have a great year ahead. Attaching a great whitepaper about Financial Inclusion for your reading pleasure below.