Terrible collections will bring down even the best lenders.

Terrible collections will bring down even the best lenders.

Two FinTechs. Same offering. BNPL at checkout for food and grocery delivery apps.

However, when it’s time to pay, one lender bombards the customer with automated calls while the other sends a friendly text reminder every two days.

Guess who sees more customer churn?

Let’s start from the beginning.

A FinTech provider pours their heart and soul into a product that incisively addresses customer pain points, builds a kickass interface, makes loan applications flow like water, and the whole nine yards. The loan is disbursed within a matter of minutes, if not seconds. Happy ending for everyone!

But what’s to come after the end credits roll?

For borrowers – dodging pesky calls from collection agents, the unrelenting dread of messing up credit scores, and complex repayment methods. For lenders – a grueling cycle of reminders, rude and polite.

Unfortunately, collections are meted out step-motherly treatment even in digital lending. The consideration and attention to detail for onboarding, application and disbursal workflows has not been extended to the heart of the lending business – recovery.

Collection practices are still steeped in archaic communication channels, predatory recovery operations, and a complete dissonance from the needs of the customer.

The lean, mean innovation machine

FinTechs are constantly innovating on how credit is distributed. Whether it’s by tapping into deserving yet ill-served customer groups, the use of alternate data underwriting, rolling out innovative products like BNPL, or their approach to fraud management, lending today has become unrecognizable from until a decade ago.

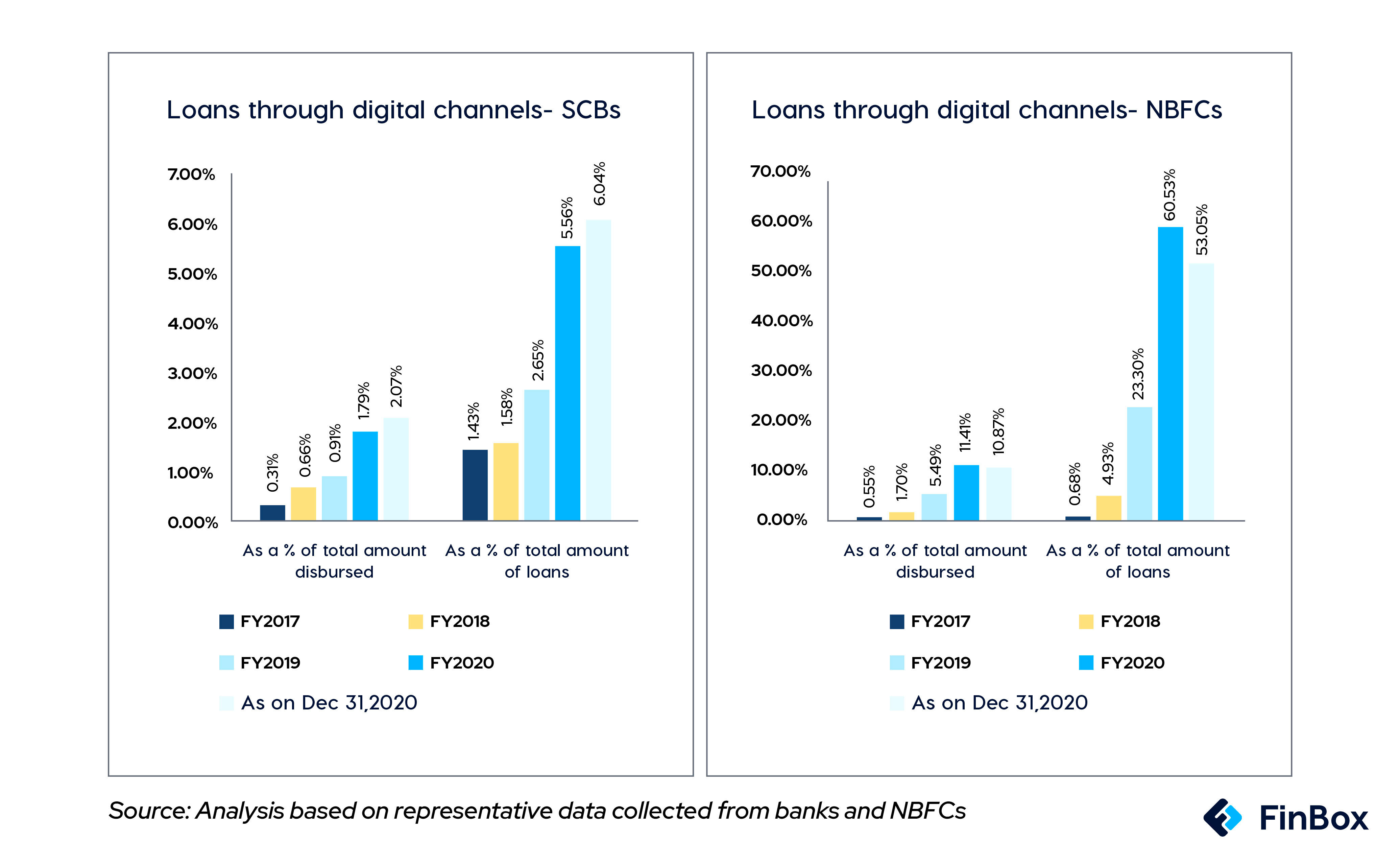

But more importantly, FinTechs have reimagined the ‘how’ of lending. When wooing a customer, digital lenders will roll out the red carpet, whether it’s host platforms or end users. APIs for easy integrations, state-of-the-art consumer interfaces, adaptive onboarding and checkout journeys – you name it, FinTech’s got it. As a result, customers are warming up to the use of digital channels to get a loan. In FY20, digital loans made up around 6% of all loans disbursed by scheduled commercial banks and a whopping 60% of loans sanctioned by NBFCs.

However, a darker trend has accompanied this one. When it came to collections, a number of lending apps resorted to harassment by contacting their relatives and employers, threatening with legal notices and even fake pornographic content. In fact, a number of suicides have been traced back to these practices.

Collections are considered a necessary evil, to be carried out once the good part is over. Debt recovery, as necessary as it is to business, flies in the face of quality customer experience. Loan defaulters are protected by a number of rights. And lenders who breach these risk hurting their reputation or worse – legal action.

Collection differs from other lending activities on one fundamental parameter – it can’t be done without a human touch. Digital lenders who choose to take this in their stride and tweak their workflows can make their collections more successful.

Intent and ability

Answering one simple question can bring lenders a lot closer to aligning their collections strategies to better suit their customers’ needs –

Why do people default on loans?

It could be one of two things:

a. Because they cannot pay due to extenuating circumstances.

b. Because they do not wish to pay back.

Let’s explore reason a. Customers could simply be hard-pressed for funds to repay their loans, lacking the ability to repay. A McKinsey study found that poor money management was a leading cause for delinquencies. It also concluded that respondents were indeed motivated to repay – they wanted to maintain good credit scores and honor their commitments.

The second kind of borrower is the opposite of what traditional economists dubbed Homo economicus. They do not have the infinite ability to make rational decisions that are in their self-interest – like paying off their debt.

For whatever reason, these borrowers are likely to commit wilful default. For example, there’s a psychological need in humans to exercise their agency. Around 20% of the respondents in the study said that they withheld payments after getting upsetting calls from debt collectors. Even though these customers had the ability, they lacked the intent to pay.

Evidently, collection is a business of human interactions. Tech innovations cannot replace behavioral recovery operations, but simply augment them.

Behavioral segmentation

So far, customer segmentation is riddled with the problem of homogenous delinquency buckets. This 15-, 30- or 60-days delinquent approach views customers as figures on a computer screen, failing to account for individual circumstances and experiences.

With a combination of empathy and data intelligence, lenders can personalize these ‘buckets’ as well as the ensuing treatment for each customer. They could leverage real-time data and machine learning to preempt the probability of default for each case, creating segments of one.

They could also use data to make sub-categories within at-risk groups, or take a value-at-risk approach to prioritize collections from high-risk high-balance customers. We’ve explored the subject at length in our blog here.

Contact strategy

With a finger on the pulse of delinquents and defaulters, lenders can carefully tailor their contact and messaging strategy for each customer. There are many ways to alter communication and influence customers to make a favorable decision.

Communication channels

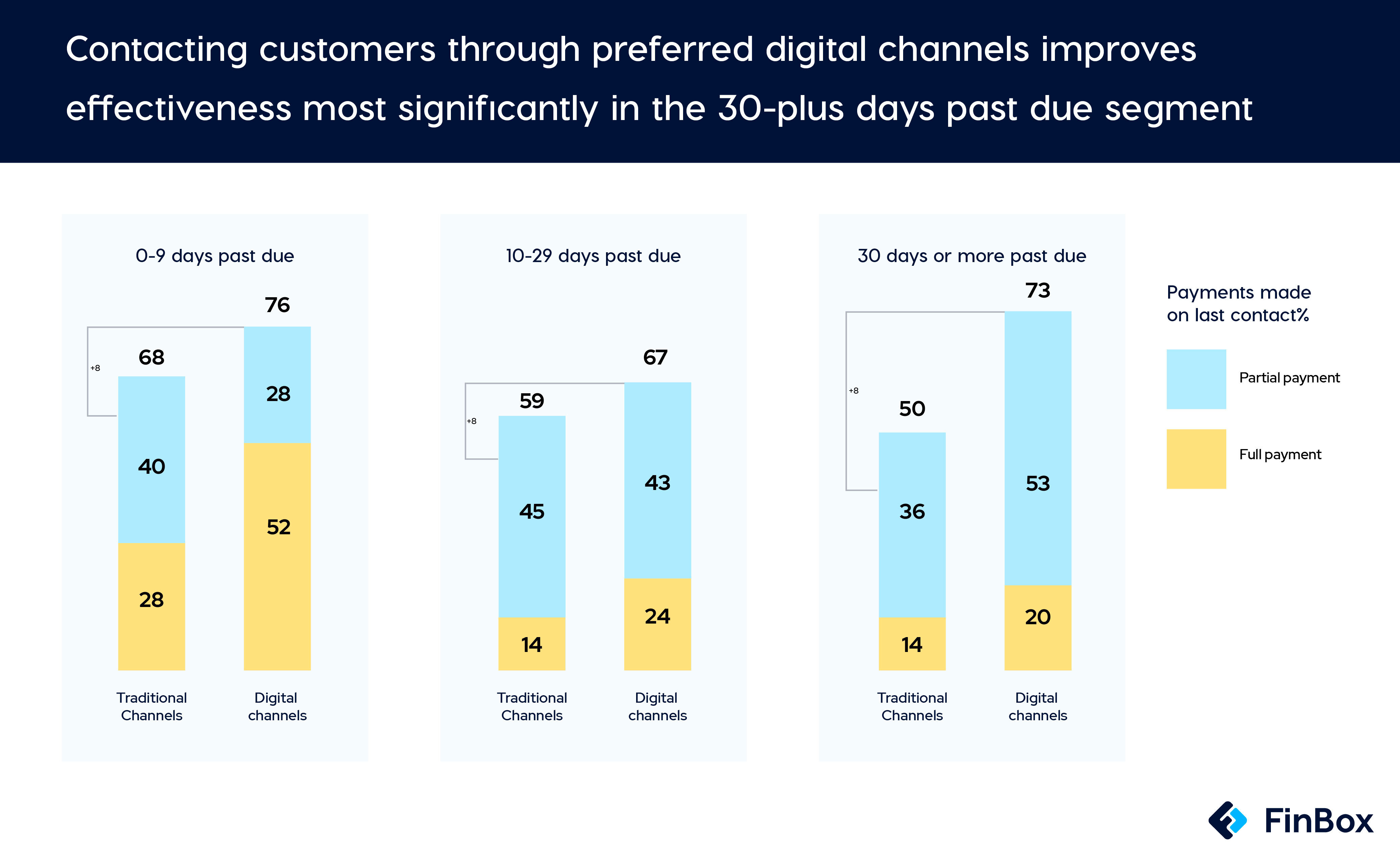

When the rest of the loan journey occurs digitally, it’s jarring to break the flow and hound customers via phone calls or at their doorstep. Instead, escalate communication channels based on individual risk profiles. Go from in-app notifications to text messages, then phone calls and finally physical contact.

Remember the psychological need for control? Unsolicited, aggressive contact via an undesirable channel will only antagonize customers, even if they intend to make the payment.

Elicit cooperation

Collectors must take a page out of the salesman’s playbook and increase the chance of repayment with psychological interventions at four crucial moments during a conversation: opening, committing, negotiating and following through.

Collectors can create a positive space upon establishing contact, ensuring the customer is more receptive and open to finding a solution. Next, keep the customer engaged to ensure they commit by, say, offering a solution popular with other customers (herd-effect) or offering a customized repayment plan. Finally, easy repayment options and prompt customer service can encourage customers to follow through.

Choice architecture

You can take the horse to the water, but you can’t make it drink.

Building a choice architecture does exactly that — points the customer towards making a favorable decision. For example, tweaks to the user interface can display desirable choices and omit unfavorable ones to nudge customers towards repayment. The language and tone of voice in communication, as well as the user experience can also nudge unwilling customers in the direction of repayment.

Real-time insights

Data insights from the underwriting stage continue to be used during collections. Customer behavior is not static so by this time, this intelligence becomes redundant – whether it’s bureau data that can be accessed only after a lag of 60 days, or alternate device data.

Through timely portfolio monitoring with the use of analytics and behavioral segmentation, lenders can anticipate upcoming delinquencies and prepare their contact strategies accordingly. The result?

By some estimates, a 20-25% reduction in NPAs, 25% increase in resolution rate, 15% less collection costs and 5 times the present customer engagement.

The long and short of it

No amount of innovation can help collections if there isn’t a mindset shift in digital lending. Instead of treating debt recovery like reluctant wetwork, it should be viewed as an opportunity for building positive customer relationships based on deep understanding of human behavior.

In fact, as they work through consumer behavior issues, lenders should address their own biases and heuristics resulting from fatigue that may tank recovery efforts.

Such a patient, understanding and forgiving approach to debt recovery built on the foundation of psychological evidence is the only sustainable way to reinvent collections. And it’ll need a careful crafting of the right products that ensure collections without hampering customer experience and turning you into a pariah.