Shot in the arm, or in the head?

How Budget 2022 will bode for MSME financing

The run-up to the budget is usually an exciting time, both in terms of expectations and wracked nerves. The latter more so in the past two years, with the pandemic bringing economic activity to a screeching halt in 2020. But if numbers give comfort, India’s GDP growth is set to be world-beating and estimates for tax collection predict a four-year bump.

All thanks to the government and the Reserve Bank of India (RBI) firing on all cylinders to keep the economy from tanking. From reining in borrowing costs at 4% for the past nine quarters to sanctioning Rs 2.9 trillion via the Emergency Credit Line Guarantee Scheme (ECLGS) till November 2021 - the singular focus on India’s growth engines, namely the micro, medium and small enterprises (MSMEs) - has come to bear fruits.

The ECLGS - a 100% government-guaranteed scheme with no processing fee - has helped stressed MSMEs tide over working capital crunch during the lockdown. A study by TransUnion CIBIL (ECLGS Insights Report, December 2021) shows that 45% of the ECLGS loans were used to clear vendors, 13% for paying salaries and 29% to restart operations.

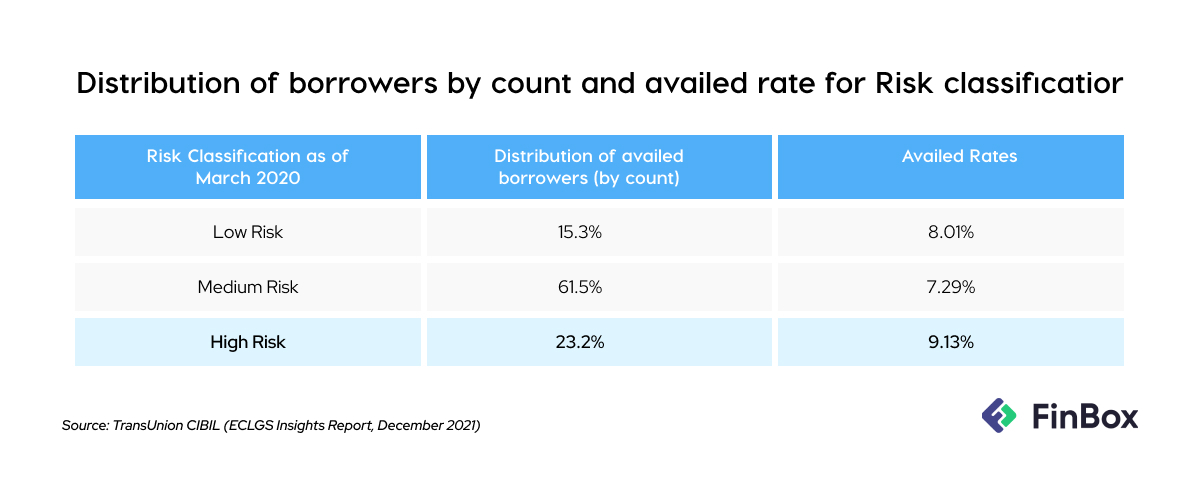

More so, the ECLGS becomes a departure point for credit to MSME story. It has improved credit penetration in the sector that accounts for 30% of India’s GDP, helping banks revisit the entire creditworthiness narrative. Data shows the scheme was specifically beneficial to medium- and high-risk borrowers, where bank credit had been negligible since time immemorial.

This also bears testimony to the role fintechs have played in bringing risk assessment models of age. Although, the MSME credit gap is far from being addressed, the scheme has catalyzed the flow of formal credit to the small, medium business sector - ushering in better NPA management (only 2% of ECLGS loans are reported as NPA), improved credit health of borrowers (indicating a movement from higher risk bucket to lower), and improved economic prospects with 68% of MSMEs surveyed in the TransUnion CIBIL report anticipating a positive future outlook.

Credit where it’s due

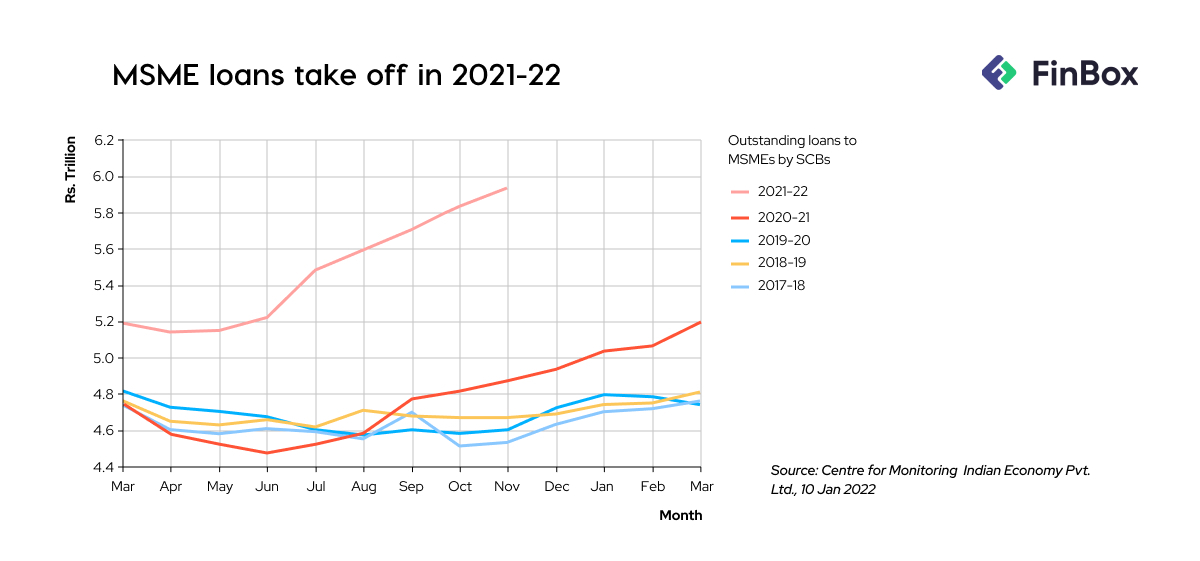

This should also, in part explain, the bank credit offtake for the past year, in spite of overall credit growth moderating at eight percent. As per Center for Monitoring Indian Economy, the average monthly outstanding scheduled bank credit to medium-sized industrial enterprises during April-November 2021 is 43 per cent higher than it was in 2020-21. See it for yourself:

But the other part of the story - apart from the ease of financing access - is the genuine growth in the MSME sector and a true demand for credit fueled by upward-looking business prospects. The opening of bank credit may have spurred the slow-turning wheels here, and this sector may be gearing up for growth in an environment where industrial and corporate spending remains muted.

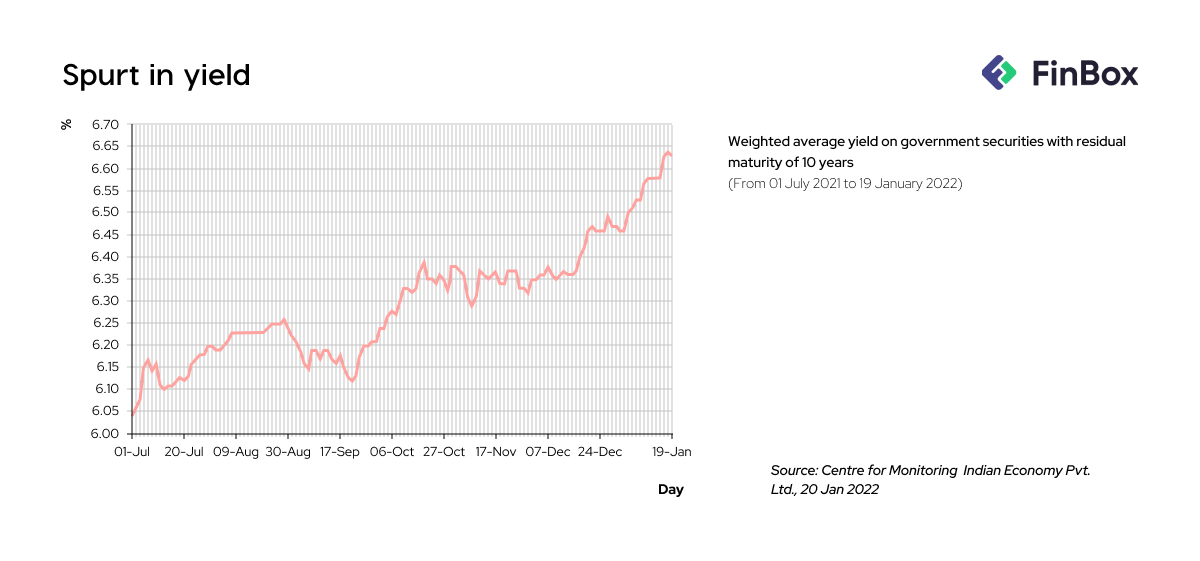

But while growth is on the agenda, so is inflation. Keeping the economy flushed with liquidity - pegged at Rs. 8 trillion per day - for protracted periods goes against the grain for the inflation-targeting RBI. But for all that, State Bank of India and HDFC - the behemoths for public and private sector respectively - have increased rates across products, effective January 12, 2022.

And now with rumours gaining fervour for the U.S. Federal Reserve tapering due in March, the chorus to increase rates will grow louder.

And once that happens, maybe the sheen of easy to come by credit will wane, a little, which could be a lot for the kirana store that availed loans under the ECLGS.

The Budget: Bumper or Bummer?

The ECLGS was rolled out in March 2020 with the limited availability. It was extended in 2021, and now with a third wave underway, speculations are ripe for another extension. That’s the budget expectations across NBFCs and fintech players serving the MSME sector.

There have been calls for tax rebates and further concessions in use to technology to enhance underwriting and risk assessment models. These sops will help streamline the credit flow to MSMEs, but nothing as stellar could be delivered in such a short term as seen this year.

Given this is an election-year budget, it could border on a populist skew - lowering taxes, easing credit options and stoking consumption. But the government will have to balance these expectations with fiscal targets, as has been voiced by cautionary voices across expert panels.

Our two cents - a granular look at liquidity flow will help the government deliver sustained policy benefits to those in need. As for the ECLGS, if continuing seems improbable, maybe a staggered roll back should cushion the free-fall.

For now, all eyes on February 1.