After years of dodging with India’s non-banks, the Reserve Bank of India (RBI) may finally be warming up to NBFC credit cards. The RBI’s new guidelines, a master circular of its old ones, triggered debates on whether non-banking financial companies (NBFCs) will finally be allowed to issue credit cards.

Here’s the thing though - it’s old wine in a new bottle. The new directions don’t say anything differently for NBFCS. Since 2004, the RBI has told NBFCs in many periodic circulars that they could launch credit cards - they just had to take its permission first.

So what’s different this time around?

Rules mainly to protect customer interest and rein in the misconduct of card issuers. And more importantly, the timing. The RBI’s scale-based regulation will take effect from October this year. Basically, NBFCs will be categorized based on their size and the top tier NBFCs will be regulated like banks.

So if NBFCs are regulated like banks, they should also be allowed to sell products that banks do right?

But do NBFCs even want to?

Let’s take a quick look at credit in India

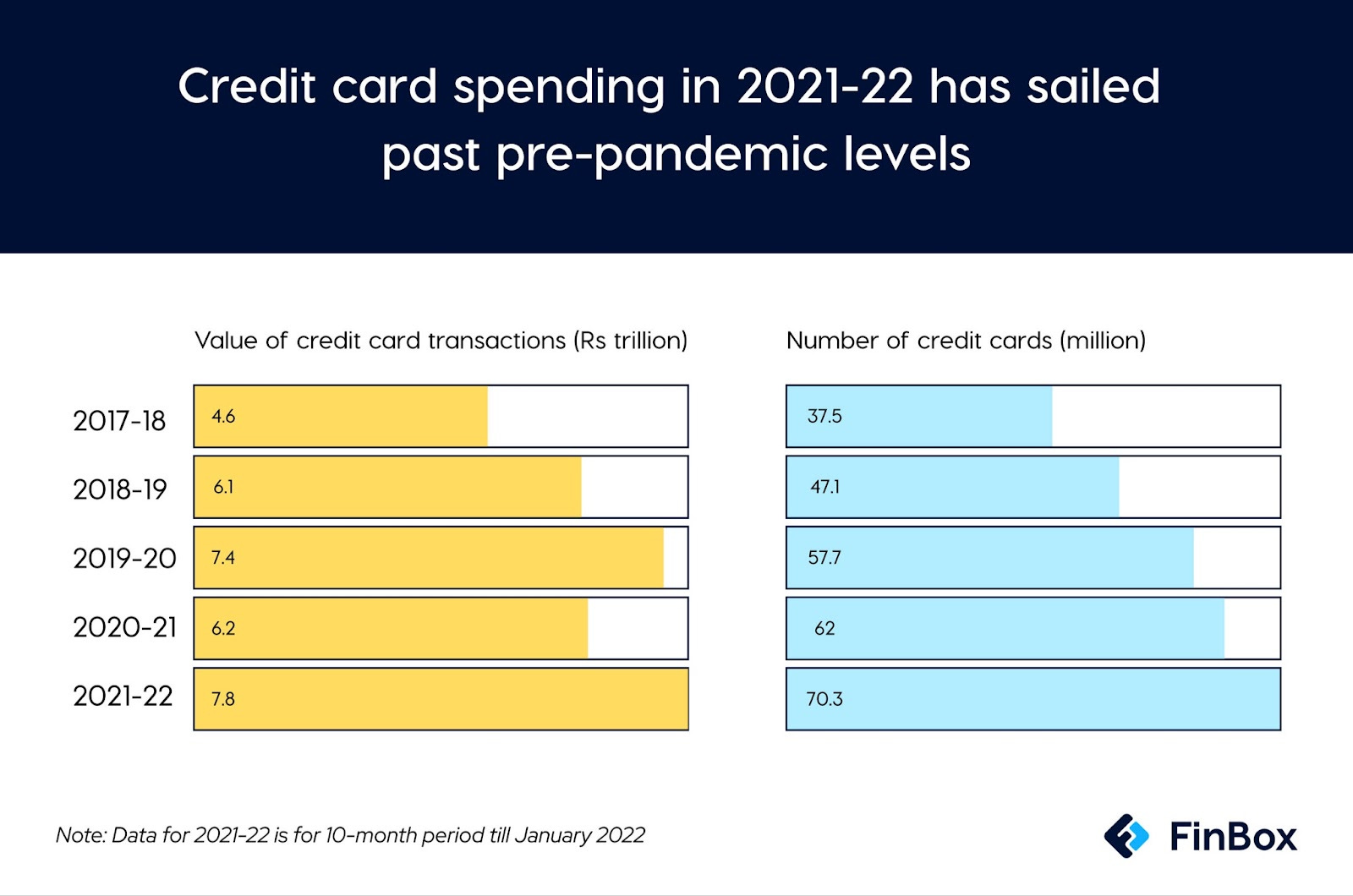

Nearly a decade ago, the value of cash-based transactions in India was close to 70%. In more developed economies, it stood at 20% for the US and 11% for the UK. Back then, it was fair to assume that, much like the west, India would move to plastic money.

And it did - as of January 2022, there were 940 million debit cards and 70 million credit cards. While the number of debit cards are higher, credit cards dominate in transaction value.

Credit cards have grown 87% in the last five years. And yet, it's a sunrise market - overall penetration remains at just 5% of the country’s population. That means there’s plenty of room for more players.

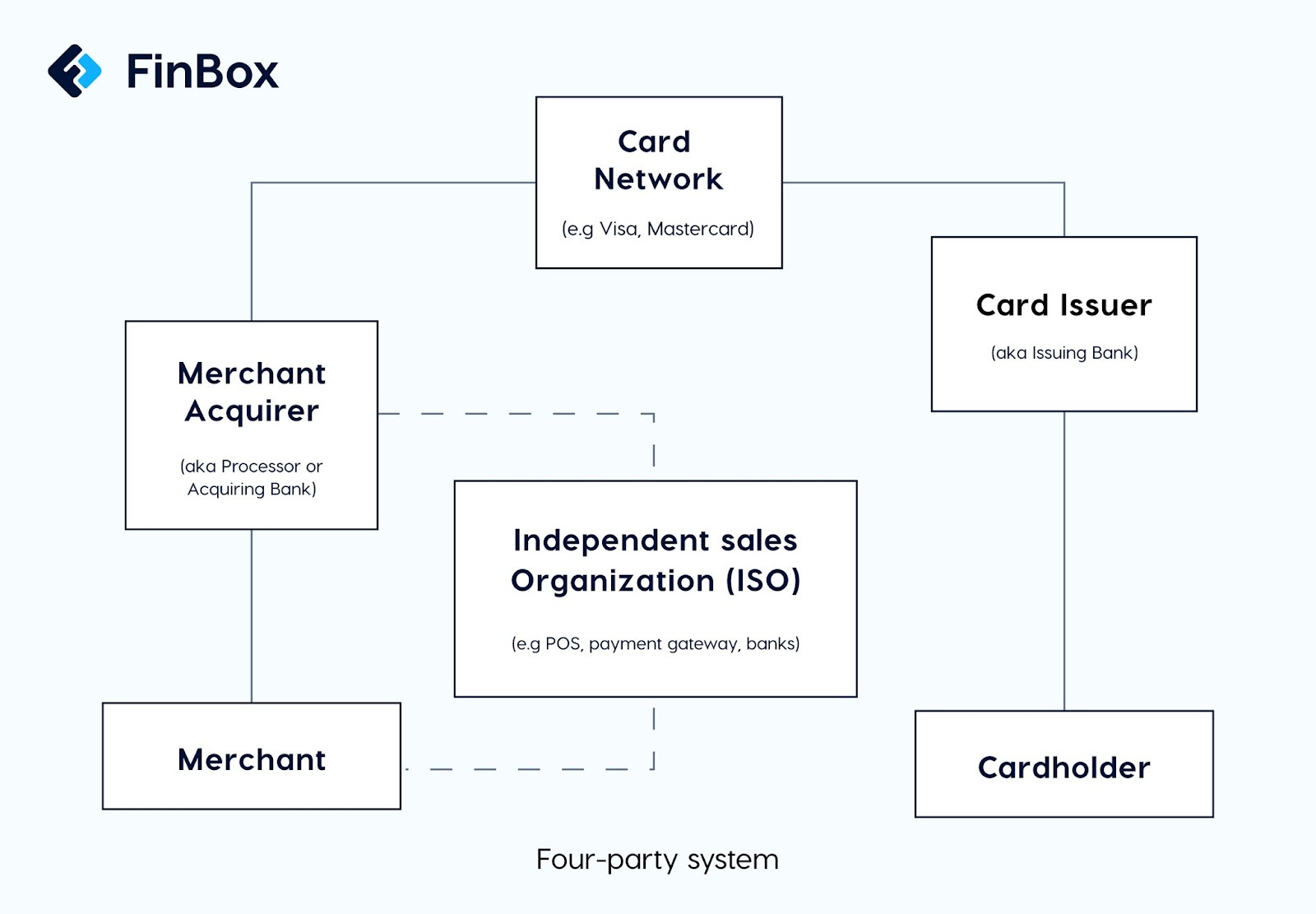

The card ecosystem as it is -

The global electronic payment processing industry has two large players, Visa and Mastercard and a few smaller players, Amex, Discover and JCB. The larger players partner with local banks to issue cards

The Card ecosystem is a four-part system with the following players -

Merchants are charged for every transaction that involves a card (Merchant Discount Rate or MDR) and the proceeds are shared by the card network, the card issuer and the merchant acquirer

Customer acquisition cost (CAC)can be anywhere between Rs 2,000 to Rs 4,5000

This Economic Times article brilliantly summarizes the economics of why the credit card business is lucrative - a Rs 4000 CAC and a post-tax earning of 2,700 means reaching breakeven in 1.5 years. Sounds bankable right?

However, the credit card business is just as expensive as it is lucrative

NBFCs face a setback of charging a higher interest rate and processing fees due to their easier and more convenient financing options

Over 50% of the cards are not activated within the first 90 days of issuance. With RBI’s new guidelines suggesting a 30-day window for activation, it might render the Rs 4000 Customer Acquisition Cost futile

NBFCs face a higher cost of capital compared to banks, which can simply tap into their CASA (Current Account and Savings Accounts) pool of funds.

The Merchant Discount Rate (MDR) - the fee-sharing structure among the multiple parties involved in a credit card transaction - means that NBFCs will do little more than pocket this inflow

With the RBI pondering over capping the MDR, it might put downward pressure on earnings

Second, asset-quality challenges presented by new-to-credit customers, who have driven significant growth for NBFCs might also act as a potential pressure point on earnings

Underwriting for credit cards is very different from what NBFCs are typically used to for unsecured loans

The entire credit limit needs to be considered as a loan, rather than the amount spent. Capital allocation can get tricky - especially since NBFCs borrow from banks to lend. And unless their borrowers don’t pay back at a temperate pulse, repayment structures can get complicated.

More than 160 million Indians are credit underserved; if non-bank credit becomes a reality, it could mean an explosion in access to credit. But NBFCs are already doing it - Buy Now Pay Later (BNPL)-type credit, or use prepaid cards to deliver credit. These products are already similar to credit cards but come with limitations.

The rules have been the same all along and yet a majority of NBFCs haven’t applied for a credit card license. And it’s obvious why - credit cards are an elite product.

Credit card penetration is as low as it is in our country because banks don’t have the stomach to issue credit cards beyond the top earners. Besides, credit card loyalty works on rewards, discounts and loyalty programs - this is on top of the hyper-personalisation that’s needed to lure in customers from different segments of the country. For an offline, process-heavy industry like credit cards, it just means wafer-thin margins for NBFCs.

The way forward

NBFCs should think about their business model and roadmap before jumping on the cards bandwagon

Cards are going to be eventually replaced with personalized virtual credits - BNPL etc and those are better, less risky bets - because revenue is clear

NBFCs diversifying into credit cards and other forms of credit would do well to evaluate their technology stacks and partner with the right solutioning companies (such as FinBox) to ensure they just don’t launch a fancy looking product but one that comes with a business model too.