Lifetime products, not lifetime marketing

Fintech: The diamond in the rough that shines

Hi,

One of the most common criticisms levelled against fintech is that beneath the multiple layers of slick user experience, nimble underwriting, and petabytes of data analyzed in under minutes are startups burning investors’ money in search of a profitable business model.

And in typical fintech fashion, I’d like to think that accusation is layered. For one, technology can be intimidating; add a layer of the one thing that’s most dear to people (money) and it becomes threatening. Understandable. But not fair.

When I think about what drove the digital revolution in our country, it often strikes me that financial inclusion was always the nucleus. We began with ramping up the number of bank branches and ATMs, Priority Sector Lending (PSL) was introduced, and MNREGA was put in place, among many other initiatives. But none of this would have been possible without a bank account.

Enter Aadhar - India’s unique ID project and the base layer of India stack’s ambitions. The biggest ambition of the India stack was to create a digital identity for Indians and allow them to do anything they wanted - open a bank account, get a credit card, invest in mutual funds, hire a cab, change their mobile operator, share a bicycle. Practically anything.

That was the identity layer.

Then came the payments layer - UPI - a pivotal moment in the India stack story. UPI was easy - it runs on the core mechanisms of IMPS. But what UPI did was add wrappers on top of its core technology (APIs). Only banks would be allowed to directly access UPI’s APIs directly, so startups would need to find a bank willing to license it as an SDK. This allowed fintechs to deliver superior UI, UX and consumer experience at scale.

And then came the data layer - the account aggregator.

Much like UPI filled the cash-starved void created by demonetisation, the Account Aggregator framework was created to fill the cash-starved void in the MSME sector.

The biggest ambition of the India stack now? Creating a critical mass of data on each user.

The digital rails of the India Stack provided as a public good and letting startups build on it is what has made fintech possibly the most revolutionary industry.

The simplest definition of a revolution is an abrupt change in social/ economic /political order.

Let me contextualize it -

Even as recently as a decade ago, small business owners were caught in an unfortunate gray area - too small to be worth the attention of banks’ corporate lending divisions and too complex to be served by banks’ consumer lending divisions.

But fintech changed that. My colleagues have written a bunch about how the industry is fixing the MSME credit gap, one crevice at a time. You can read them here, here and here.

(There’s more on MSME lending on our blog page. Click here, maybe?)

The value proposition is clear - trained on millions of data points, the AI/ML models created by fintechs can bring previously baulked sectors into formal lending.

What next then? Contextualize further.

Think about what UPI did - swift, interoperable, near-instant transfer of money, and cheap, it took the digital payments ecosystem to unprecedented heights in India and across the world. So much so that billion-dollar companies like Google flocked to adopt it.

What UPI essentially did was render payments to commodity status. Payment companies took payment data from UPI and ran with it to bring more services - from wealth management to lending.

They took the data and contextualized it. Radical.

Like payments, several non-bank players are already contextualizing lending. Uber recently partnered with Moove to offer accessible vehicle financing exclusively to drivers on Uber’s platform. Shopify offers a couple of hundred dollars to merchants as “starter capital” to spend on expenses like branding, ads, and inventory. They’re paid back as a fixed percentage of the merchant’s revenue over a 60-day period. Not only is it a low-cost acquisition tool for Shopify, but even if merchants don’t pay back the loan, Shopify still finds an out thanks to the fee for every transaction made on its platform.

Radical.

India’s radical lending moment will come from the deeper adoption of the Account Aggregator framework.

Still, in its early days, the AA framework would throw data in a raw form, and lenders would need to build credit analytics on top of it to underwrite, and all that work is being done as you read this.

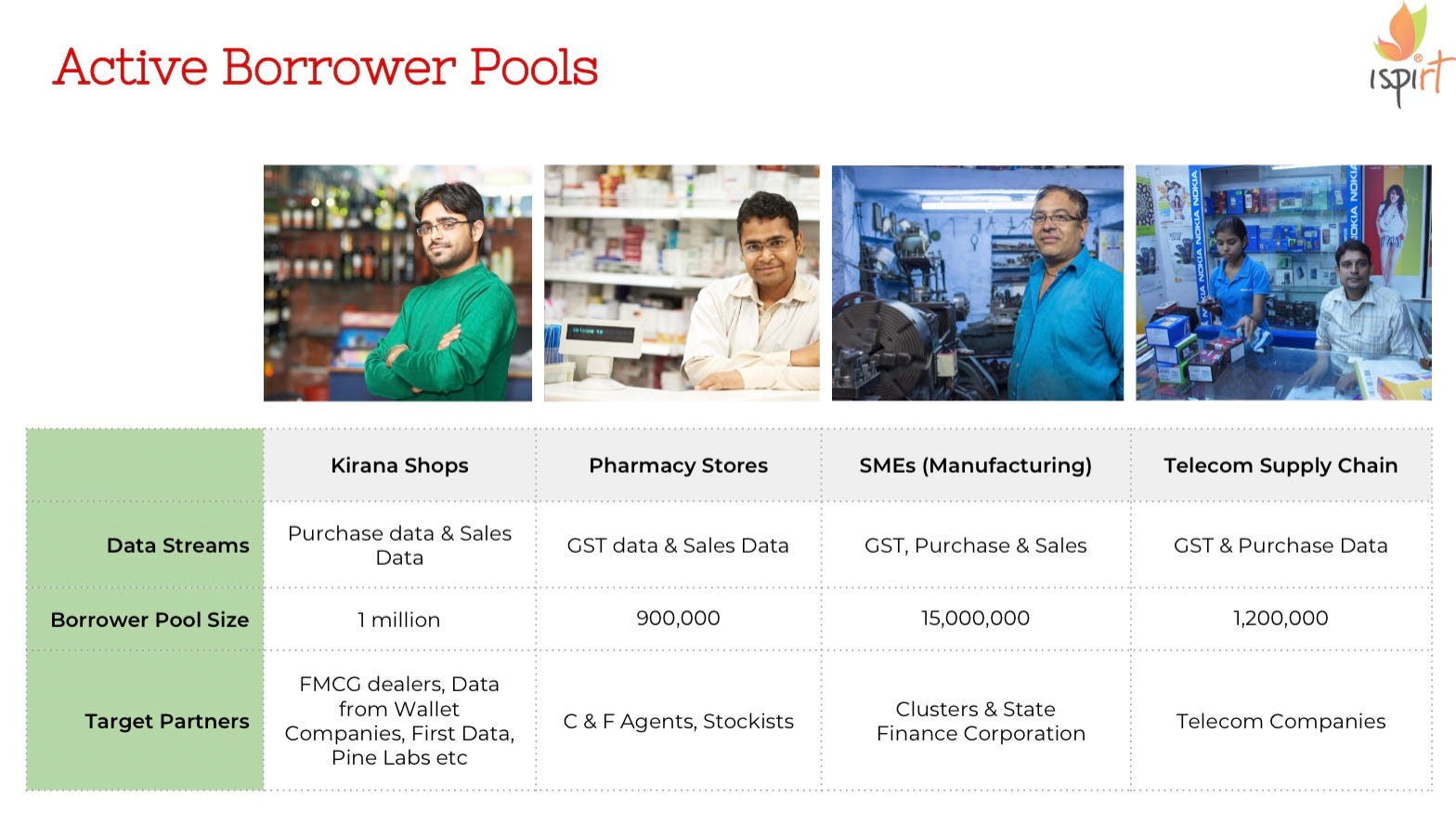

This graphic in Ispirit’s ‘India's Digital Leapfrog and its impact on Digital Financial Products’ report sums up the kind of raw data that the AA framework could potentially produce -

And think about the contextual loan products that could be built on top of this; customisations can be based on cash flow, checkout financing, loan tenure, specific borrower segments, and loan against future cash flow. Underwriting gets sharper, customer acquisition gets cheaper and the risk of default much lower.

This PwC report gives a comprehensive take on what the evolution of AAs will look like towards developing revolutionary products and services

Every digital transaction we make, we leave digital footprints. This data is already leveraged by fintechs for stronger underwriting (FinBox’s DeviceConnect for instance processes device data to bring several new-to-credit borrowers into the formal lending arena)

For small businesses, its payments and purchases, taxes and invoices could be used by lenders to make credit decisions effectively even if they’re unable to assess the business on-ground.

AA has the potential to phenomenally change banking. Every fintech segment will eventually be on account aggregators. Every business will have access to its entire financial life in one place.

But, there’s a difference between data and understanding.

Here’s a quick example - A works as a graphic designer who also wants to start selling cakes. With plenty of encouragement from her friends, she starts baking for friends’ birthdays/anniversaries. She makes enough to meet her expenses and keep some extra cash on the side. At this point, her business (modest) matches her credit needs (non-existent).

Now if she decides to quit her full-time job and pursue baking full-time, her first plan of action would be to buy an industrial oven and other equipment. At this point, her credit needs have jumped to meet her ambitions. This is also the point where most MSMEs get stuck. While ambitions seem perfectly normal to her, based on her experiences, a bank may not understand whether it's a well-suited risk or not.

Now imagine this in the context of the AA framework - as a lender, would GST, invoices etc be enough to assess her creditworthiness? Maybe as a lender, I should request data like social media activity, mobile bill repayment history, and even data from similar businesses in the area to better understand the borrower and her business in the context of the industry/area she operates in?

Here’s the bottom line - Nobody likes debt; human beings borrow for a purpose. If a business wants credit, it’ll be willing to provide any information that’s needed. And that takes care of the consent part of it, cold as it may sound.

But here’s where fintech, the messengers of this data, need to educate their customers. And here’s also where a scaffolding of innovation can come in - there could be voice-based consent that could be localized to suit the customer’s native language, for instance.

Think about it, there was so much fintech innovation around e-KYC, e-signing, and UPI. There are talks of getting telecom and even health data into the AA framework, and the holistic profiling with several permutations and combinations is endless (cliched as it sounds).

Nandan Nilekani believes that data on the account aggregator framework can be used to get a better deal on credit, health care, and even jobs.

With every incremental user/Account Aggregator, there can be a step-up in innovation for better accessibility.

And that’s the idea, right? To solve for accessibility. Maybe restaurant aggregator platforms like Swiggy/Zomato could start lending to restaurants on their platforms (check out Toast).

Really then, fintech innovation is radical. All the criticism? Par for the course.

See you next week!

Cheers,

Rajat