Lies and loyalty

What can lenders learn from NPS’ fall from grace

Ever wondered why people are more afraid of flying than driving, even though the probability of dying in a car crash is much higher than dying on a plane?

Or why do most of us still struggle to eat healthy and exercise regularly and spend money recklessly from time to time?

It’s certainly not a lack of information in both cases, right? Or a lack of intent in the second one?

It’s heuristics - the mental shortcuts that come hardwired in our brains to make decisions. An automated behavior trait, if I may. We’ll come back to this.

When I think about shifts in consumer behavior, I think about consumerism. The cheap and cheerful mentality that China introduced in the 1980s by mass manufacturing items at a lower cost and perhaps a lower quality.

I also think about big brands that once were. Brands that fell victim to behavior changes by not shifting their business models in time to keep up with changing trends. Take Blackberry, for instance - at one point there were nearly 80 million Blackberry users in the world, including former U.S. President Barack Obama (who ditched his Blackberry only in 2016).

Blackberry Messenger, or BBM, was all the rage. Almost like you weren’t cool enough if you weren’t on BBM. So, what was Blackberry’s demise? The iPhone. Blackberry ignored the touch screen based technology and the iPhone was already miles ahead. Its failure to innovate and adapt to changing consumer needs meant a market share of just 0.2% in 2016.

Adapting to change is about being in tune with consumer behavior. And we’re in the business of optimizing for the best behavioral outcome.

So, what is the best behavioral outcome for companies? Loyalty. And how can they optimize for it? More importantly, how do they measure it?

Enter NPS..

Back in 2003, the business world caught fire when Bain & Co’s partner and marketing consultant Fred Reichheld published an article in Harvard Business Review titled ‘The one number you need to grow’ and introduced the Net Promoter Score (NPS). He wrote that managers can gauge the ‘pulse’ of their customers with a ubiquitous one-question survey that now seems to trail just about every customer interaction — “How likely are you to recommend this brand to your friends and family?”

Reichheld’s conclusion was rather grand - “This number is the one number you need to grow. It’s that simple and that profound.”

It soon became the go-to number to measure customer loyalty.

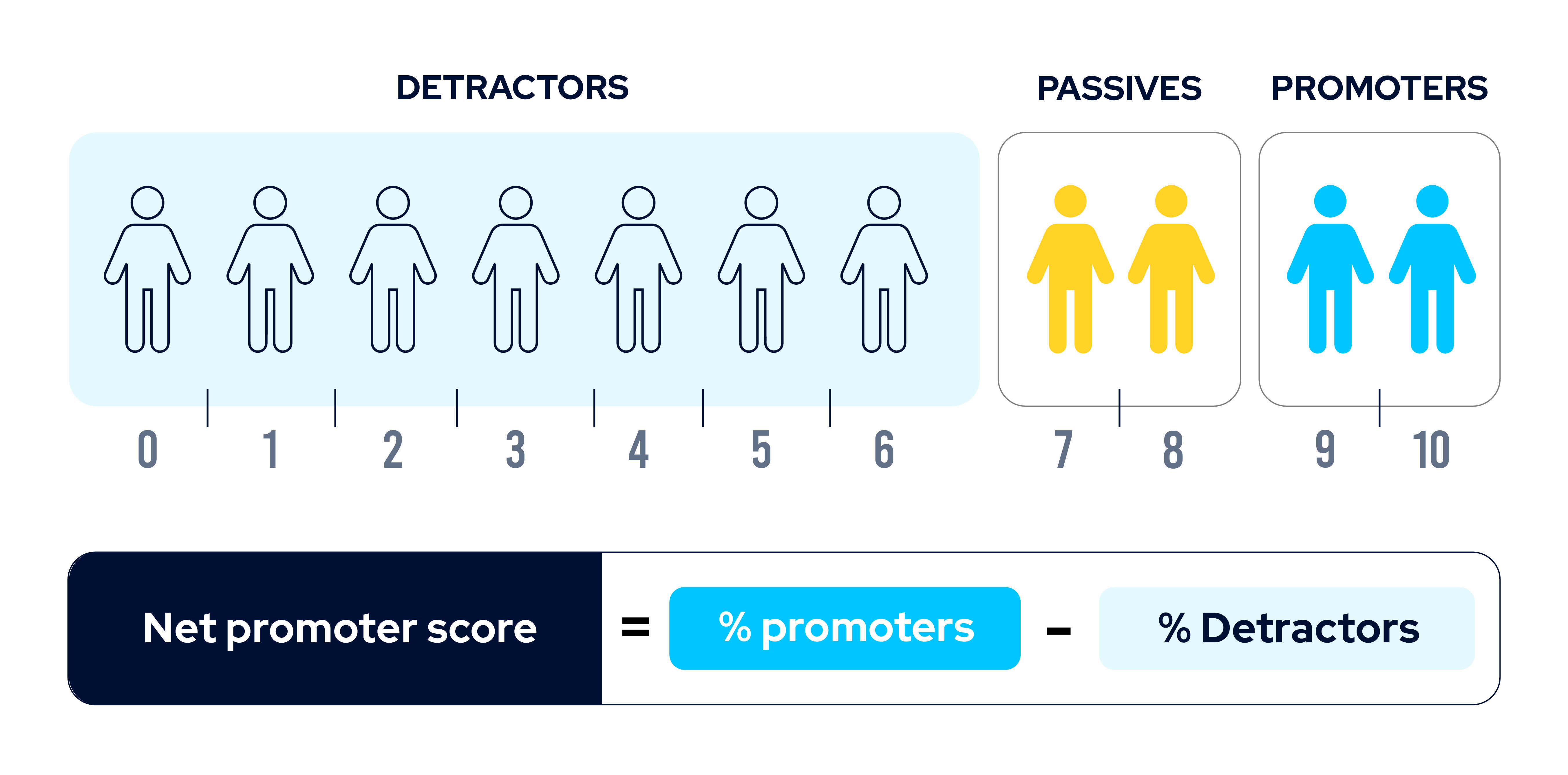

How does NPS work? Customers rate the likelihood of recommending a company/brand on a scale of 1-10. They’re then sorted into three categories -

As you can see, NPS fully ignores the passives. It disregards important differences in the score distribution, and no distinction is made between a 0 score and a 6 score. There is obviously a substantial discrepancy between those two.

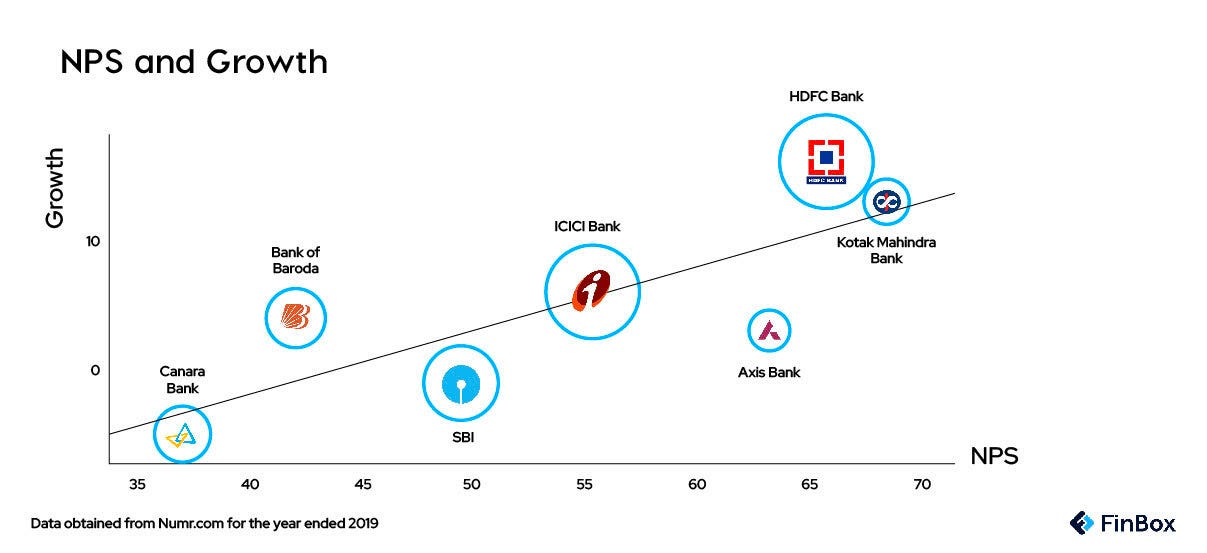

It’s a simple metric to get a quick read on consumer sentiment and also largely touted as a metric to measure business growth. According to the Wall Street Journal, in 2018, the NPS was cited more than 150 times in earnings conference calls by 50 S&P 500 companies. Surely, there must be some merit to it then? (even though WSJ called it a dubious management fad). Since I’m in the business of lending, I did some research on the top Indian banks and their NPS- to-growth rate relationship and here’s a little something -

Kotak Mahindra and HDFC had the highest NPS measuring 68 and 67 respectively. And both their compounded growth rate for the year ended 2019 was 13% and 16% respectively. Certainly then, the growth rate is mirroring the NPS.

Sure, NPS acts as a single number that companies across a particular industry can measure to scan the room for competitors.

But there’s a flipside to this argument. Its fallacy lies in its premise and its own success. Allow me to explain.

The premise of NPS is based on the homogeneity of its customers. For instance, if younger customers recommend products/services more than older customers do, then what does an improvement in the NPS mean? Does it mean your products/services have improved or that there’s been a demographic shift in your customer base?

Many organizations link executive bonuses to the NPS score and because it’s become such a widely used metric, it's often misused. Self-reported scores and misinterpretations of the NPS framework have sown confusion and diminished its credibility.

Also, there’s the feedback fatigue we all feel. Unless companies look at their consumer journey analytics, it’s hard to find at what point in the journey their customer is most engaged. Sending out the NPS survey at that moment, or at the ‘moment of truth’, might yield different results.

What if customers interpret the ‘likelihood to recommend’ question as a proxy for their satisfaction level? Or what if it’s just not in their nature to recommend?

And, the central argument against the NPS being the primary and only metric to define customer loyalty - Intent Vs Behavior.

Consider this 2007 survey of 16,000 people that showed only half of the respondents that had an intention to recommend a firm actually did.

Despite Kotak Mahindra Bank being the one with the highest NPS in 2019, Forbes’ World’s Best Banks survey for the same year found that HDFC, ICIC and DBS bank figured in the top three. Forbes’ customer survey is based on five key metrics, other than recommendation and satisfaction - trusts, terms & conditions, customer services, digital services and financial advice.

So, even with Kotak Mahindra Bank’s high NPS, it still wasn’t the most preferred bank among consumers (at least according to certain surveys). That means, despite NPS’ popularity, it doesn’t necessarily predict behavior.

So, how do we measure loyalty then?

Personally, I don’t have a problem with the NPS. If anything, its ease of use, surveying, calculation, benchmarking and its immediate peak into the emotional state of the consumer is great.

But, it can’t be a vanity statistic.

Here’s a question - would you recommend a crypto trading platform to your friend who’s really invested in the space AND to your 15 year old niece? Definitely to your friend but not to your niece right?

NPS does not capture this duality. And understanding the nuances behind recommending and not, is vital for any company looking to grow.

In late 2021, Reiccheld suggested a complementary system to the NPS and termed it earned growth. This requires companies to capture the reason each customer joined (whether they were referred, earned organically or bought with paid ads) and the net revenue retention.

Sounds like a more holistic approach, right? It still runs on the principles of homogeneity, doesn’t consider the feedback fatigue and more importantly, complex human behavior.

Let’s talk about lending for a minute..

Lenders are dime a dozen and customers aren’t borrowing for fun. That is a double-edged sword for loyalty and probably one of the hardest problems to crack for lenders.

Let’s get one thing out of the way - nobody WANTS to default on loans. Human beings are naturally hesitant and are influenced by uncertainty, perceived risk or the idea of indebtedness. They’re also concerned about the borrowing process itself, often assuming it to be more tedious and complex than it actually is, increasing distrust and dropping off.

Thus, the gaping hole in the financial services industry that deals with a plentitude of data, especially in a post-covid digital world, is palpable.

So how do lenders optimize for loyalty when there’s little to no trust?

Remember the example in the beginning about how we’re more scared of flying than driving? It’s a classic case of availability heuristics. Since news and media around air crashes are higher, we recall that information easily and make an unconscious decision about how dangerous it is.

We’re all emotional about money and naturally prey to the availability bias - the one time you had credit card debt and you recall how stressed you were, or all the news about banking systems collapsing and all your savings tanking.

What’s a fix for the availability bias? Hyper-personalization. Tracking the financial footprint of the consumer and creating communication and products can increase digital conversions of potential borrowers by 36% by applying behavioral economics, according to EY.

One of the biggest fallacies of the NPS is assuming homogeneity of its customers. One report found that consumers buying gold loans in North India prefer flexibility and do not like to be bound by procedure. So giving them the power to structure the loan builds trust and increases loyalty.

And these are the consumer behavior patterns that really need to be looked at for hyper-personalisation and eventually, loyalty.

That’s not news for fintechs sitting on petabytes of consumer information that can potentially turn the financial world on its head.

Look at what Embedded Finance is doing - it’s allowing platform companies to nurture deeper relationships with their customers. It’s giving them credit at the point of sale, tailor-making flexible credit options, enabling platforms to cross-sell/upsell personalized products.

Embedded finance is built on the conjecture that predicting human behavior trumps building core technology.

Think about all the fintech innovations that exist thanks to the industry’s AI/ML capabilities that predict behavior. Everything from personalized and adaptive finance, encrypted cryptocurrency trading, customer identity verification and fraud prevention to inclusive finance, smart audit, and handshake loan brokerage.

To tie it all up together…

Look at the adoption of Buy-Now-Pay-Later (BNPL). In mature markets like Australia, 50% of BNPL customers have stopped using credit cards. Even in nascent markets like India, BNPL emerged as the preferred option for people across age groups with the youngest customer being 18 years old and the oldest at 66. This trend is glaringly visible among Gen-Z and Millennials.

Fintechs adapted to the younger generation’s need for ease - this cohort grew up with the internet and have probably never visited a bank branch. So fintechs optimized for this behavior and created the mammoth that is now BNPL.

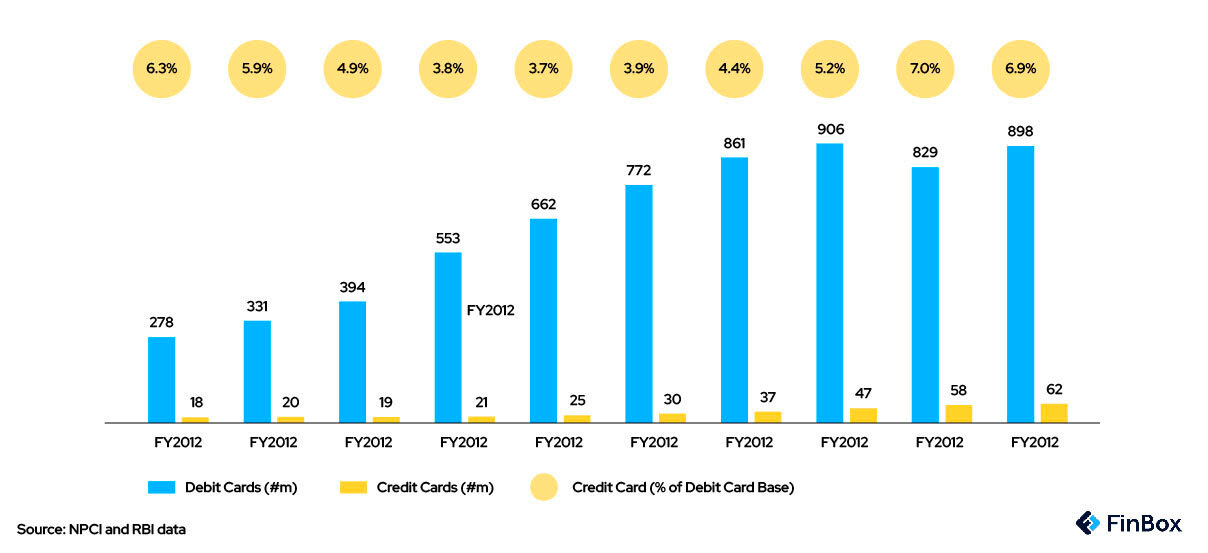

Remember Blackberry? Well, traditional financial institutions that have not adapted to BNPL saw a rather flat growth in the number of credit cards added in the last decade. So, safe to say that BNPL adoption is likely to precede the demise of credit cards?

I’m in the business of optimizing for the best behavioral outcome. I know that the information that eating healthy and exercising everyday, or gauging the intent to do so won’t actually make me want to do those. And that’s really the problem with gauging intent alone - we’re hardwired to be optimistic.

When NPS was first introduced, some companies struggled to grasp the concept, some struggled to align it with existing data, some had adopted the likelihood to purchase additional products as more closely tied to growth. But for everyone, the NPS was the elusive unicorn.

Now, however, the access to more layers of data as well as qualitative enrichment of consumer behavior analytics can tell us previously untold secrets. It’s not just what we hear from the consumers but what we see when no one’s watching. These insights have helped us build not only better risk models but also newer products and features that optimize for consumer experience as opposed to just empty-boosting the NPS.

In fact, when it comes to lending and allied activities, Goodhart’s law comes to mind and offers a rather illuminating perspective. To me the law suggests that we should focus on improving not what’s readily available but what’s important. Put simply, the law states:

"When a measure becomes a target, it ceases to be a good measure."

There’s not an easy, harmonized solution to understanding any human behavior. We’re all complex and contradictory beings. We’re simultaneously operating on multiple planes - placing facts, emotions, experiences within context and making decisions. There’s no oversimplified model that can predict the natural human state.

Guess we just have to stay hungry, stay foolish and keep digging – one petabyte of data at a time!

PS: Watch this space tomorrow for our weekly FinTech wrap to hit your inboxes. Have a safe and happy holi!