Know Your Regulations before you Know Your Customers

Know Your Regulations before you Know Your Customers

A few weeks ago, I predicted in this newsletter that the RBI was on the path to overhaul its digital lending regulations one piece at a time. I was obviously referring to its clarification vis-a-vis PPI norms that led to companies transforming their business models almost overnight.

As if on cue, the regulator is on to the next piece.

The Morning Context reported this week that the RBI is now coming after fintechs’ KYC check processes. The central bank is set to release guidelines that might set some guardrails around the KYC processes for digital credit products across the spectrum. . It may also ask fintechs to draw a distinction between customer onboarding and underwriting, among other things.

The regulator seems to be going over its regulations and policy the digital lending industry with a fine-toothed comb — closing any loopholes that may be exploited in the name of innovation.

Interpreting KYC guidelines

If one closely observes various products and journeys across apps, one will find that in digital lending, KYC processes are often designed to suit budgets and user experiences of fintechs. In the eyes of the regulator, this amounts to giving business imperatives precedence over regulatory imperatives.

The existing RBI guidelines on KYC include Aadhaar verification, digital KYC which includes capturing a live photo and coordinates of the customer, a digital signature, or video-based customer identification.

While these form part of the KYC requirements for most digital lenders, the guidelines have been interpreted differently by all companies. In many cases, fintechs have found themselves in hot water over violating, or not sufficiently adhering to these rules.

For instance, Ola Financial Services was fined Rs 1.67 crore for violating KYC norms. Paytm Payments Bank was barred from onboarding more customers in March for the same reasons. There must be many more incidents that the public record doesn't yet reflect but it’s clear that the regulator won’t let these adventures go unnoticed.

I’m all about fintech innovation, but the regulator’s concerns stemming from widespread disbursal of loans without proper know-your-customer checks seem justified. A prolonged, unchecked practice of conducting inadequate KYC checks could result in a mounting bad debt problem and could violate the provisions of anti-money laundering laws.

It’s the same story as the PPI crackdown – the regulatory gray area that gives freedom also makes the system vulnerable. After all, there is a difference between inventiveness and an outright bending of the rules.

By the rules - the best business strategy

Many fintechs affected by the PPI clarification are once burned twice shy. Already, the likes of Slice and Uni Card are onboarding only those customers who have completed full KYC checks. This is a good step in being proactive and escaping corrective action at the hands of the regulators.

But it brings me back to a point I made earlier – KYC norms are often taken lightly, or being completely bungled, because it serves the business interests of fintechs. Yes, lowering the KYC drawbridge accelerates customer acquisition by reducing drop-offs and makes the whole process cheaper. But how sustainable is it?

I’ll attempt to address the two major reasons why digital lenders could be driven to play fast and loose with KYC rules – user experience and costs.

The UX problem

While onboarding, the average customer does not know the difference between KYC and underwriting. That’s a deliberate step taken by fintechs to smooth over the user experience. Customers are asked for a mix of information that could serve risk assessment, KYC or both.

In fact, these are two very different things. KYC is a mandatory part of financial services onboarding which requires the business to get the customers to provide their verified details. This is done for both regulatory and anti-money laundering reasons.

Meanwhile, underwriting is the process of taking a credit decision by analyzing additional information shared by a consumer about their financial wellbeing - this could mean bureau scores in traditional lending or new-age alternate data-driven scores such as the FinBox Inclusion Score.

As the new guidelines look to make this distinction more coherent, digital lenders will be left with a high drop-off problem on their hands, right?

Not necessarily.

In 2016, the Wells Fargo banking app introduced a safety feature to replace passwords. It allowed customers to unlock the app with an eye scan and conduct transactions worth millions of dollars. The only problem was that the feature worked so quickly, worrying customers that it couldn’t scan properly. An artificial wait time was added to create some positive friction to elicit trust.

Similarly, separating KYC requirements from underwriting at the time of onboarding allows lenders to seek pertinent information at various points. Such positive friction could establish credibility with the customer and ultimately contribute to a positive customer experience.

This will require a lot of work in terms of rethinking the journeys and finding ways to keep the consumer engaged but it’s hard work that must be done to avoid long-term pain. Be it dynamic journeys, positive friction or graded assessments, it’s time for FinTechs to once again balance consumer experience with the regulatory imperatives.

The cost dilemma

Costs of physical KYC, especially those conducted for small-ticket loans, have been the bane of lenders, both traditional and digital. The existing RBI guidelines already allow for various ways in which the process can be carried out digitally. In the race to onboard customers quickly and cheaply, these have been flouted time and again.

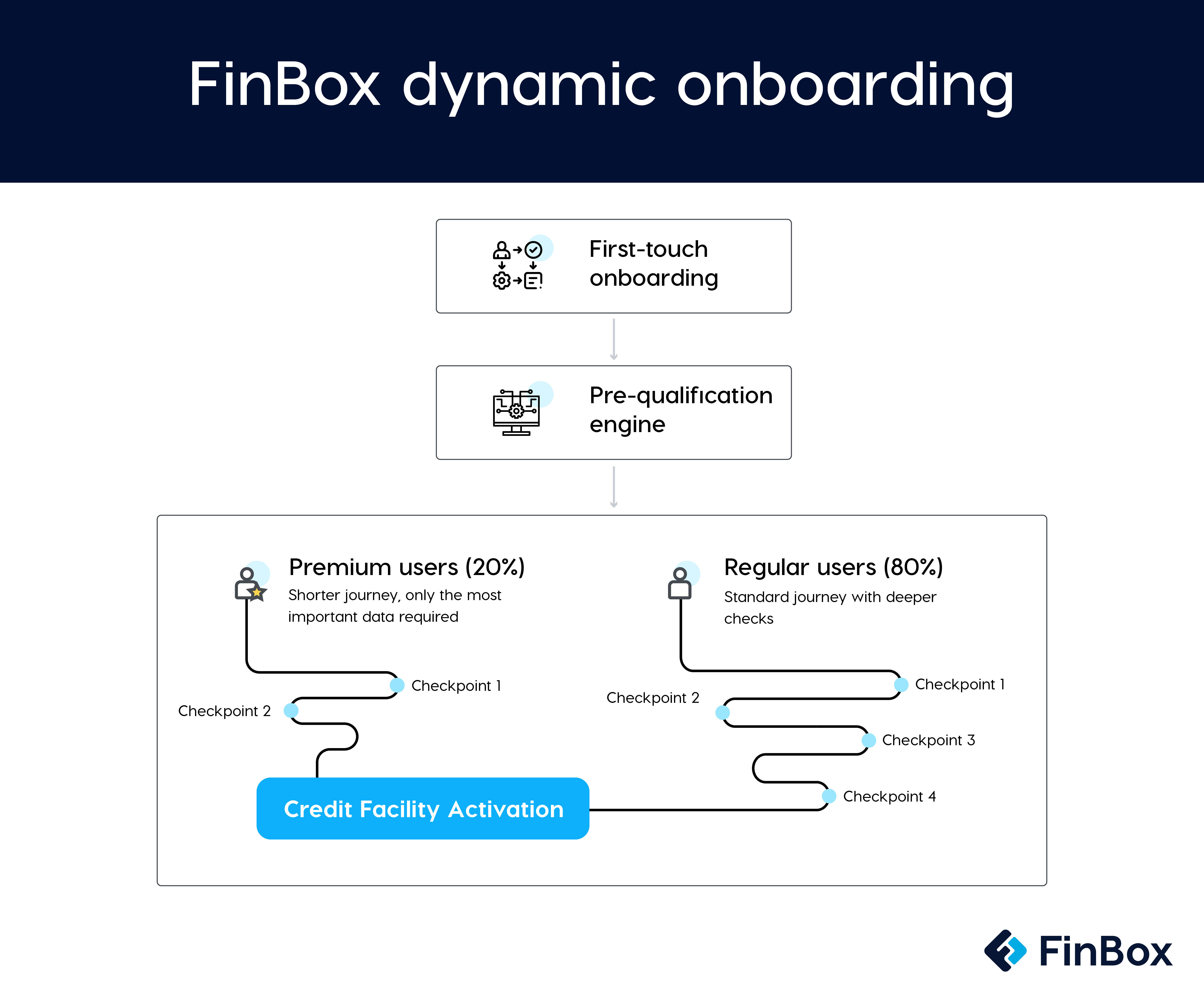

So how can lenders rein in these costs while adhering to the norms? Allocate budgets smartly with dynamic KYC.

Design KYC processes for various segments of loan applications based on their ticket size. Moreover, a prequalification engine can help judge a preliminary risk profile of each customer. Now, applicants in each funnel can be put through customized onboarding.

For instance, those seeking small loans with a relatively safer risk profile need not require physical verification. Meanwhile, larger budgets can be earmarked for physically verifying riskier and high amount loan seekers.

The RBI’s guidelines on KYC are more comprehensive than its rules on underwriting. So, lenders can invest in cost-effective underwriting stacks complete with AI/ML capabilities. This would free up resources that can be diverted towards more comprehensive KYC checks.

The bottomline

Over the last few years, misconduct on part of digital lenders has given sufficient fodder to headlines. The trickling regulatory interventions at this juncture are not only justified, but warranted. But there is no knowing how restrictive the incoming guidelines will be and whether they will leave room for ingenuity.

“The best and safest thing is to keep a balance in your life, acknowledge the great powers around us and in us. If you can do that, and live that way, you are really a wise man.” - Euripides

That’s the key – finding balance, while acknowledging the greater powers.

As fintech finds itself being limited by more and more regulatory scrutiny, there is wisdom in adapting to change and finding ways to work honestly and honorably. Fintech needs to show it can engender trust the same way banks do, while also remaining agile and accessible.

After all, isn’t that where we excel?

See you next week.

Cheers,

Rajat