How many crises before banks tread with caution?

On trust, bad habits, and good times

Hi,

The etymology of the word ‘credit’ stems from the Middle French term for belief or trust.

Grand banking halls were the earliest signals of trust - letting customers know that the bank would still be there in the morning and that their money is safe.

Financial services is all about trust. And finding new ways to contrive it. The pawnbroking industry that sprang up in Buddhist monasteries of China was also a signal of trust - it leveraged the trust available with religion. Clearinghouses - trust in a single centralised entity rather than any counterparty; Credit scores - trust in a consumer’s ability to repay a loan; Deposit insurance - eliminates the need for depositors to undertake due diligence on the financial condition of their bank.

However, trust is also fragile and easy to dissipate.

From the dotcom bubble in 2000 through to the 2008 Lehman debacle and this decade’s eurozone sovereign debt crisis,and more recently, the Silicon Valley Bank run - all instances of a cumulative breakdown of trust that took decades to establish.

Only last week, the Reserve Bank of India Governor Shaktikanta Das raised some red flags - that I’ll get to a little later- but here’s what he had to say about trust -

“The importance of public trust in the banking system, as exemplified in the recent bank failures in the United States, also needs to be appreciated. This was a classic case wherein public trust in certain banks evaporated suddenly.

Further, in this digital age, it took only a few hours to transfer billions of dollars held as deposits in a bank to other institutions, leading to a severe liquidity crisis. The monitoring of information appearing in various media, including social media, has therefore become very important for any bank.

In this kind of milieu, it is upon the banks and their boards to assiduously build a sound corporate culture and value system within the organisation.”

If the crises have taught us anything, it’s that trust, once lost, is difficult to restore. And we must never take it for granted. Especially at a time when things are looking up.

How do banks build trust?

Trust was a promise standing on a three-legged stool - a) banks will be solvent and keep deposits safe; b) banks will be around for a long time; c) banks care about customers’ money and take their interests (pun intended) very seriously.

In fact, ‘legacy banks’ that I keep talking about all have the same approach to trust - avoid failure at all costs, avoid lending to risky client sectors, and often the optimal trust move is to change nothing.

And nothing wrong with that kind of stability, especially for older generations and big corporations that can’t bounce back from setbacks very easily. But it also means stunted growth for banks and financial exclusion - more specifically, slow-to-no innovation, and the exclusion of segments who may seem risky on paper, but could prove to be exemplary borrowers if only given the opportunity.

What we need now is a fresh approach to trust - one that places customer well-being and convenience at the forefront. Or, in the words of Anthony Lipp, IBM Global Head of Strategy for Banking and Financial Markets, “unregulated trust” that goes beyond what’s required by regulators.

Here’s what I think that involves:

Embracing a Data-Driven Approach to De-Risking: Rather than relying on broad categorisations of high-risk sectors, incumbents should focus on empowering risk teams to become adept data scientists. By consistently pushing the boundaries of data science and challenging traditional practices, institutions can better mitigate risks without resorting to rigid labels. This shift requires a cultural and mindset change.

Finding the Right Place for Transparency: Loan applications have traditionally been laborious and time-consuming, disappearing into a black hole of ‘processing’ for weeks on end. This is just one example of how opaque the financial industry can be. Today, banks are offering digital platforms where customers can log in and track the progress of their applications, alongside a list of conditions and charges, if any.

Embracing Effective Storytelling: There's no downside to becoming a better storyteller. While leaders like Jamie Dimon may not start tweeting about every outage, they can follow the example set by annual letters that provide consistent narratives, addressing both the positive and negative aspects. Authenticity and professionalism can coexist, as demonstrated by Microsoft under Satya Nadella, who successfully broke historical taboos (like supporting Linux in Azure) while maintaining and growing their market share. Stepping away from outdated advertising and embracing a middle ground can yield positive results.

Good times, bad habits and how the RBI can trust banks

Addressing the Conference of Directors of Banks last week, RBI Governor Das cautioned banks from abandoning prudence, especially at a time when things are beginning to look up for the Indian economy as well as its financial sector -

“Today our banking sector stands out as strong and stable with CRAR (capital to risk-weighted asset ratio) at 16.1%, Gross NPA (non-performing assets) at 4.41%, Net NPA at 1.16% and Provision Coverage Ratio at 73.20% at the end of December 2022.It is in times such as these that complacency may set in. We have to bear in mind that risks often get overlooked or forgotten when things are going well.”’

It is evident that the Reserve Bank of India (RBI) has expressed concerns regarding the governance standards of commercial banks. There are plausible reasons behind this apprehension. It is possible that recent events, such as the distressing incident at Silicon Valley Bank in the United States, have caused unease within the RBI.

In the same speech, the RBI governor further raised concerns about evergreening loans, using internal or Office accounts to adjust borrower’s repayment obligations; renewal of loans or disbursement of new/additional loans to the stressed borrower or related entities closer to the repayment date of the earlier loans.

Why are the warnings when things are - by all indicators - looking up? Because it’s when things are going well, that we tend to become overconfident. It’s simply human nature.

During the prosperous growth period in the early 2000s, when the economy was growing at an average of 9% andinvestment levels were high, banks prioritised growth over caution. This led to companies taking on excessive debt. Corruption among politicians, bureaucrats, bankers, and corporates further worsened the situation by allowing loans to be granted to financially weak entities.

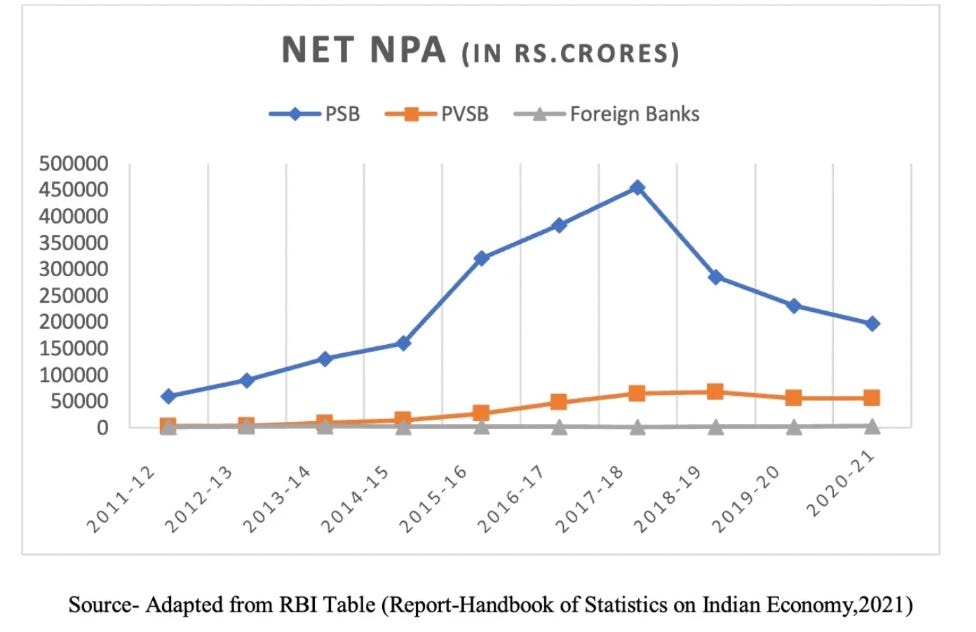

When the global financial crisis hit in 2008, even financially sound companies faced a decline in their business. As a result, many companies were unable to repay their debts to the banks. The total amount of non-performing assets (NPAs) reached a staggering 4.5 lakh crore, which is nearly five times the annual budget of the rural employment guarantee scheme.

The table shown, taken from a Parliament document, vividly illustrates the troubling tale of non-performing assets (NPAs) – a narrative marked by a series of mistakes and wrongdoing. It is evident that the fiscal missteps made during the years of economic growth have come back to haunt us.

The Reserve Bank of India (RBI) is determined to prevent a recurrence of such circumstances, at a time when bank lending has grown by 15% in FY23 and the country’s largest lenders including State Bank of India, HDFC Bank andBank of Baroda reported a record annual profit.

In good times like these, old habits die hard.

Sound advice by Das then, no?

.

What the banking community expects from the RBI

The banking community expects the RBI to figure out a framework to identify loans, the type of stressed loans which are used in the evergreening process.

A red-code system of sorts, in collaboration with Automated Clearing House (ACH), and other relevant enforcement agencies; one that involves assigning a unique code to large and frequent borrowers to monitor the disbursed funds from the source. This could potentially facilitate data analysis from a centralised database to verify the occurrence of evergreening.

From a macro perspective, research suggests that a 10 percentage point rise in the proportion of trustworthy individuals within a particular region can lead to an approximate 0.5 percentage point increase in annual GDP growth. Furthermore, trust's advantages extend beyond borders in our interconnected world. According to another study, a one standard deviation increase in trust is linked to a significant 90 to 150% alteration in bilateral trade. These findings demonstrate the far-reaching impact of trust in fostering economic prosperity.

But, there is a toxic loss of trust that vitiates financial services.

In order to rebuild confidence, some argue that central banks should undergo greater transparency and increased political oversight. However, this approach carries the risk of politicising these crucial institutions that require independence from politicians. Additionally, to prevent a repeat of the past, there is a call for a comprehensive reform of the prosecutorial system for white-collar crime. This reform could significantly enhance public trust, but caution must be exercised to avoid scapegoating or turning trials into mere spectacles.

Trust is complicated. One thing I’m certain of is that without trust in financial institutions themselves, or those who work in them, the next crisis could be far more deadly than the last.

That's all from me this week!

Cheers,

Rajat