GSTN on AA: Credit vs welfare?

Can credit and AA become the welfare state that India was supposed to be?

The financial world is thrilled by the news of GSTN’s imminent launch on the Account Aggregator (AA) platform. This is bound to give a fillip to MSME lending — the expectation is a Rs 25 lakh crore disbursement in the next three years. Now, that’s almost the total value of credit disbursed to MSMEs as of 2023. In other words, a doubling of MSME credit in the next three years, marking an audacious transformation that will give primacy to unsecured credit.

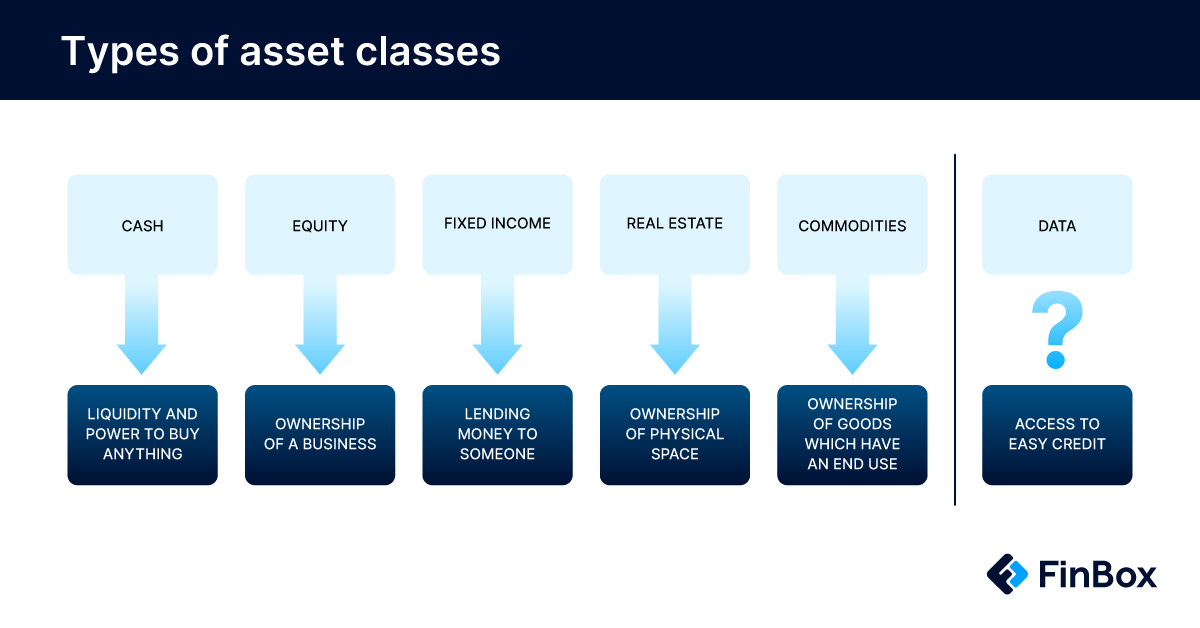

Data as an asset class

Throughout much of recorded human history, the dynamics between the haves and the have-nots have been a prominent theme and it will continue to be. For most parts, the struggle was between the landed gentry and the landless. Then it was between those who owned the means of production and those who didn’t. In the 21st century, however, data will eclipse both land and machinery as the most important asset, and it will be a struggle to control the flow of data. Hence, the most pertinent question of our century is, “Who owns the data or rather who should own the data?”.

If we want to prevent the concentration of wealth in the hands of a small elite, the key is to regulate the ownership of data. In this context, EU’s PSD2 regulations and India’s AA framework are baby steps towards addressing this fundamental question. The general narrative is that the customer owns the data, except we don’t know what it really means.

For instance, we know how to regulate ownership of land — it takes land titling and fencing. We know how to regulate ownership of industry, for we have perfected the art of shareholding. But we don’t have much experience regulating the ownership of data. However, it’s not hard to paint a picture of what it could look like.

Let’s go back to the news of GSTN going live as a Financial Information Provider (FIP) on AA for a bit. Discussions are ongoing about the integration of TReDS platform with GSTN e-invoicing portal to allow real time sharing of data through a single window of access to authenticated invoices (The Hindu Business Line). Such an integration will ensure that e-invoices raised by MSMEs on GSTN can come directly to the TReDS portal, thus negating the need for any additional activity or documentation.

What this means is that a small business will be able to obtain a loan against their invoices as soon as they raise it on GSTN, even if it has minimal to no credit history. In other words, a small business will now be able to use their own data to protect themselves from the vagaries of billing cycles, thereby, attaining financial stability.

Gradually the AA framework is bound to see more participation and will sooner than later regulate the flow of tax data, pensions data, securities data (mutual funds and brokerage), insurance data, and more. With such a diverse range of data at financiers’ disposal, unsecured lending opportunities are bound to flourish.

Imagine this: Pensioners who otherwise have very little chance of accessing credit can share their pension data and get personal loans. Unemployed can get bridge loans. Those hit by a calamity can get disaster relief loans. New families can avail adoption loans. Those awaiting disability benefits can tide themselves over with special needs’ loans. The possibilities are endless.

Well, an inclusive credit system therefore poses as a realistic means for people to realise their economic rights.

Can an AA-powered credit system fulfil the role of a welfare state?

This is one of the most pressing questions before contemporary political economists. And according to some, when real incomes failed to keep pace with productivity and cost of living, credit filled the void. Corporate America provided credit to households in lieu of raising wages and as a reward for disciplined individual behaviour (Watkins, 2017 and Langley, 2008).

How it will play out within the Indian economy remains to be seen. As I see it, an inclusive credit system can at best be considered indirect welfare. This is a subject that merits thorough investigation, something I hope to do in the coming weeks.

What does a credit-driven welfare system mean for the Indian economy? How much credit is too much credit? I’d love to know your thoughts.