‘Going digital’ is not cheaper; save money, find yourself a fintech

‘Going digital’ is not cheaper; save money, find yourself a fintech

I made a joke the other day. The joke was that we had not ordered anything online yesterday, and our usual delivery guy should have called to check if we were OK.

As bad a joke as it may be, it made me realize that we really have pivoted from a world of stores and streets to a world that is decentralized, digital and delivering to our homes.

The same themes of decentralization and democratization apply to banking just as much as it does to retail and the world. During the 2020s lockdown, we moved to work-from-home, order-from-home, entertain-at-home, bank-from-home.

The thing is, this really is the reconstruction of our society from physical to digital in real-time and turbo-charged

We see the statistics almost everyday.

At 48 billion, India accounted for the largest number of worldwide real-time transactions in 2021

India is set to experience the biggest boom in digital banking adoption in the next five years - 21% increase in adults with an online-only bank account. Essentially, a little under 400 million adults will have a neobank account

An estimated 205 million Indian adults already have a digital-only bank account.

A report predicts that Indian banks are projected to spend over $1billion by 2025 on public cloud initiatives.

What does this mean? It means society is truly digital - not just a small step, not just an incremental change, but a true revolution of society.

What does this mean for banks? Uber digitisation ideally means disruptive innovation and new technologies, forcing banks to invest heavily to upgrade their IT infrastructure, leading to higher operating expenses.

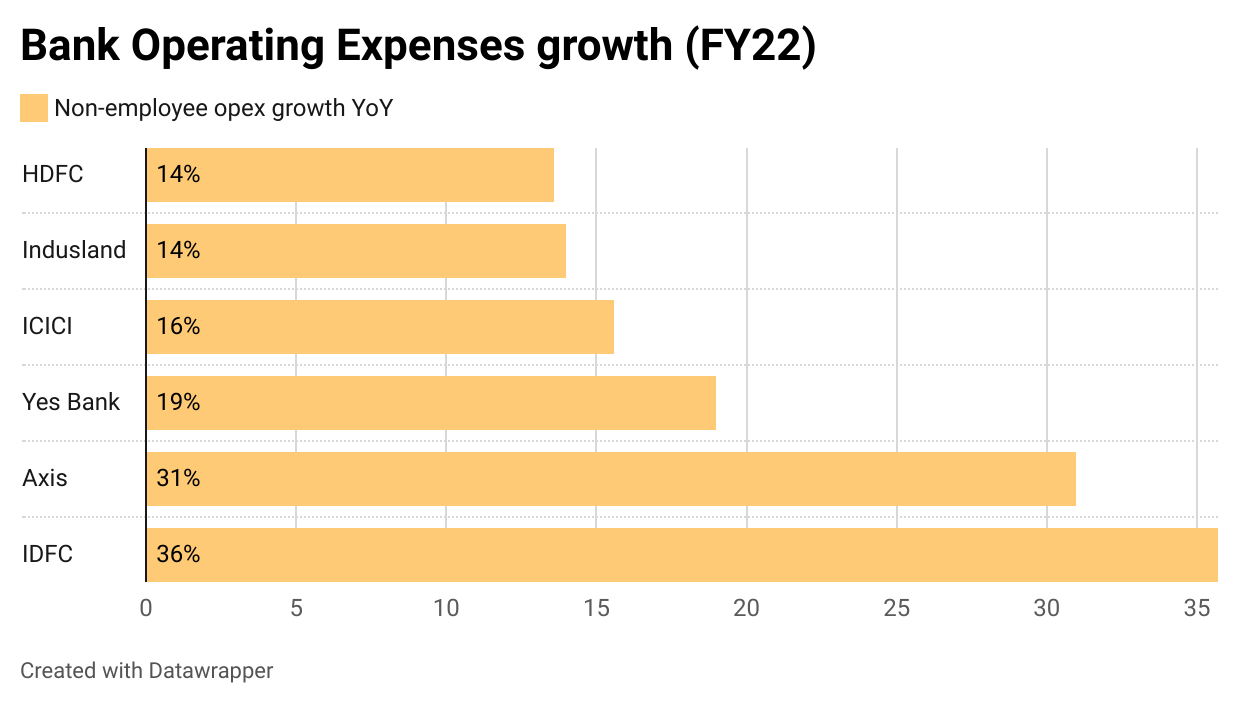

Operating expenses for the banks have grown steadily over the last year.

India’s second largest private lender ICICI Bank saw a 16% year-on-year (YoY) increase in its non-employee expenses to Rs 17,060.57 crore for FY22. This increase was on the back of expenses in its retail business and technology-related expenses. ICICI has said that nearly 8.5% of the bank's total operating expenses were spent on technology-related expenses - that comes to about Rs 2300 crores.

Axis Bank, one of the bigger private sector lenders, saw 31% YoY growth in non-employee expenses for FY22 and claims to have spent nearly 8% of the total expenses on technology - that’s a little more than Rs 1800 crores. That’s a 40% increase YoY on tech-spend for Axis

The need to modernize to remain competitive and relevant is real.

The spur in tech-spend comes on the back of a need to compete with big conglomerates like the Tatas, Reliance and Adani, all of whom are building super apps that might take away the customer further away from the bank branches.

Read: TATA launches its super app: what does it mean for banks, businesses,

And if, or rather when, these super apps double down on their FinTech play, they will emerge as another threat to banks.

Indeed, in understanding how fintechs pose a fundamental challenge to banks, we could also understand the digitisation of banking in itself.

I think every financial product imaginable will have a structure like this. What did fintechs do? They stole the stack.

So now, the new financial stack looks like this -

There are two key reasons that Fintech has come to dominate the financial stack:

Better distribution - Conversions are complicated and expensive. 97% of online banking journeys that are started are abandoned - effectively leaving the conversion rate at less than 3%. Considering that 52% of customers prefer using digital banking options, the 3% conversion rate can be daunting.

I came across this rather insightful whitepaper by ARK Investments which estimates a $20 Customer Acquisition Cost (CAC) for digital wallets as opposed to a $1500 CAC for opening a checking account with a bank.

Intuitively, it makes sense. Wallets, for instance, have grown at a furious pace due to the inherent network effects and the virality of managing P2P payments. The acquisition of one customer means the acquisition of the second, third, fourth and fifth. Fintechs have made financial products viral. How? By removing friction from account opening processes such as enabling photos of ID to be used for account verification or using additional accounts. Try that with most banks - it is difficult if not impossible.

Better analytics - Analytics needs data and the correct data is not that easy to collect. The data you need is lending data, not just demographics or social media data. How do you garner lending data? You need to make some assumptions and give loans to test those assumptions and then refine those assumptions. Fintech companies are more innovative and happy to make calculated bets on improving the experience 10x rather than making incremental improvements. For regulated banks, risking customer deposits in such fashion can be difficult to explain to regulators and customers later.

And beyond that..product development has followed fintech and overall technology stack (not just distribution, the entire operating system).

Technology is extremely important; it is the shift towards open banking, open data, Banking-as-a-service provided by fintechs the world over that has facilitated the investor and customer rush towards fintech.

And ushered in an era of embedded finance. Almost every financial product can be built outside the traditional ecosystem, so why should banks spend crores of rupees building tech rails when they can just rent it?

“Banks should be “scared s***less” of fintechs,” said JP Morgan Chase CEO Jamie Dimon, in the company’s January 2021 quarterly call to analysts.

When I talk about renting the tech rails, I mean partnering with fintechs. And Dimon wasn’t wrong, harsh as it may be - fintechs and other new entrants in the financial services arena are redefining the industry.

In fact, a 2021 KPMG report said “over the last year, many have seen that it’s quicker to do so by partnering with, investing in, or acquiring fintechs, particularly with respect to high demand skills.”

The benefits of fintech for banks go beyond increasing revenue through - building brand reputation, offering new products/features, Increased ease-of-use, broadened consumer base, reduced costs, scale faster.

Source: EY

Banks used to compete largely based on price, product, scale of the branch network. But today? Today customer experience is the final frontier. Traditional banks can invest billions of dollars into upgrading their IT infrastructure, but who’s going to teach them how to act and think like fintech? Who’s going to guide them through understanding and emulating how fintechs approach customers?

As you saw in my financial stack doodle, banks are still very much part of it. They’re trusted (maybe some more than others), they will continue to attract deposits (aka cheap funding), they’ve painstakingly built themselves up around rigid regulation. And that’s great; except that these pipes and rails need to be put to good use and that means being in the financial services business, rather than in the savings account and credit card business. The digitization puzzle is complex but it doesn’t have to be complicated.

This is how financial services will develop - in micro doses by micro specialists. Banks will be specialists in some activities but FinBox, for instance, is a pioneering specialist at infrastructure architecture that can help enterprises and lenders launch, distribute and scale credit products on-the-go.

And concluding…

Fintech has made magnificent strides at capturing audiences where banks failed. This has been propelled by

Lower CAC

The ability to reinvent data driven products

Banks are spending ‘bigly’ on tech. The smart ones? They’re realising that they can co-operate with fintechs by utilising their regulated status to allow for innovation in product and Customer Experience on top of their existing infrastructure.

A world in which teenagers who can code is the new world of finance. The banking model is completely turned on its head.

There is a big difference between being a digital immigrant and a digital native; between being built-on-the-cloud, born-on-the-internet and evolved to become cloud-based and available-on-the-internet. If you want to build a bank truly fit for the next few decades, look around - plenty of fintechs in the sea.

Read: Banking-as-a-service: Risks and complexities to consider before choosing the right partner