Gen Z and Millennials: Driving Consumer Credit and Reshaping the India Story?

When does cosnumer credit become excessive?

The ‘India story’ has taken global centrestage. In the last 24 hours, there’s been much jubilation over Jefferies’ Chris Wood calling India’s stock market rally the best in the world, and how it’s nowhere near ending.

However, to my mind, the true essence of the ‘India story’ will be shaped by allocation of credit over the next five years. The equity market's exuberance is merely a mirror of the underlying economic narrative, not the driving force.

The sustainability of India's growth and the longevity of its market success hinge on prudent credit distribution that fuels productive investments, bolsters businesses, and meets consumer needs. How effectively India navigates this critical aspect will determine whether the current euphoria translates into enduring economic strength.

The Indian credit landscape has been undergoing some major changes over the last few years. If these persist, they could dramatically alter credit allocation in the economy, which in turn will have repercussions for economic growth as well as for the distribution of the country’s output.

Credit is shifting hands: From industry to consumers

In the last 14 years, Indian banking underwent a silent but significant transformation. From providing credit predominantly to industry and businesses, the sector became a provider of credit mainly to consumers.

The share of industry in total banking credit dropped from 43% in 2010 to 23.1% by 2024, while consumer loans increased from 19% in 2010 to 31% in 2024. Banks also provide credit indirectly to businesses and consumers through NBFCs. The share of NBFCs in total banking credit grew from 3.7% in 2010 to 9.4% in 2024. Although it is hard to precisely estimate the shares of NBFC credit that went to businesses and consumers, the general sense is a 60-40 divide between businesses and consumers, respectively. (Source: Multiple news articles)

This leads to several pertinent questions. One, what explains this change in composition of the Indian credit portfolio. Two, where is consumer credit headed and is it a structural or cyclical phenomenon? Three, is there a need for strategic shift in credit allocation to sustain the ‘India story’?

What's driving consumer credit?

Both demand- and supply-side factors contribute to the rapid growth of consumer credit.

Demand-side factors:

On the demand side, the main factors are economic and demographic. There’s been a consistent increase in India’s per capita income and per capita income thresholds have proven to be key inflection points in the growth of consumer credit across economies. India appears to have followed this global trend.

Adding to the economic driver is a significant demographic shift: Millennials and Gen Z, who are more inclined to borrow for consumption.

Supply-side factors:

The rise of fintech players and the accompanied digital lending boom are key drivers of consumer credit.

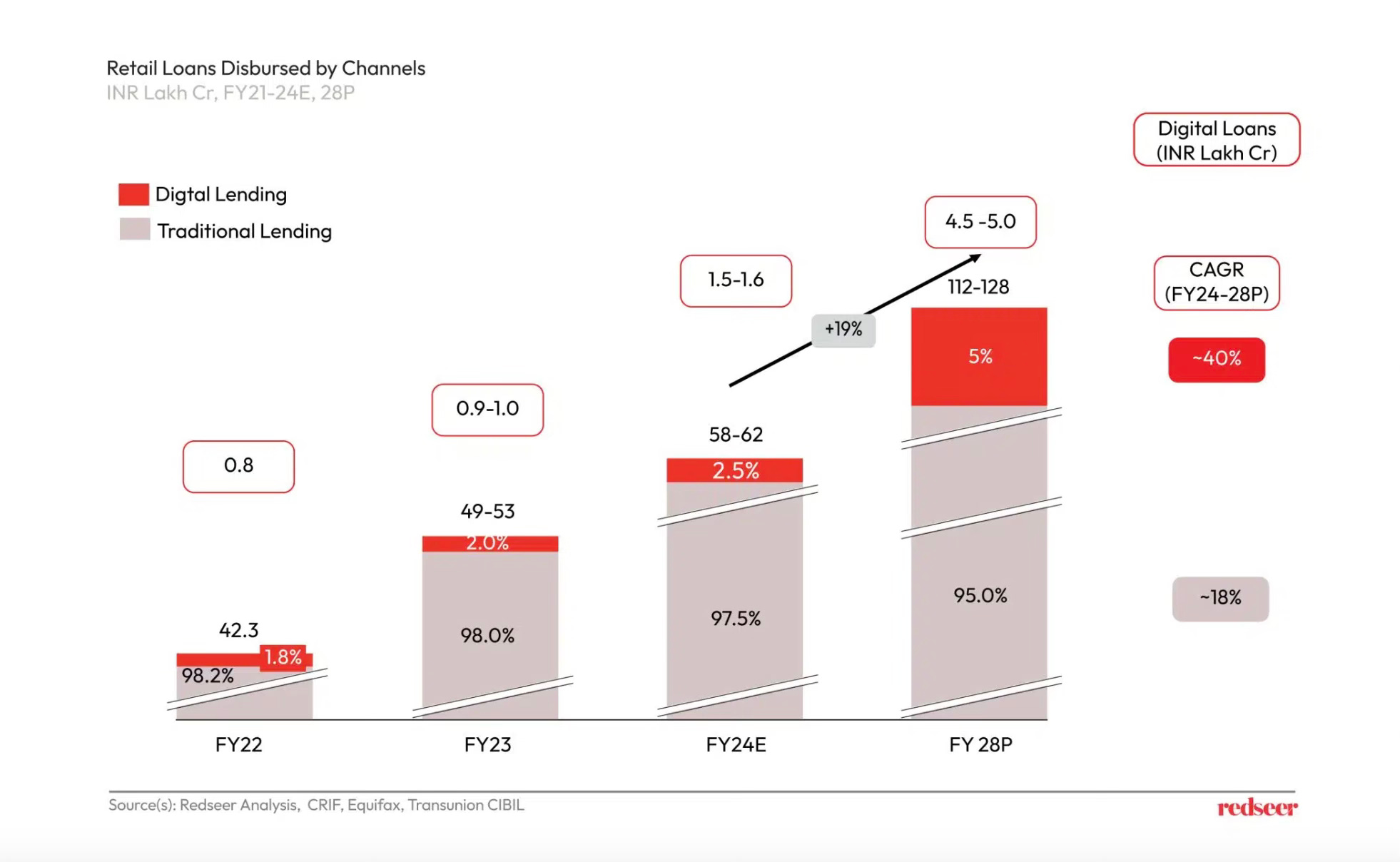

If you look at the entire retail loan market, Gen Z contributes INR 3.5-4 lakh crore to retail loan disbursals, millennials account for INR 25-28 lakh crore, and the remaining disbursals total INR 28-30 lakh crore.

The data from FY 22 to FY 24 highlights a significant growth in digital lending, which has increased from 1.8% to approximately 2.5% of the total retail loans disbursed. And it’s not stopping there—by FY 28, digital lending is expected to make up about 5% of the market, growing at a whopping 40% CAGR.

Will it last?

The median age of Indian population is around 27 years, which means that over 50% of the population is below 30 years and yet to become active consumers of financial services. Combine this fact with the efficiency of digital lending systems and the modern fintech promise – a 2-minute loan journey.

As Gen Z continues to mature and millennials advance in their careers, digital lending is likely to be a major channel for accessing credit further, sustaining consumption-driven borrowing for a long time. Continued increase in per capita income could further encourage consumer borrowing.

However, given the level of our economic development, credit moving from the supply side (businesses) to the demand side (consumers) of the economy appears to be a premature move that could derail the ‘India story’. To my mind, a balanced ‘India story’ requires industry to regain its share of banking credit for sustainable economic growth. I’d love to know your take on the matter.