Co-Lending's Trust Problem: When Banks and NBFCs Can't See Eye to Eye

Something is not quite right with the current Indian Co-Lending Model (CLM). The RBI launched the CLM in November 2020, which seemed to be the perfect solution to a persistent problem. Banks would offer low-cost funds, and NBFCs would leverage their on-ground presence to boost credit flow in India’s priority sectors like agriculture, MSMEs, housing, education, social infrastructure, renewable energy, and others. The math is quite simple: banks hold 80% of the loan, NBFCs retain 20%, and borrowers benefit from the blended interest rates.

However, two years after its launch, banks and NBFCs are seen to be struggling with a fundamental human problem: trust.

Before we get into that, let’s quickly understand how the co-lending model typically works. An NBFC identifies a potential borrower, often from an underserved market where traditional banks hesitate to venture. The NBFCs conduct the initial assessment using their credit assessment technology and alternate data points. Then comes the tricky part - this proposal by the NBFC goes to the partner bank for assessment. The loan is disbursed if approved, and both parties share the risk, albeit unequally.

The co-lending model is perfectly executable on paper; with banks bringing in their low-cost funds and NBFCs, their last mine reach, they would crack the priority sector lending. But it is turning into a classic case of ‘easier said than done’.

Well, it’s not simple to execute. Banks are accustomed to their traditional credit assessment methods. With the Co-Lending Model (CLM), they are looking at borrowing from sectors they have historically avoided, being evaluated via methods they are not entirely familiar with. This has resulted in banks rejecting up to 45% of proposals sent by the NBFCs.

NBFCs, on the other hand, believe their understanding of local marketing with their sophisticated analytics-based assessment gives them a better insight into borrower quality. Their success in priority sector lending comes from their ability to look beyond conventional metrics as they understand local business cycles, informal cash flows. But translating this understanding into bank-acceptable documentation is a herculean task.

Banks also charge a higher risk premium to compensate for what they see as incomplete information. This drives up borrowing costs, pushing away better borrowers and leaving behind a riskier pool.

Varying risk assessment methods lead to conflicting evaluations. And somewhere in this maze of processes, the original goal of affordable credit gets lost. It's a self-fulfilling prophecy; the very thing banks feared is becoming a reality.

The cost of this mutual distrust isn't just operational; it's affecting India's broader financial inclusion goals. Large NBFCs are entirely staying away from co-lending. Banks are spending extra resources on duplicate underwriting. And somewhere in between, worthy borrowers from priority sectors miss out on affordable credit.

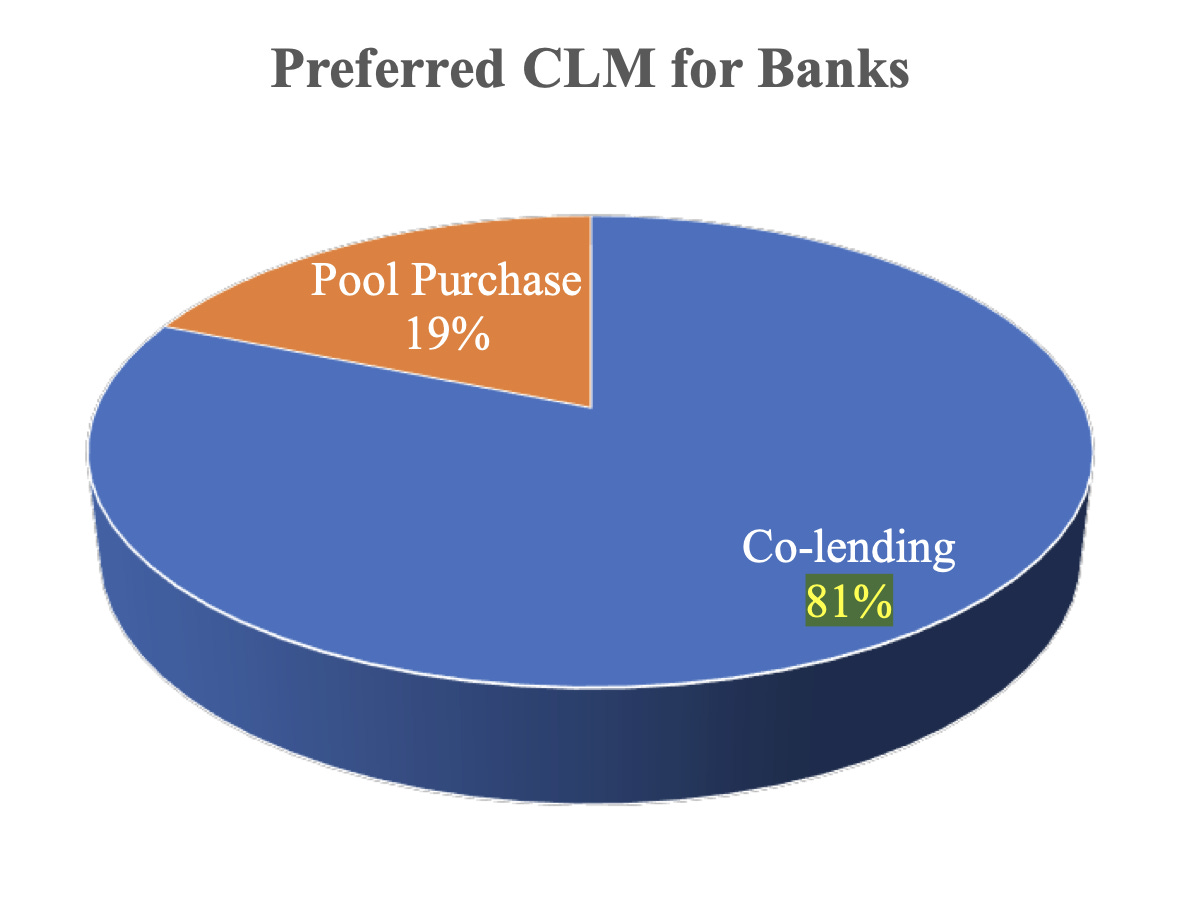

However, there is a positive factor often overlooked in the rapport between the two institutions. About 81% of banks prefer direct co-lending over pool purchase of loans i.e. purchasing a bundle of loans from NBFCs. Co-lending gives bank better control over credit quality through individual loan assessment. There’s a clear benefit for both involved, however, the change needed to make this work will come with technology.

Some banks and NBFCs are experimenting with a unified credit assessment framework. NBFCs can find it easier to present their cases when backed by data-driven insights. More importantly, the tech can create an audit trail that both parties can trust. Others are working on common credit policies that blend traditional banking metrics with new-age analytics.

Advance bank statement analyzers could emerge as common ground between traditional and alternative lending approaches. Additionally, BREs, i.e., Business Rule Engines, can streamline credit decisions, making the approval process more objective and less reliant on individual interpretation.

For the co-lending model to flourish, banks and NBFCs need a bigger mindset shift. Banks need to recognize that traditional metrics might not capture the full potential of priority sector borrowers. NBFCs need to appreciate banks' need for standardized assessment frameworks.

The stakes are high for India's priority sectors. They desperately need the credit that co-lending promises to deliver, and the trust deficit in the current collaboration will be a barrier to financial inclusion.

The question isn't whether co-lending can work; it has to work! The real question is, how do we create a system where trust becomes less about faith and more about verifiable data points both parties can rely on?