Can neobanks ever replace banks?

Not in India. Not yet.

Hi,

An hour of failure in UPI payments can cost a large bank over 400,000 transactions, according to NPCI data.

There are a few inferences we can make from that statement -

Banks’ IT architecture is unyielding, systems are ineffective and the skill sets of banks; IT department of banks isn’t up to the mark

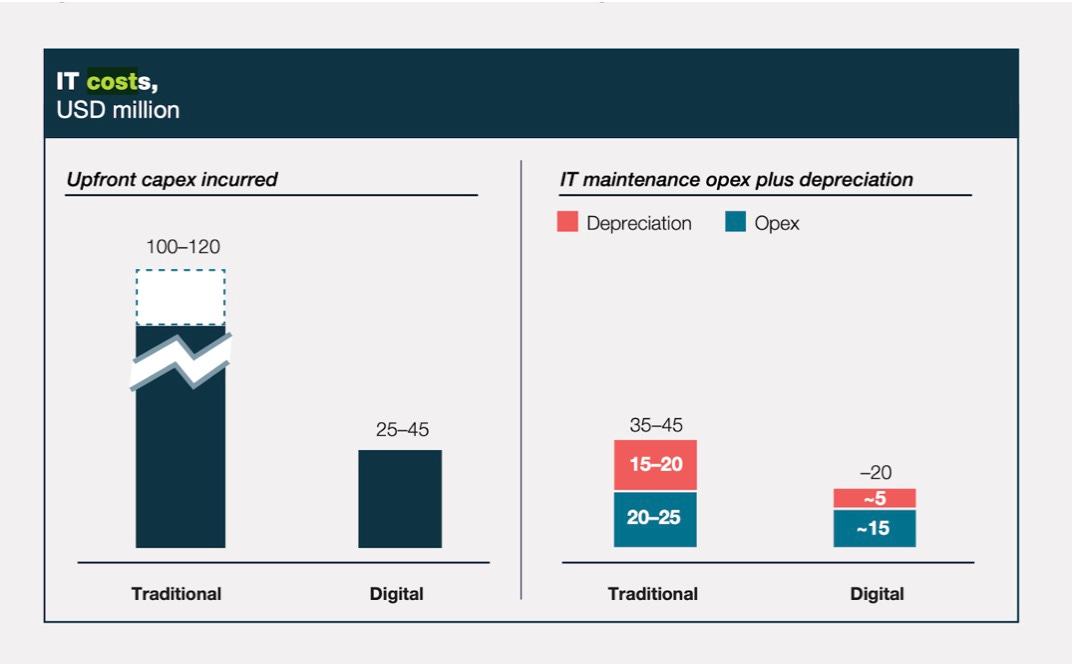

Banks’ spending on IT has gone up, but either it's not enough and/or not directed towards the right resources. A PricewaterhouseCoopers partner told the Ken that banks have gone from spending 1-4% of their net income to 2-5% on IT; however, spending needs to be at least 10% of net income to truly be digital.

Small ticket transactions have increased, which means the lack of robust infrastructure is being felt. Especially given that the cost of a digital transaction—be it for Rs 1 or Rs 1 lakh —is the same as it taps the same resources. This is choking banks’ IT systems.

I know this paints a rather gloomy picture of banks and the most popular inference to draw would be that Neobanks will replace traditional banks.

Nebanks are nimble and agile - they have much lower acquisition costs, as low as one-tenth of the acquisition cost of a traditional bank; operating costs per customer are lower as well.

Source: Mckinsey

Notionally, anyone would agree that most consumer neobanks are great and have the potential to break banks. And why not -

There’s (usually) no minimum balance requirement

No (usually) transaction limit/free transactions

They’ve got a good NPS score, as good as traditional banks

Quick procedure to join and easy to use

No server issues (hopefully)

Customer support 24*7

Faster UI/UX

The short answer to whether neobanks will break traditional banks: probably

The long answer:

That’s the case for banks that are unwilling to modernize their IT architecture and systems. It's a pretty straightforward argument, customers expect simple, fast and immediately rewarding interactions with their banks; so being truly digital isn’t good to have, it's both expected and preferred by customers.

There’s no denying that the rise of FinTech and digital banks has strained traditional banks’ IT operating models and almost forced them to reevaluate their customers’ needs.

Speaking of which, FinBox is hosting its first-ever live webinar on how FinTechs can unlock the $350 billion lending opportunity for MSMEs. I’ll join my colleague and co-founder Srijan, longtime peer Arihant from IIFL and Kushal from Vyapar to discuss this massive opportunity in MSME credit. Make sure to sign up!

The digital v traditional debate has long quizzed financial leaders. Jeffery Pilcher, CEO and President of The Financial Brand believes the digital revolution is now a ‘mandatory survival strategy’ and that the debate is centred around just how quickly banking can be unbundled and margins slashed.

Some others like Raman Bhatia, digital chief of HSBC in the UK and Europe believe the David versus Goliath debateover digital players challenging big banks is ‘overblown’.

The debate really then boils down to two combative forces - neobanks offer superior customer experiences and traditional banks have the license to lend and have earned customer trust. At its core, this gives legacy organisations a competitive advantage.

By that logic, It’s easier for banks to be neo than it’s for neobanks to be THE BANK!

Case in point - State Bank of Mauritius (SBM)

Corporate banking has been SBM’s bread and butter. For March 2021, corporate banking represented nearly 63% of the bank’s deposits. But then it turned its head towards growing its retail presence. How did it do that? Hitched a ride to India’s burgeoning FinTech scene.

SBM claims to have customers across 500 Indian cities, and its assets under management grew more than 3.5x to Rs 4,739 crore for the year ended March 2021. What’s incredible is that it did so with just eight branches and only 250 or fewer employees across the country.

In an interview with The Economic times, Managing Director and Chief Executive at SBM Sidharth Rath said “Starting my own branch network will take years and is very capital intensive. A metro branch costs Rs 1.5 to 2 crore”. Makes sense then that the bank has employed the FinTech partnership-led model and has over 30 different FinTech firms working alongside it. Some of the big names include Lendingkart, Slice, Uni and LazyPay.

That’s one thing, but this story by The Ken posits that one of the reasons SBM has been able to make a dent in Indian fintech is its agility. I agree - most banks have too much bureaucracy in the form of hierarchy that usually makes ‘digitisation’ a trundle.

There are a bunch of complications in the form of regulation, exclusivity from FinTech firms (who’d want to work with more than one banking partner) and customers who’re sometimes completely unaware of SBM in a meaningful way (since the FinTech partner becomes the face of the operation). But that’s for another day.

The idea is simple - if you can’t digitize, then delegate. And an even simpler idea to grasp? Banks have ALL the power.

Banking sector loans in India are Rs 110 trillion, of which, Rs 55 trillion are borrowed by companies and the rest of the Rs 30 trillion are borrowed by retail customers. Despite FinTech firms having a good leg up in the scene, banks seem to know their retail customers better than FinTech firms - at least as of today.

The way I look at it, banks need to capitalize on the four pillars that give them the power -

Trust - Trust is the foundation of banking. It’s difficult for neobanks to beat the tenure and long-standing branding of nationalised banks.

Regulation - Banking is possibly one of the most heavily regulated sectors. The regulator - Reserve Bank of India - has put its guard up with the entry of FinTechs and the thousand different ways it impacts business and customers. And banks have an upper hand because they’ve been navigating the regulatory maze for aeons. Besides, some regulations around neobanks w.r.t. processes and allowances for neobank are still hazy.

Technology - Banks may not be the first movers when it comes to technology adoption but they are certainly on the right path. It’s only because of the sector’s concerted push that we have UPI and AA. While tech-first and digital FinTechs can reach customers not serviced thus far, banks do have an inherent advantage of being able to build the right assisted products and leverage their physical networks to serve customers even in the hinterlands.

License supremacy - While neobanks stitch together a bank-like experience using technology and business partnerships, banks have the ultimate license to not just lend but also accept deposits, provide payment systems and whatnot. This means that the pecking order will always require a bank’s backing.

When the ATM was first introduced in 1967, bank employees were wary. They thought it would render the human teller obsolete and a considerable chunk of bank employees would be out of work. But clearly, that’s not been the case. We did an in-depth study of the bank branch statistics that revealed some interesting insights. You can read that piece here.

It’s safe to say that the current debate of whether new-age players will dethrone the legacy lenders lacks nuance. That nuance must come in the form of a deeper understanding of the larger regulatory and business context. It’s clear that, at least in India, a FinTech will have a much harder time building a viable business than a licensed bank that’s steadily digitizing will find it to retain its customers.

Hope to see you at the webinar!

Cheers,

Rajat