Can BNPL the challenger turn into a champion? 🏆

I miss the old grocery shopping days.

Walking to the local kirana shop, trying to stick to the week’s grocery list, but almost always falling for last-minute impulse buys at the counter. Not to mention, the complete disregard for whimsical ‘no credit’ signs – why bother to make change every few days when you could clear your dues in one go at the end of the month?

Burgeoning digital payments and e-commerce have ushered in a new digital transactional order. The last vestiges of shopping in the analog age are becoming fewer and fewer to sight – almost quaint.

But that’s just a half-truth.

We have managed to accommodate shopping behaviors like short-term credit in this new regime. The humble ‘udhar’ is polished and packaged as ‘BNPL’, and a niche industry is now swarming around it.

Current state of BNPL

Strictly speaking, BNPL wasn’t the first product of its kind to be introduced to the market. Credit cards (within the no-interest period) and no-cost EMIs were already there. How did it make a place for itself in a somewhat saturated market?

As digitally native demographics like millennials and Gen Z capture spending power, they are also embracing digital payments and credit. BNPL providers leveraged this opportunity to build an irresistible value proposition.

")

It solved the gaps left behind by credit cards in one fell swoop, catching up to their market share at stunning speed. In FY20 alone, BNPL made up ~37% of the volume (even though the total value of transactions are lagging) among all retail digital lending by banks.

Within just two years, the number of BNPL users in India have grown to 10 million, poised to comfortably knock out the reigning champs in the space – credit cards with their ~35 million users.

")

This growth is the result of several catalysts in the economy. The role of e-commerce in the rise of BNPL, for example, is uncontested. In the B2B context, especially, it can make MSME purchasing flexible and improve crucial platform metrics like CLTV, average order value and retention.

But a larger question looms –

How do BNPL providers make money if they don’t charge interest?

BNPL comes in many flavours

One crucial way in which BNPL differentiates itself from products in its category is that there is no single model at play. It cuts across several business models based on distribution channels, user type and the merchant’s ecosystem – and at many intersections of these categories.

")

How does each of these weigh against the other to make the most business sense? Let’s break down what the research indicates:

Merchants with proprietary models or wallets enjoy higher customer stickiness as the lending journey is deeply ingrained within their own ecosystems. They are also better placed to charge merchant discount rates than open-loop players who offer BNPL plug-ins. However, the latter can encourage faster adoption and scalability.

Incumbents like banks and NBFCs, wallets, and to an extent, marketplaces cater mostly to existing customers. FinTechs have an upper hand as they can expand to new-to-credit customers.

B2B BNPL providers win in terms of monthly spend compared to their B2C counterparts. They are also better protected from delinquencies.

Notwithstanding these trade-offs at a granular level, the overall business strategy should be guided by the lender’s purpose.

Where the money flows

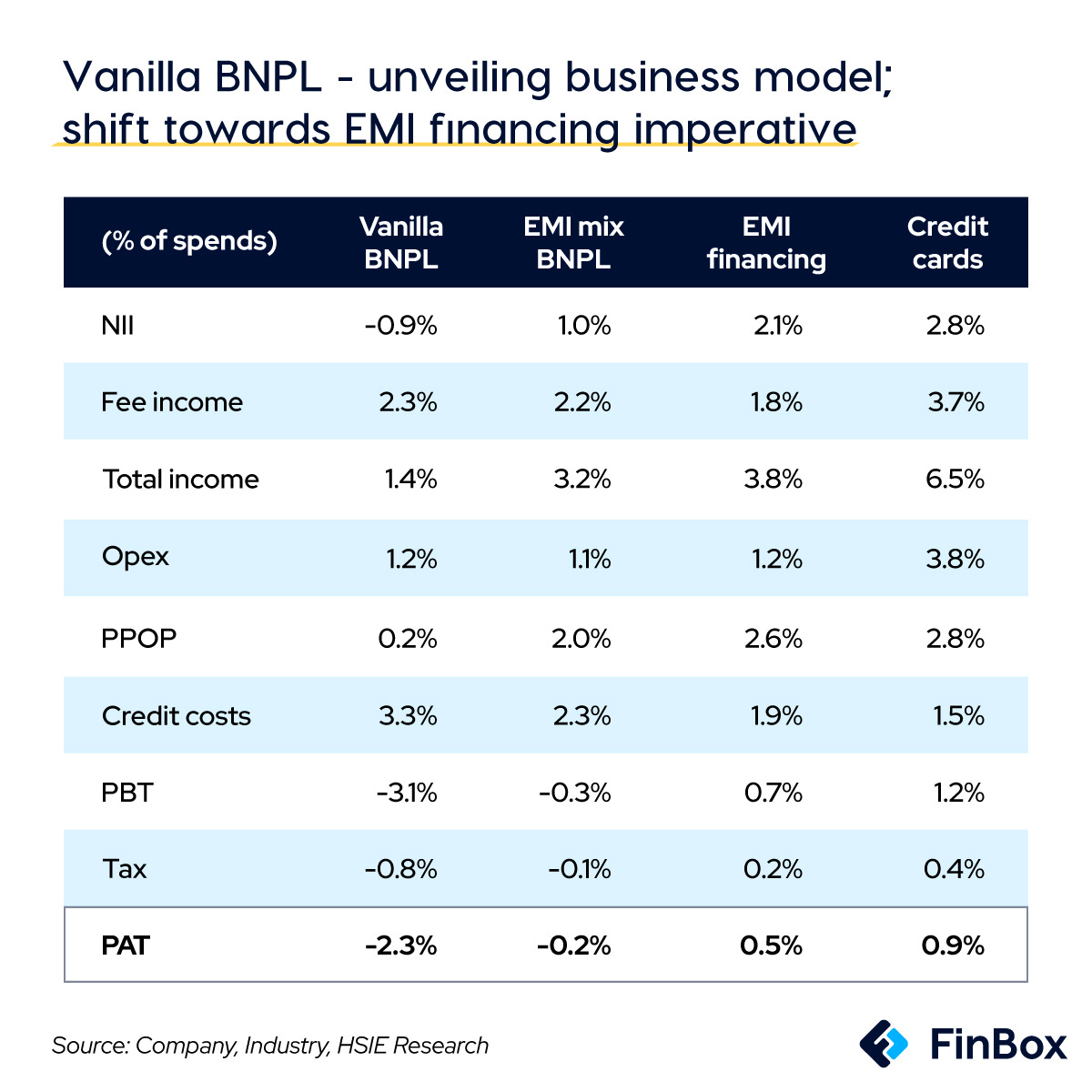

Irrespective of their business model, all BNPL products can be broadly categorized into credit products or convenience products. Convenience products are the more widely marketed 10-30 day interest-free period micro loans to be repaid in bullet installments. Credit products lean towards a more traditional approach, often to be paid over an interest bearing tenure of three to 18 months.

The cold truth is that convenience BNPL – the darling of FinTech in India – is not a revenue-generating model. It suffers from negative net interest income and overall losses when compared to credit cards, its closest competitor. Pitted against credit cards, the value proposition of convenience BNPL also shrinks — shorter interest-free periods, smaller credit limit, limited rewards, only domestic acceptance and inability to transfer balances.

Does that mean BNPL is a lost cause?

Certainly not. Convenience or ‘vanilla’ BNPL continues to be the gateway for customer acquisition. In fact, it helps tap into and groom potential users whom incumbents shy away from. For instance, it gives new-to-credit customers a chance to not only access credit, but also build a credit score.

But from the perspective of profitability, that’s all it should be – a gateway. Credit BNPL, which encompasses EMI financing (both no-cost and with interest), is where lenders and credit enablers generate positive revenue. Effectively, convenience BNPL becomes the fulcrum of customer acquisition following which users can be cross-sold more viable and income-generating EMI products.

")

However, to create a prudent business model, BNPL players must fortify revenue generation by expanding beyond interest payments to other revenue streams.

Late fees are charged based on the total bill amount as well as the overdue period. User accounts are often frozen until their dues are paid. It’s important to note that even though BNPL late fees are lower compared to credit cards, they do form a higher percentage of the spend compared to credit cards. However, late fees as a high share of revenue signal a poor portfolio. Lenders must keep a check on these to ensure sustainability.

Activation, subscription and convenience fees can form a portion of the total revenue share at the time of acquisition or when EMI financing is activated. However, this can diminish the value proposition of the product since most players in the space provide the same services without any fees.

Once a user is elevated to a form of EMI financing, a BNPL provider can start charging merchant fees like MDR and subvention. This can potentially account for a bulk of the revenue share as merchants are better positioned to pay service fees due to gross margins.

BNPL players must pivot towards a strategy that prioritizes this category to create a truly sustainable revenue model.

From captive to fluid customer bases

With credit cards still in possession of a chunk of the market share, BNPL has a long way to go. One interesting way BNPL can make inroads is by striking at their weakness – credit cards are still perceived as vanity products.

As captive customers ascend the social ladder, they are likely to shed perceptions of having risky profiles. At this stage, BNPL providers risk losing them to credit card providers offering lower interest rates and higher prestige. These losses may be difficult to sustain, but BNPL players can continue innovating for those far down the ladder – aspirers and the next billion – to protect themselves from such graduation risk and ensure a steady stream of socially mobile customers.

")

Conclusion

Digital lending has seen immense success due to regulatory arbitrage. However, growing scrutiny will take away from customer experience and cost BNPL players more in terms of compliance. The expected incoming restriction on first loss default guarantee (FLDG) will also impede growth in the future.

In FY21, digital lending accounted for ~30% of investor funding. But as VCs brace for an economic downturn amidst waning enthusiasm for tech (if stock markets are any indication of market sentiment), BNPL players must likewise prepare and shift their focus to boosting profitability. I explore this in detail in this piece.

Revenue generation is on everyone’s mind, as it should be. It remains to be seen how BNPL players will build a financially viable business around an offering that’s achieved acceptance and product-market fit.