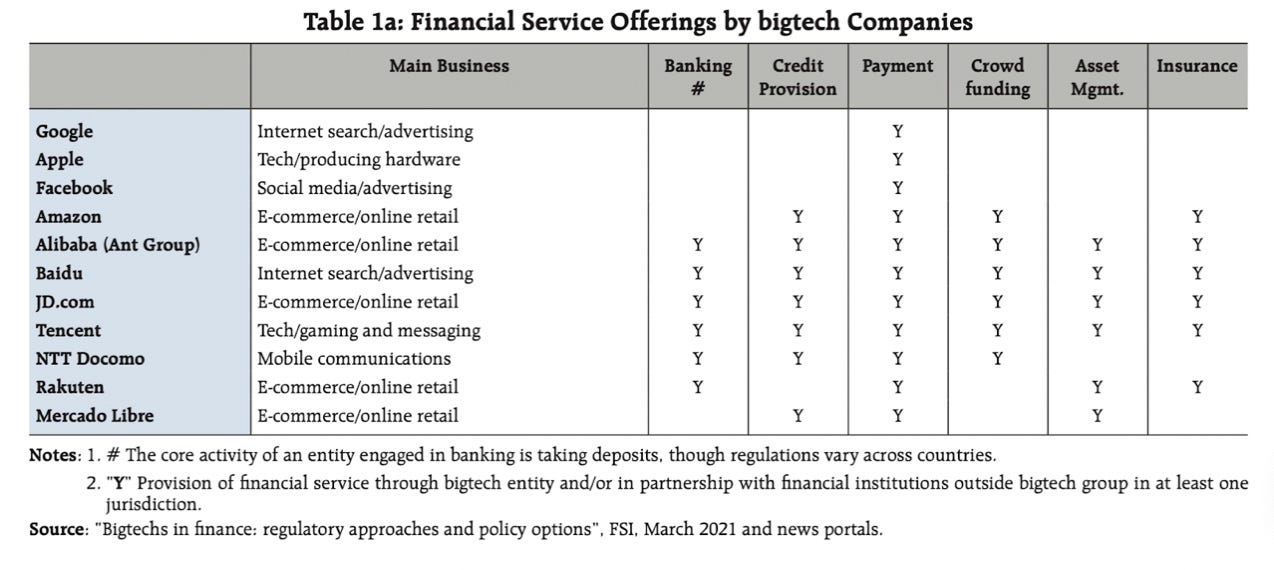

Banks are the antidote to Big Tech in Financial services

Big Tech serves advertisers, and banks serve customers.

Hi,

Before December 2020, China’s tech entrepreneurs were considered icons - everybody’s favourite rags-to-riches stories, their guile and contempt for the rulebook earned them cult-leader statuses. But like the fate of all cults, there was growing anger at their obscene wealth; then came the regulatory scrutiny that wobbled the perch of these previously untouchable tycoons.

It was the beginning of the fall of Big Tech in China.

Big Tech companies have had it relatively easy on the competition front in India. That's until the two-decade-old Competition Commission of India (CCI) slapped a penalty of Rs 1,338 crore ($162 million) on Google for abusing its dominance in the Android ecosystem, just last week.

Pocket change for a company valued at over $1 trillion, which earned 10 times the penalty in revenue from the Indian market in FY22.

But it makes me think about what the implications of the Big Tech antitrust would be for financial services and banking.

Quick context on the allegations against Google

Reduced the ability of device manufacturers to opt for alternative versions of its Android mobile operating system.

Search manipulations where GooglePay appears on the top when a user searches for a payment use-case such as recharge on (Google search);

Leveraging Google properties and data such as YouTube and Play Store to plant advertisements for its payment service, through ad personalization

It doesn’t allow developers to access key features via forks (think of forks as literal forks used to pick up food) to develop key parts of the software of competing for android versions.

Any app that can’t afford to be on Playstore either because of the commission it charges or due to policy issues, cannot even be downloaded as an APK file without users being warned of how harmful it will be for their systems.

That’s just the tip of the iceberg. In god we trust, In Big Tech we antitrust? Is one of my favourite stories from last year. It was about Big Tech’s tussle with US and Indian antitrust laws, concerns of competition regulators around Big Tech’s monopoly, Big Tech’s foray into India’s financial sector and how it's making financial regulators anxious. Should give you a fair idea of why big tech gives regulators the shivers.

And why shouldn’t it? (don’t answer that, it's rhetoric).

What's the biggest leverage that big tech has? The network effect. Where does that come from? Data.

An asset far more valuable than oil, data makes these internet platforms more onerous than industrial monopolies. Why? Data is iterative, it's non-rivalrous, and as a result, makes the Zuckerburgs infinitely more powerful than the industrial barons of the 20th century.

The amount of data being produced is doubling every two years, equating to a 50-fold increase from 2010 to 2020. With machine-generated data, it's expanding at roughly 50 times the rate of traditional business data.

This data explosion gave rise to aggregators to help gather, organise and manage data. The western argument is that the data aggregators, the ones that are “free” (think Twitter, Google, Facebook and the likes) and the ones that monetise via services (think Netflix, Uber and the likes) have the demand side economy of scale. That’s essentially the network effect, by virtue of which, more users of a product make that product better.

Take Google, for example, the more people that use it for search, the more data there is to train the algorithm, and the better the search results become, attracting more users; a self-reinforcing virtuous cycle.

Vast amounts of data have been aggregated by data platforms to better manage the flow.

Network effects in lending?

And in lending, data is key. Large tech platforms will likely be able to outperform banks in calculating financial risk. Lending products are risk-dependent, and platforms may have an advantage there: From Google’s search cues to Amazon’s extensive data sets on spending habits, coupled with their machine learning capabilities, Big Tech’s advantage is an exceedingly precise understanding of the market and consumer behaviour.

But lending is also about building the right risk predictors. That comes with expertise in data science and risk modelling - this is where financial services win. The core idea of this argument is to view banking and the rise of embedded finance as a vertical SaaS solution, rather than a horizontal SaaS solution (which is what Big Tech is).

Look at Toast - In September 2021, Toast went public, just a decade after the company was launched at a valuation of well above $30 billion. But like most public SaaS companies, Toast saw a sharp fall in its valuation to about $9 billion - still healthy and indicating investors’ belief in the company in the long term. It started out as a point-of-sale solution thatsolved a particular problem for restaurants (i.e., collecting customer payments) to a comprehensive back-of-house management system.

The way I look at it, Toast’s success even in turbulent market conditions suggests something deeper is at play, the secret sauce that could potentially help to lend. For Toast or any vertical SaaS business or any lender that aims to replicate that success, it is pivotal to understand their customers’ workflows in order to identify unmet needs and key control points in the flow of information through a business.

The Big Tech data threat holds true, but India is a fragmented country with markets that go beyond the reach of the Amazons and Flipkarts of the world. And I’m in the business of B2B lending, and at FinBox, our goal is to democratize credit for the next billion, basically extending the reach of formal, fair and seamless credit beyond the few millions in urban centres with access to smartphones.

And how can B2B lending be contextualized without Big Tech data? Data from ONDC and OCEN. When you think aboutwhat ONDC can do that Big Tech can’t, it's the opportunity for banks to tap into markets where they don’t have a branch presence or relationship with customers there.

Cities below the tier-2 category have become the focus of banks, whether private or public, and ONDC will help penetrate this space. What’s better, add a layer of OCEN and every interaction can be captured digitally. This can prove to be a goldmine of contextual data that helps improve processes across the loan’s lifecycle - from underwriting to collections and cross-sell.

Any company today can become a fintech, and almost anybody with ‘data’ can theoretically get into the business of lending. But here’s where I think financial services can make a dent in Big Tech dominance - reliable extraction of contextual data and building the right risk predictors.

So, when we think about banks as the trusted source for lending, the idea of who holds all the data flips on its head. Big Tech’s advantage is that it has been able to create ecosystems which exploit economies of scale across products and services. Couple that with big data analytics and the ecosystems become protected by high exogenous and endogenous switching costs. This makes big tech platforms gatekeepers, who monopolise the interface with an important segment of customers.

But we’re in 2022, and by virtue of the Account Aggregator framework, ONDC, OCEN and the mind-blowing innovation ecosystem in the country, licensed lenders - banks and NBFCs - will be the Big Tech. They will be data aggregators as well as data users; that combined with vertical integration to offer consistent and high levels of customer satisfaction means that the threat of Big tech might somehow be null and void. In theory at least.

Much like Toast, a better model to compete with Big Tech would be a vertically integrated open platform. Vertically integrated to take advantage of banks’ execution capabilities and expertise in risk assessment and offering a small number of own-labelled products where they have a competitive advantage (like secured lending). And the open platform would be open to allow banks to offer products/services from third-party providers (as in the aggregator model) but being vertically integrated would mean it could be delivered faster and with less friction.

TL;DR

An author I keep going back to Steven Johnson, (who largely writes on the intersection of science, technology, and personal experience) described Big Tech as “the single most influential concentration of new wealth and information networks in the history of humankind.” China’s antitrust crackdown on its Big Tech shows the impact of these giants and how it is undoubtedly colossal. It showed the world the fear ignited by these tech mammoths and why antitrust agencies had to go in guns blazing to curb their power. Here’s a good read on that.

Big Tech serves advertisers, banks serve customers. That statement speaks for itself, especially in a world where trust is in a positive decline.

Big Tech’s biggest flex? Data. They’re custodians of petabytes of data, but everybody knows that malpractices there can cause non-negotiable negative externalities.

We don't necessarily need Big Tech data in India. We’ve got deep financial data pipelines in the form of innovations like ONDC & OCEN to provide contextual data, necessary for lending.

Big Tech has nothing on banks that have years of experience in risk management - an exercise that gets easier ONLY with experience and not JUST data.

Banks need data custodians, they need to be trusted aggregators. This adds value not just to the many stakeholders (customers, banks, fintech, etc) but to society itself. They're not in the business of monetising data for advertisers.

So, really, the antidote to Big Tech in financial services is banks themselves. I would love to hear your thoughts on this.

See you next week!

Cheers,

Rajat