Banks and FinTechs must stop stealing away each other’s customers

What does it take to build a successful fintech company? Or any company, really? Are you building a riveting product that people want and can you distribute that product efficiently and reliably?

I’d think most founders wrestle with two challenges - manufacturing and distribution.

Let me explain the context.

A simple two-paragraph announcement by the Reserve Bank of India (RBI) earlier this month closed a loophole that gave birth to billion-dollar companies and resulted in more than a million credit cards being issued every month!

I wrote about it last week, you can read it here to refresh your memory.

No doubt there’s more regulation incoming for digital lending and my guess is, that it will look like a replica of existing lending regulations. Maybe the extra layer for fintech will be tighter KYC norms for technology players.

Here’s the thing right, regulation is inevitable, especially when it involves people’s money.

And if fintechs want to compete in the big league, sooner or later, they’ll have to either consistently innovate faster than legacy players and/or build distribution pipelines reaching farther and wider than their big brothers.

Or risk becoming irrelevant.

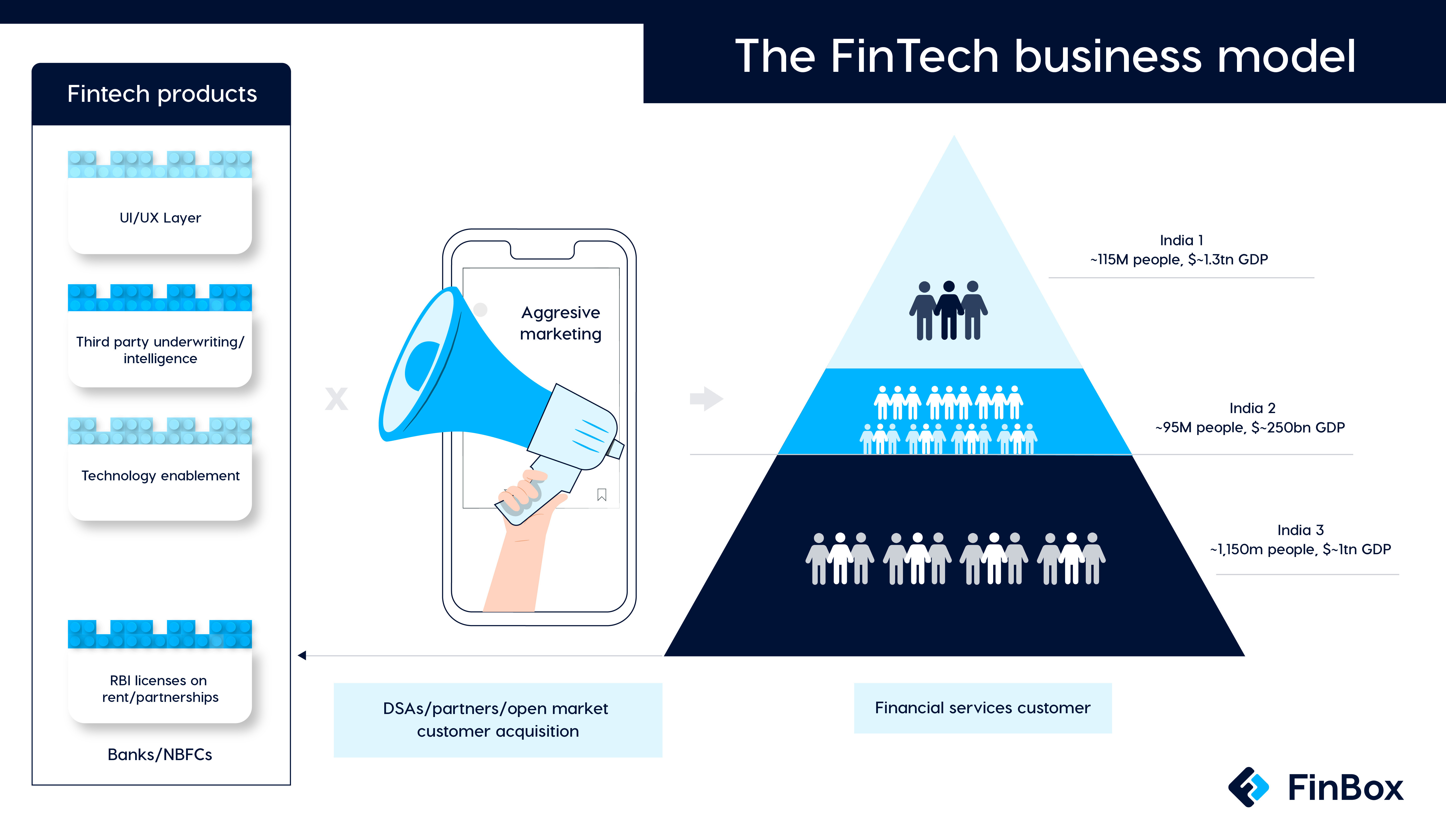

A quick look at the business models of B2C fintech companies today will reveal two things -

They’re serving largely the same customers that banks are.

The big boys with the lending licenses hold all the power and can theoretically shut fintechs’ business pipelines whenever they want.

This brings me back to the two inherent challenges of running a business - manufacturing and distribution.

The question that’s interesting to me is which challenge do you start with?

Obviously, the answer depends on a number of specific factors — the customer problem that is being solved, the founding team and their very particular set of skills, etc. — but I also think it depends on the ‘era’ in which the company is being founded.

The end of the manufacturing era

I’d say, the fintech manufacturing era began roughly 15 years ago and has now reached its tail-end. And ironically, the success of fintech over the last 15 years has created tougher conditions for companies using the ‘manufacturing-first’ strategy of their predecessors.

No doubt that the absolutely staggering amount of VC money in fintechs is profound - in 2021 alone, private companies raised a record $621 billion in venture funding globally, and one of every five of those dollars was invested in fintech.

Despite being the VC world’s whizzkid, making a differentiated product is difficult; especially with strong unit economics when you and all your competitors are relying on largely the same licensing arrangements and true innovation comes harder than a cleverly cobbled-together product

And this challenge gets compounded when you realise that your competitors are catching up and copying all your cleverest and most ‘unique’ product features, which forces you to do the same or risk falling behind.

So what’s a clever fintech founder to do?

Enter the age of distribution

First option - buck the fintech infrastructure trend, take all the time you need to build a differentiated offering. There are plenty of unmet financial needs that fintech can solve!

Alternatively, you could move your strategy away from manufacturing and on to distribution.

I’d think this is the path we will see a majority of consumer fintech companies take over the next decade.

In fact, we already are.

Convenience v community - a tale of two Indias

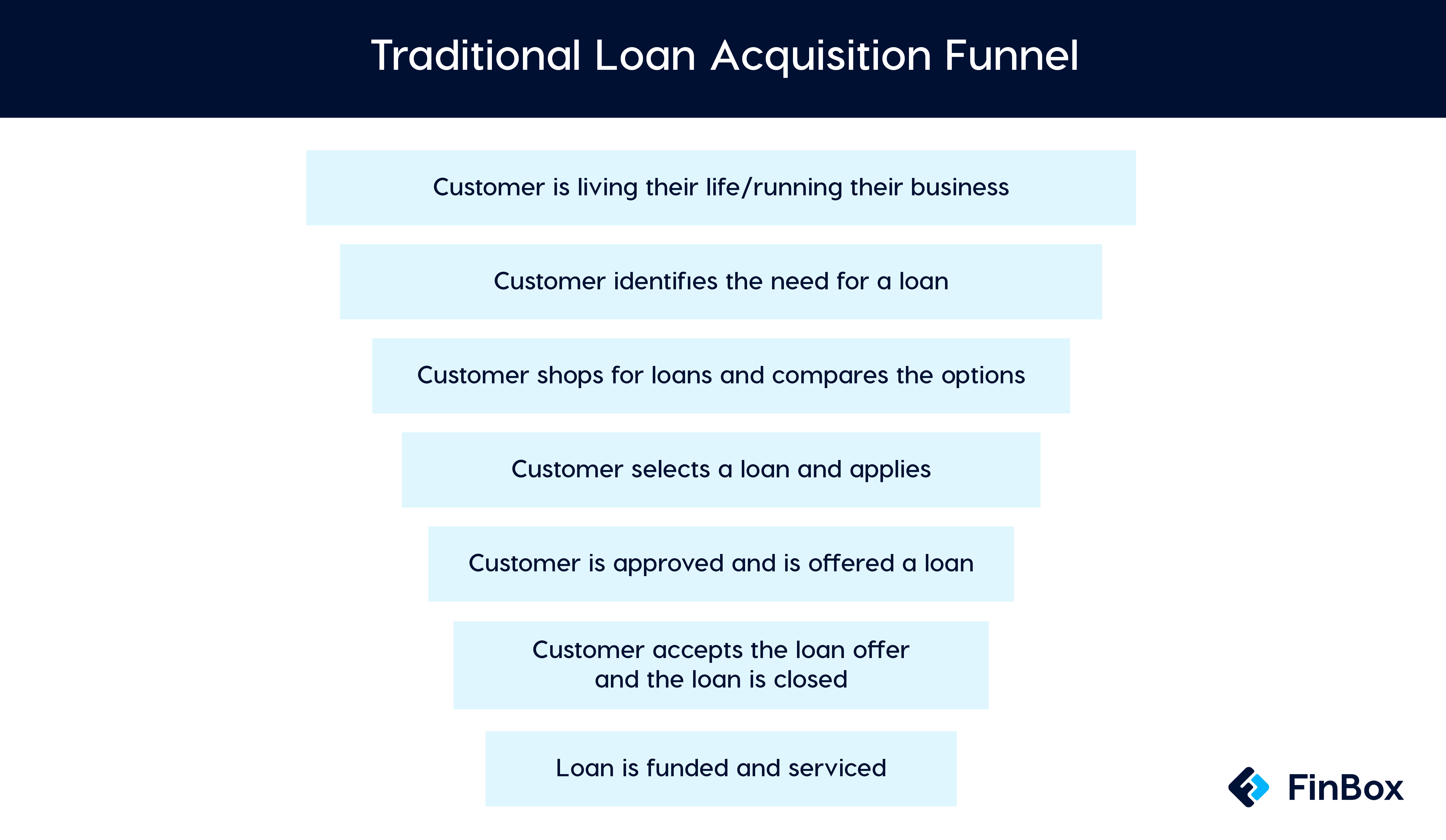

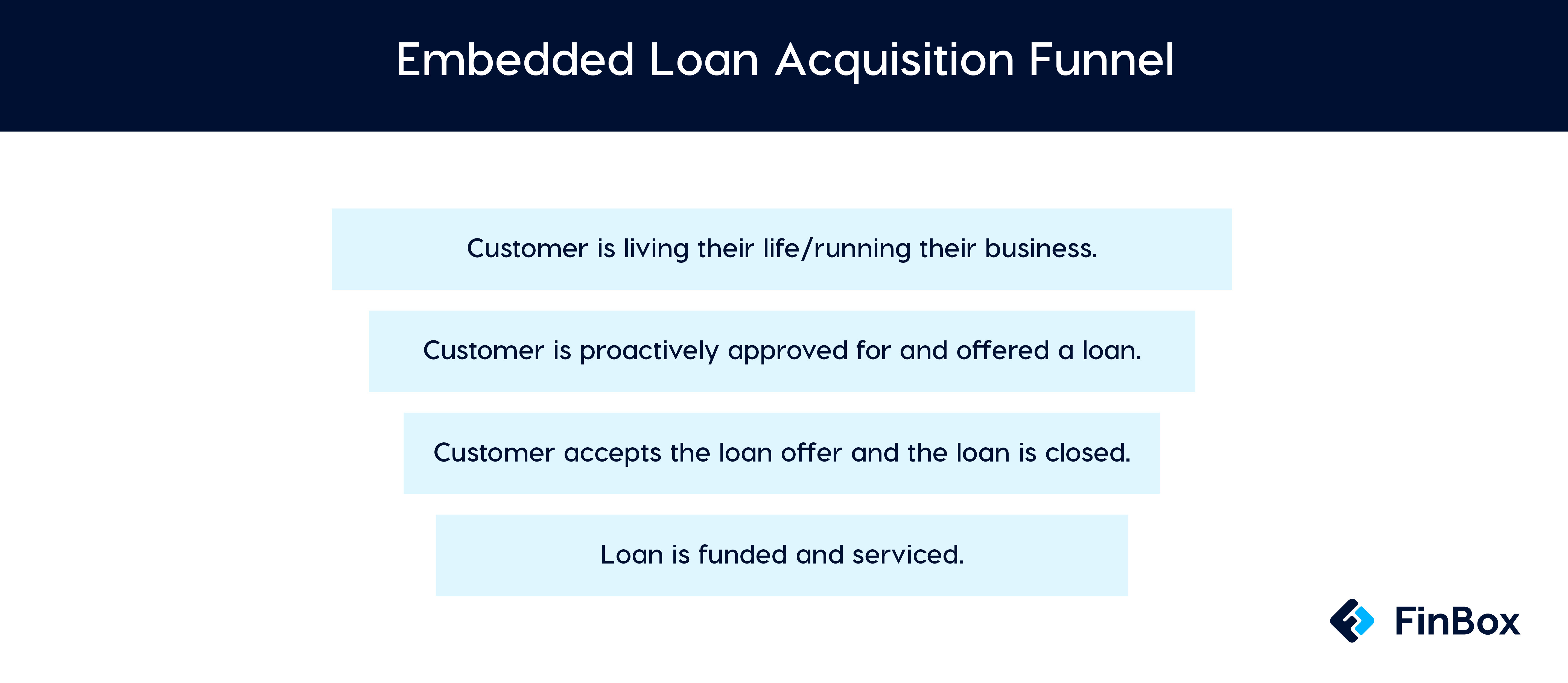

The value proposition that most fintechs were built on - convenience. The idea was to make banking as easy as ordering food. This business model functions on the idea of making the acquisition experience easy - the details of the financial product itself are mostly immaterial to the customer.

Lending is a prime example. It went from this

To this

Successfully executing an embedded lending programme is hugely beneficial. For banks, customer acquisition goes from being extremely frustrating to a free service provided by your partners.

Also read: How lender can supercharge their conversions to increase loan disbursals

But convenience cannot be your growth strategy when there’s fierce competition, you’re serving the same customers that banks are serving.

We need to look deeper.

The case for community

With 190 million unbanked Indians, the potential for a community-based distribution strategy is immense.

Think about it - innovative distribution models can not only build in-roads from urban to rural India but can truly simplify user experience - and isn’t that what most fintechs set out to do in the first place?

A community-based approach to building a good mix of distribution channels includes local influencers, resellers or agents, various POS outlets such as Kirana stores and local bodies such as farmer producer organizations (FPOs) who’re using their existing customer base and journeys to sell insurance and credit offerings based on specific needs.

This ‘FinTech for the underserved’ report by PwC India provides the perfect example of a fintech distribution strategy -

Look at digital community banks in the US - Whether its Daylight (built for LGBTQ+ consumers) or First Boulevard (built for African-Americans) or Nerve (built for musicians), there are a few things that are clear -

Some communities have clearly identifiable, unmet needs; and if your distribution isn’t reaching them and solving a unique problem, your product is an affinity marketing play

Some communities have clearly identifiable, unmet emotional needs; and if your product isn’t reaching the right stakeholders, then any exercise in brand building and customer retention is futile.

Some communities are self-organized with a strong purpose; and if you’re not tapping into that and becoming an enormously important and low-cost acquisition channel for their needs, you’re losing out.

I’ll leave you with one pertinent question that we ask ourselves all the time -

This isn’t only about what your distribution strategy should look like (though that question needs pondering over and it will be consequential in your survival) - it’s a bigger question of the role of financial services in all of our lives.

How do we take the products we know, use and love to 1 billion people of this country and generate enough real value that there’s some left on the table to be captured?

I’d like to know what you think.

See you next week!

Cheers,

Rajat

CEO and co-founder

FinBox