After telecom, can Jio’s ambition change the face of financial services in India?

What does the next decade look like for financial services?

Hi,

When one thinks of a tectonic shift, what comes to mind first? An earthquake. A natural disaster of epic proportions.

However, not all tectonic shifts are this dangerous. In financial services, digitization and innovation have disrupted entire industries but the effect has largely been a net positive one.

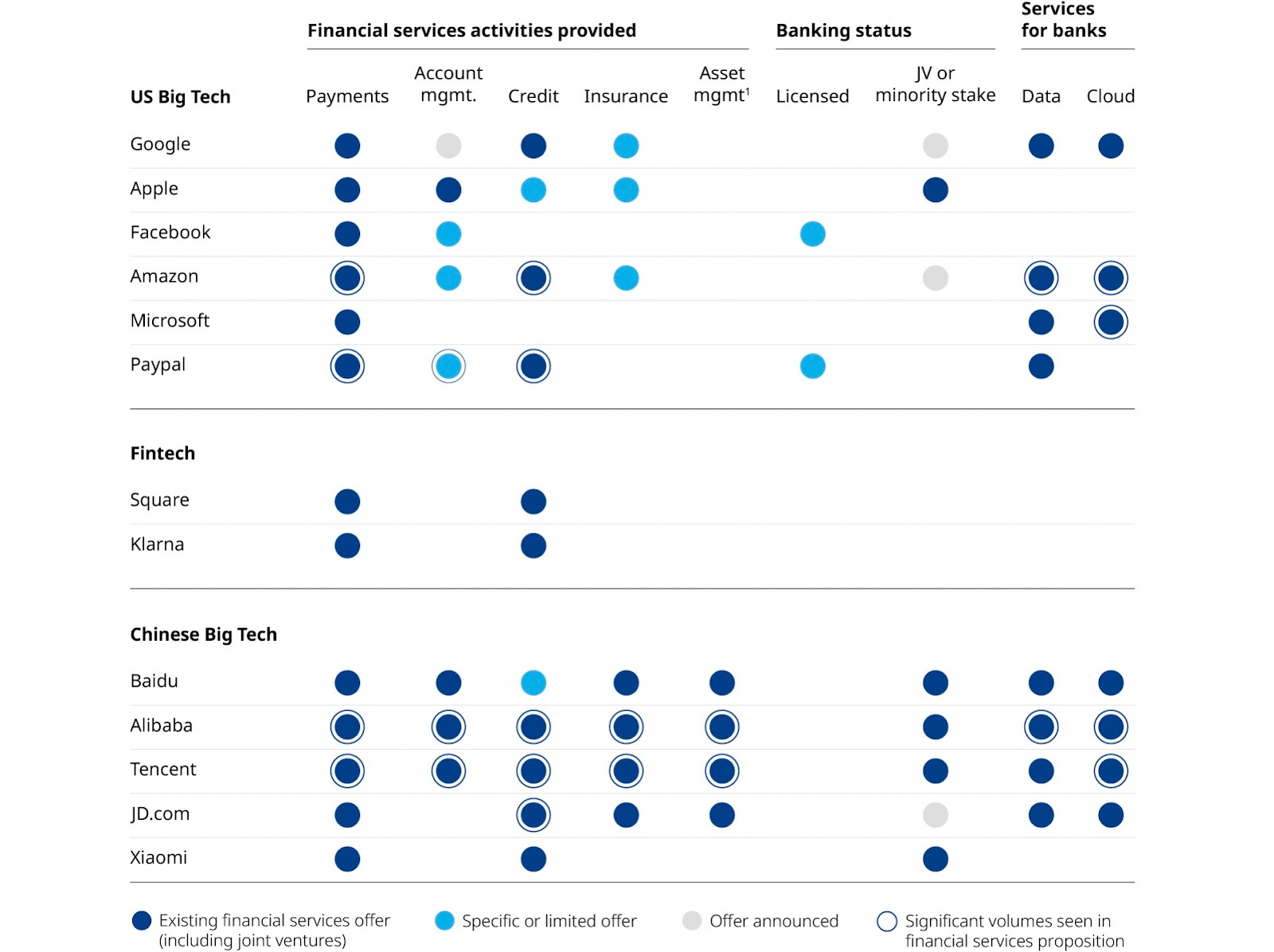

Source: Oliver Wyman

Looking at the above graphic shows us the disruption that big techs like Amazon, Apple, and Google have ushered. Closer home in India, Reliance Jio has ushered in the era of disruption - initially with telecom and energy and now with financial services.

The behemoth is getting ready to list its little-noticed financial services company - Jio Financial Services(JFS). It will be counted as India’s fifth largest lender by net worth, trailing closely behind top banks including Axis Bank and HDFC Bank.

I’m trying to figure out what this means for NBFCs and fintech. Consider this newsletter my rambling notes on this -

Jio has led the cost curve decline - Post Jio, the cost of 1 GB of data has come down from Rs 300 in 2016 to Rs 10 as of 2022.

It has created an entire digital ecosystem -

The Jio platform is an access enabler for 400 million Indians. It has created an entire ecosystem around its core competency (telecom)

JioMart - It serves merchants and the end customer. It’s doing what Walmart + Alibaba does in India

JioTV– good content is a bait and it's a very sticky business if done right. JioTV might be on the path to getting it right.

Other than the fact that these markers are what attract marquee investors towards Jio, it also means that Jio is our home-grown big tech.

Jio users consumed around 20GB of data every month in the final quarter of the financial year 2021-2022; data traffic exceeded 91 billion GBs in the financial year 2021-22, which marks an increase of around 46% year-on-year. To put that into perspective, here’s a vague factoid - to record all the words ever spoken by humankind, five exabytes of storage would be enough. One exabyte of data is about 1 billion GBs of data - that’s five billion GBs of data. Jio users consumed 18 times as much data in the last financial year alone!

All this data makes Jio the carrier with the largest single-country subscriber base, and it carries the highest volume of data globally, excluding China. When Reliance was starting out, their biggest question was probably - how to sell data in a developing country; Now that their consumers are literally guzzling data, what to sell next? One of the most straightforward answers is financial services.

People will always need credit. And current, traditional credit-scoring models leave out a large swathe of the unbanked population.

Credits: Reuters

But alternate data based underwriting models are picking up. Notwithstanding the concerns around data privacy, there are frameworks and innovations that enable data sharing and empowerment through a consent-driven framework. It has been demonstrated by Ant Group in China or MercadoLibra in Argentina or by what we do at FinBox even, creditworthiness can be gleaned from buyers’ and sellers’ transaction data via Account Aggregator framework; mostly from large online platforms. Jio already has a presence here, and that’s where they intend to go next - to a “consumer and merchant lending business based on proprietary data analytics to complement and supplement the traditional credit bureau-based underwriting”

Reliance, apart from owning India’s largest telco, the conglomerate also runs the country’s biggest retailer - it has over 16,000 stores sprawled across the country, enough physical touchpoints to build an omni-channel distribution system. It has what the Bank of International Settlements calls the ‘DNA loop’. The DNA loop, shorthand for data, network and activity - basically, big tech has all the data and the network from its platforms to get a headstart into financial services.

Big tech essentially has a large ecosystem of users across various platforms that generate a ton of data. This data can be a goldmine of insights and used to fuel algorithmic underwriting through machine learning models that take into account a more holistic range of indicators than just the credit scores of the consumers.

RIL’s $200 billion balance sheet! This allows the company to exploit the cost-of-capital advantage and take bigger risks.

The jury’s out on whether or not it could potentially disrupt the financial services just as it did in telecom by offering products at discounted rates.

Here’s my two cents anyway -

Competition in lending is tough and consumer finance is even tougher to crack. Unlike telecom, RIL has its competition cut out from battered lenders.

Bajaj Finance for instance has 140,000 points of sale and is on track to go fully digital by March 2023.

Let’s talk about Paytm. A report by Australian financial services firm Macquarie ominously saying that Jio Financial Services entry into lending is a threat to Paytm and Bajaj Finance sent Paytm’s stock into a tizzy. The report said “While it is too early to take understand the exact customer segments and target markets that Jio Financial plans to cater to, it seems clear that it will be focused on consumer and merchant lending, which is the mainstay of NBFCs like Bajaj Finance and fintechs like Paytm."

It is, in fact, too early. Paytm has 30 million merchants - this includes groceries, streetside-stalls - compared to Reliance’s 2 million merchants; it disbursed 9.1 million loans in the quarter ended September 2022 - a 224% YoY jump. That’s tough competition!

Source: Paytm

This TRAI report from September 2022 shows Jio has 426 million users that it has acquired from scratch in the last six years. In theory, this means Jio will be able to offer loans to all of the 426 million of its customers. And while nobody can say with certainty if all these 426 million customers will convert to borrowers (unlike in China with limited options), cross-selling their financial products is that much easier.

JFS listing as a separate conglomerate means little to its credit rating - RIL, the parent company, will still hold 50% of the company. And RIL has the best credit ratings, which means borrowing will be much easier than other shadow lenders.

Source: RIL

Demand is on the uptick. According to the Reserve Bank of India, bank loans for consumer durables grew 57% YoY in October 2022. Imagine the number of products it could build on top of that demand when its 600-odd million (400 mobile and 200 registered offline customers just on reliance retail) want to purchase a washing machine, a flat-screen TV or clothes.

The financial services market is big enough and the underbanked/unbanked pool, wide enough. There’s room for everyone. When fintechs came on the scene, everyone was worried about their imminent threat to banks. Over a decade into the fintech frenzy, we’ve seen innovation from all quarters; incumbents included (Think SBI Yono or Kotak 811). The way I look at it, RIL has contrived strategies to continue to stay relevant and for all we know, it could partner with lenders to create a larger ecosystem for itself.

What does this all mean?

I’m not sure there’s a single takeaway - it’s a mosaic of much more granular insights that are context specific. The industry is so wildly different than it was 10 years ago. We haven’t had a major financial crisis since 2008 - COVID-19 and a war in Ukraine later, the world is in a better place than it was in 2008, financially. There has been no financial crisis when there should have been one - financial systems have gotten more resilient.

Not to say there won’t be anymore financial crises; the build-up of leverage in economies around the world after an entire decade of cheap money is concerning; stagflation, credit deterioration, they’re all probable. But financial systems are in better shape than at any time in recent memory.

The only way to protect the world from a crisis is sound financial risk intermediation - and the risk management to support it. And banks have a core competency here. The industry has spent decades understanding the economics of each product and managing the risk pool thereof. It's an advantage for sure, but how can it keep up with the capital-light business that big tech is mastering? That’s for another newsletter.

For now, it’s going to be interesting to see how incumbents respond to high-growth tech and data services and the opportunities therein. It’s also going to be fascinating to watch how the financial services industry is going to look like in 2032. Rising interest rates, shifting consumer loyalty, trust, and spending patterns, tech valuations coming under market scrutiny, changing climate, more pandemics, phew! The next decade could look wildly different from the last one. And the likes of Reliance Jio will be betting on it!

I’d love to hear your thoughts!

Cheers,

Rajat